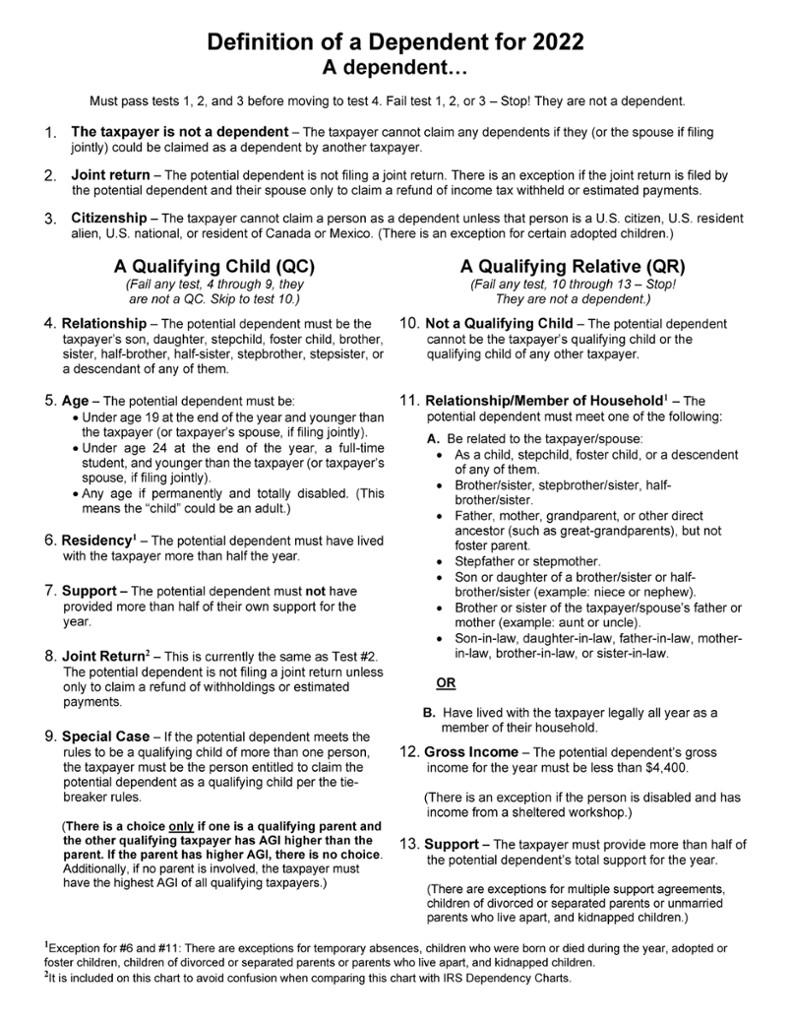

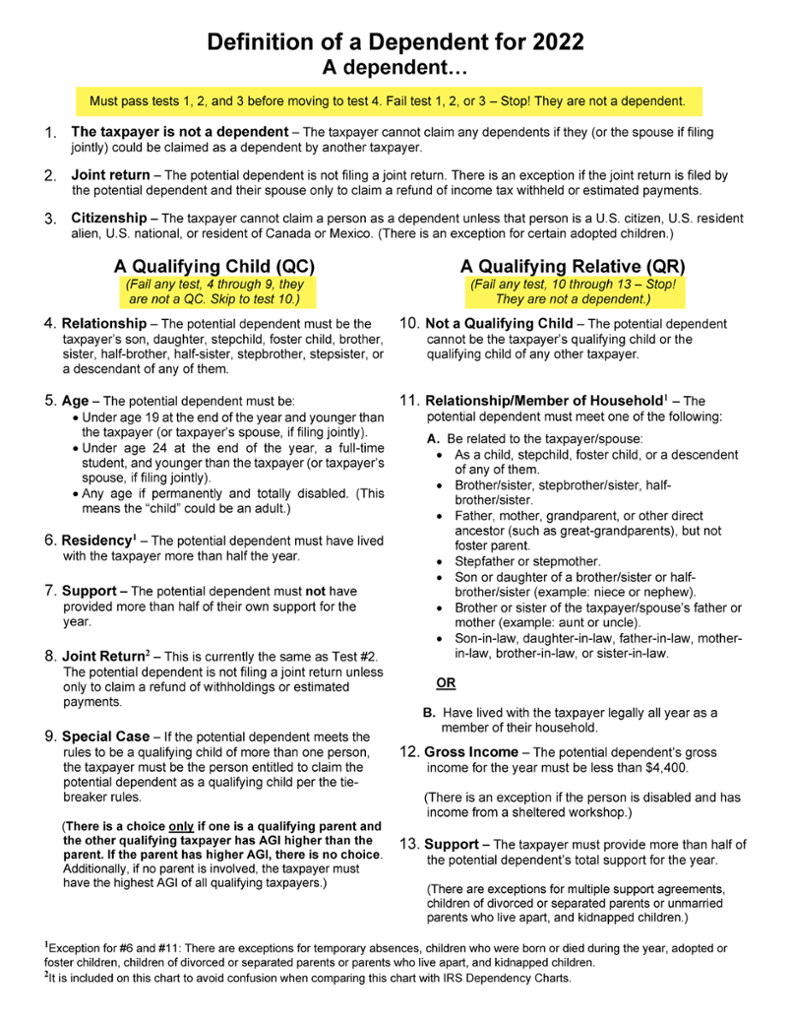

According to the Tax Code, the term dependent means either a qualifying child (QC) or a qualifying relative (QR).

All the requirements for claiming dependency are summarized below. (A PDF copy of the chart can be found here.)

This Definition of a Dependent chart can be used to guide you through the dependency requirements. It is numbered in the order the requirements must be met.

For each potential dependent (person), you will consider the first requirement at the top. If any of the first three requirements are not met, you do not have to go any further. The “potential dependent” is not a dependent.

If the first three requirements are met, then you move down to the fourth requirement, which is under qualifying child (QC). If all of the requirements under qualifying child are met, you can stop because the person is a qualifying child of the taxpayer. Requirement #9 must be applied to determine if they are also the taxpayer’s qualifying child dependent.

If any of the requirements under qualifying child are not met, you immediately move to the first requirement, #10, under qualifying relative (QR). If all of these requirements are met, you can stop because the person is a qualifying relative dependent.

If any of the requirements under qualifying relative are not met, the person is not a dependent.

Throughout this course, you can use this chart to guide you through whether a taxpayer has a dependent or not. Always start from the top with the first three requirements, move to the qualifying child requirements, and then if needed move to the qualifying relative requirements.

In this chapter, we will work through the dependency requirements using this strategy.

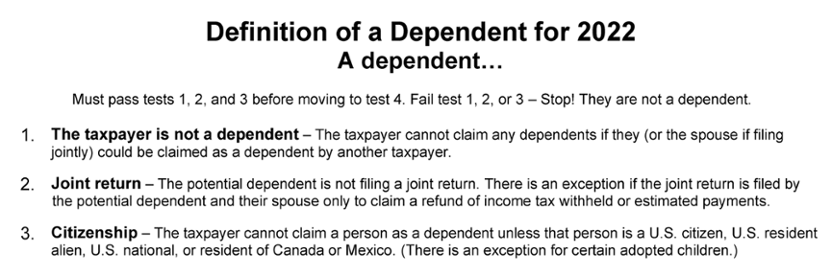

For a taxpayer to claim a qualifying child or qualifying relative as a dependent, the following three tests (or requirements) must be met:

Any taxpayer who qualifies as a qualifying child or qualifying relative of another taxpayer may not claim any dependents. Even if the other person does not claim the taxpayer, the taxpayer still may not claim any dependents. If the dependent taxpayer has a qualifying child or a qualifying relative of their own, they are not exempt from this requirement and cannot claim the dependent. Also, if the taxpayer is filing a joint return and their spouse can be claimed as a dependent on someone else’s return, then the taxpayer and spouse cannot claim any dependents on their joint return.

EXAMPLE

Lori (18) and her potential qualifying child, Cheryl (5 months), lived together with Lori’s mother, Brenda (41), for the entire tax year. Lori passes all of the requirements to be Brenda’s qualifying child, and Brenda will claim Lori as a dependent on her tax return. Lori cannot claim herself, nor can she claim Cheryl since she herself is a dependent of another taxpayer.EXAMPLE

Amparo (32) and her potential qualifying child, Miguel (3), lived together for all of the tax year. Amparo is not a dependent of another taxpayer and no one can claim Amparo on their return. Amparo may claim Miguel on her return, assuming the other tests are met.EXAMPLE

Helena (18) and her potential qualifying child, Landon (2 months), lived together with Helena’s father, Brad (45), for all of the tax year. Helena passes all of the requirements to be Brad’s qualifying child.A taxpayer may not claim a married person as a dependent if the married dependent files a joint return.

EXAMPLE

Ian (51) lived together with his potential qualifying child, Robert (21), for all of the tax year. In October of the same year, Robert married Veronica (21), and both lived with Ian for the remainder of the year. Robert, a full-time student, did not provide any of his own support, and Veronica earned only $3,000 and qualifies as a dependent of her parents. Robert and Veronica filed a joint return to get a refund of $102 withheld from Veronica’s wages. Ian may still claim Robert as his dependent since Robert was only filing a joint return to claim a refund of income tax withholding.EXAMPLE

Ronald (54) and Wendy (52) are married and lived with their potential qualifying relative, Gwyn (26), for all of the tax year. In November of the same year, Gwyn married Tim (27), and both lived with Ronald and Wendy for the rest of the year. Gwyn earned $2,400, and Tim earned $25,500, requiring him to file a tax return. Ronald and Wendy may not claim Gwyn as their dependent on their return if Tim and Gwyn file a joint return, because Tim is required to file a tax return and they would not be filing only to claim a refund of withholdings.A taxpayer may not claim a person as a dependent unless that person is one of the following:

EXAMPLE

Phoebe, a citizen of Russia, was legally placed with Madeleine and Joshua Smith, both U.S. citizens, on August 11 of the tax year. She lived with the Smiths from that date forward. Phoebe would pass this test since she lived with the Smiths for the rest of the year after her placement.Generally, a child is a citizen or resident of the country of their parents. If the taxpayer was a U.S. citizen when the child was born, the child may be a U.S. citizen even if the other parent was a nonresident alien and the child was born in a foreign country.