Table of Contents |

Let’s start with the basics: Personal finance is about managing your money to meet your life goals. Whether you’re saving for a vacation, paying off debt, or planning for retirement, personal finance gives you the tools to make it happen. It’s like being the CEO of your financial life—you make decisions, set goals, and manage resources to create the future you want.

Here’s why personal finance matters:

Did you know that over 60% of Americans live paycheck to paycheck, even those earning six-figure salaries (Dickler, 2023)? This statistic underscores the importance of personal finance—it’s not about how much you earn but how you manage what you have.

Now that you understand what personal finance is, let’s explore how it impacts various aspects of your life—beyond just the numbers.

Managing your finances isn’t just about crunching numbers or balancing a budget; it’s about setting yourself up to live the life you want. Think of it as a domino effect—every financial choice you make ripples out and affects your career, relationships, health, and future goals. When you understand and take control of your money, you’re not just saving for a rainy day; you’re building a foundation that supports your entire life.

For instance, imagine being able to choose a job you love instead of one that simply pays the bills or having the peace of mind to handle unexpected expenses without anxiety. Financial health isn’t just a nice-to-have; it’s a necessity for reducing stress, making empowered choices, and achieving your dreams.

Here’s a closer look at four ways personal finance weaves into the key areas of your life:

1. Career Decisions

Your finances can dictate your job choices. For example, if you’re drowning in debt, you might prioritize a high-paying job over one that aligns with your passions. On the other hand, good financial planning can give you the freedom to take risks, like starting a business or switching careers.

EXAMPLE

Jamie had $50,000 in student loans and felt trapped in a high-stress job. By creating a payoff plan and cutting unnecessary expenses, Jamie gained the financial flexibility to pursue a fulfilling career in teaching.2. Relationships

Money can make or break relationships. In fact, 70% of couples argue about money more than any other topic (Hinson, 2023). Learning to manage finances together and communicate openly can strengthen trust and reduce conflict.

3. Mental and Physical Health

Financial stress is a leading cause of anxiety and health problems. A study by the Money and Mental Health Policy Institute (n.d.) found that people with high financial stress are more likely to experience mental health problems—and poor mental health may make it harder to overcome financial difficulties. Building an emergency fund and reducing debt can significantly ease these pressures. We’ll cover all of these important money topics in upcoming lessons, including the psychological impacts of money.

4. Life Goals

Personal finance helps you turn dreams into reality. Whether it’s traveling, buying a home, or starting a family, learning about personal finance ensures you’re prepared.

As you can see, personal finance isn’t just about dollars and cents—it’s about building the life you want. Let’s talk about how mastering personal finance can help you on your journey.

When you take control of your finances, you take control of your life—your choices, your opportunities, and your peace of mind. Imagine a life where money isn’t a constant source of stress but a tool that empowers you to pursue your goals and dreams. Whether it’s having the freedom to take a career risk, the security to handle unexpected emergencies, or the ability to build a legacy for future generations, personal finance is the key that unlocks these possibilities.

Here are five ways that controlling your finances can transform your journey:

1. Freedom to Choose

Financial independence is the ultimate enabler. It gives you the freedom to make decisions based on your desires and values rather than being constrained by financial obligations. Picture this: You’ve always wanted to take a sabbatical to travel the world, write a book, or learn a new skill. When your finances are in order, these opportunities become real possibilities instead of distant dreams. Financial independence might also mean having the flexibility to leave a job that doesn’t serve you or taking the leap to start a business you’re passionate about.

2. Security in Uncertainty

Life is unpredictable, but having an emergency savings fund covering 3–6 months of expenses can make the unpredictable feel manageable. (Don’t worry; we’ll show you how to build savings in an upcoming lesson.) Think about the peace of mind that comes with knowing you can handle unexpected challenges—whether it’s a job loss, medical emergency, or home repair—without spiraling into debt. Security isn’t just about having money in the bank; it’s about knowing you’re prepared for whatever life throws your way.

EXAMPLE

During the COVID-19 pandemic, millions of people faced sudden job losses. Those with emergency savings were able to weather the storm more comfortably, while others struggled to cover basic needs. An emergency fund acts as a financial safety net, giving you the time and breathing room to find your footing during tough times.3. Building Generational Wealth

Financial success doesn’t stop with you; it’s an opportunity to create a lasting legacy. By saving and investing wisely, you can build wealth that benefits your children, grandchildren, and beyond. Generational wealth isn’t just about passing down money—it’s about passing down financial knowledge, habits, and opportunities.

Imagine being able to help your child graduate college debt-free or providing the seed money for their first business venture. Generational wealth creates a ripple effect, giving future generations the tools to succeed without starting from scratch.

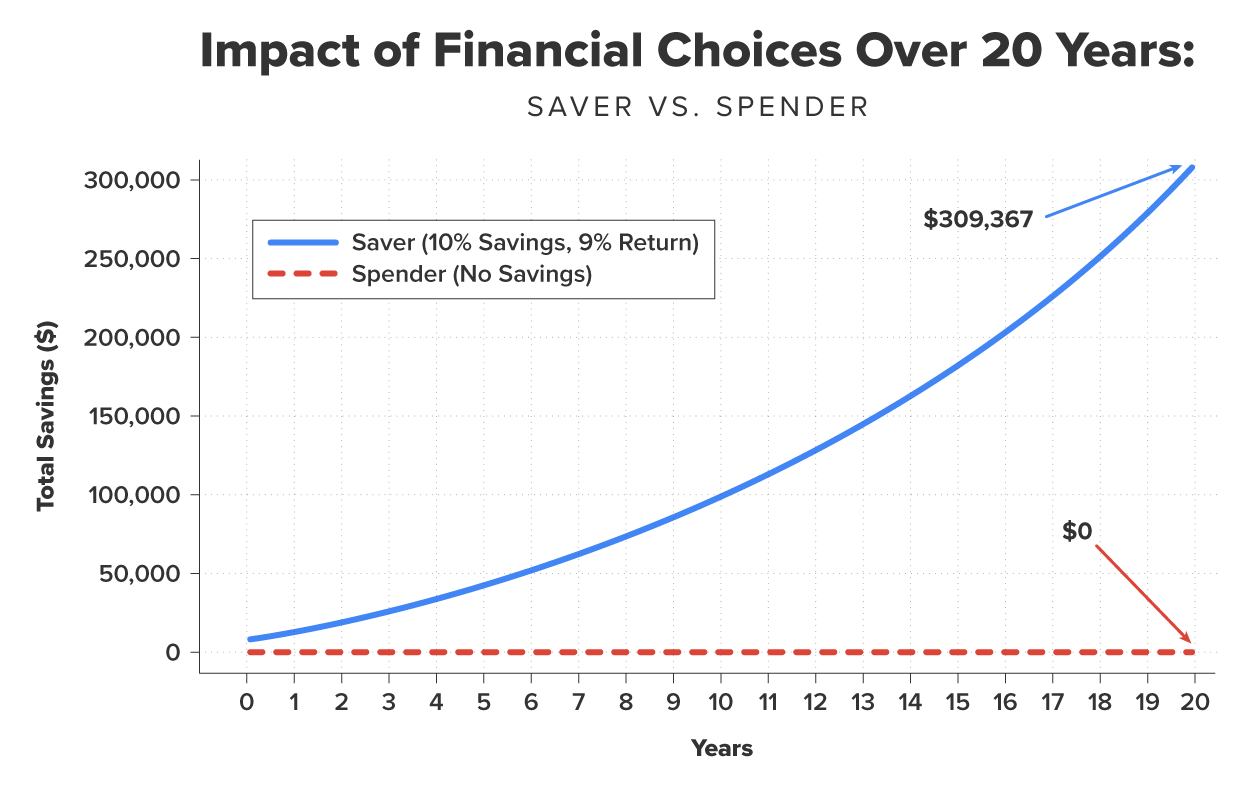

4. The Power of Financial Discipline: A Tale of Two Paths

Let’s explore the life-changing impact of financial choices on two individuals, Alex and Jamie. Both earn the same annual income of $50,000, but their financial decisions couldn’t be more different.

This example shows that achieving financial freedom isn’t about earning more—it’s about making intentional choices with the money you have. By saving consistently and investing wisely, you can create a future filled with possibilities and security.

5. Money and Happiness

While money can buy comfort and security, it doesn’t necessarily lead to fulfillment. A study by the Kahneman-Treisman Center for Behavioral Science & Public Policy Princeton University (2023) found that emotional well-being increases with income only up to about $75,000 annually. Beyond that, the link between money and happiness weakens.

Understanding that wealth is a tool, not a solution, sets the stage for making smart financial decisions. However, the choices we make with our money are deeply influenced by personal values, life experiences, and emotional triggers. Let’s delve into the factors that shape our financial decisions and uncover how they impact our journey toward financial independence and fulfillment.

If you’re new to managing money, it might feel like your financial decisions are random or based solely on what’s happening at the moment. However, in reality, your choices are influenced by a mix of internal factors, like your upbringing and the people around you, and external factors, such as the economy. Understanding these influences can help you take control of your financial journey and make decisions that truly align with your goals. Let’s break four common influences down step by step so it feels approachable and doable.

1. Your Upbringing and Environment

Think about how your family handled money when you were growing up. Were they savers, spenders, or somewhere in between? If you saw your parents stressing about bills, you might feel anxious about money now. On the other hand, if you grew up in a household that taught you to save, you might feel more confident managing finances.

EXAMPLE

Imagine two friends, Sam and Alex. Sam’s parents always emphasized saving for emergencies, so Sam naturally sets aside money each month. Alex’s parents lived paycheck to paycheck, so Alex is still learning how to save and budget as an adult. Both paths are normal, but understanding where your habits come from can help you decide what to keep and what to change.2. Social and Cultural Influences

Have you ever felt pressured to buy something because your friends had it or because you saw it on social media? Society often equates success with owning the latest gadgets, wearing designer clothes, or going on luxury vacations. It’s easy to fall into the trap of spending to keep up with others, but this can lead to financial stress if it’s not aligned with your actual goals.

3. Your Financial Education

The more you know about managing money, the better equipped you are to make smart choices. But here’s the thing: Most of us didn’t learn about personal finance in school. If you’ve ever felt overwhelmed by terms like “compound interest” or “asset allocation,” you’re not alone. The good news is that financial literacy is something you can build over time, and you’ll learn all about those terms and more in this course.

EXAMPLE

Gerrald used to avoid looking at his credit card statements because he didn’t understand how interest worked. After taking this Personal Finance course, he learned how to pay down his debt faster and started saving money on interest. Education gave him the confidence to tackle his finances head-on.4. The Economy and External Factors

Sometimes, your financial decisions are shaped by things outside your control, like inflation, interest rates, or job market conditions. For example, rising prices might mean you need to adjust your grocery budget, or low interest rates might make it a good time to refinance your mortgage. Staying informed about the economy can help you adapt your financial plan as needed.

EXAMPLE

During a period of high inflation, Jessica noticed her grocery bill climbing. Instead of letting it derail her budget, she started meal planning and shopping at sales, which helped her stay on track without sacrificing too much.Now that you understand what influences your financial decisions, you’re better prepared to take control and make choices that align with your goals. Let’s dive into the specific topics this course will cover to help you build a strong financial foundation.

This course is designed to be your ultimate guide to mastering personal finance, no matter where you’re starting from. Whether you feel completely overwhelmed by money or just want to sharpen your skills, we’ll cover everything you need to know to take control of your financial future. Each topic builds on the last, giving you a clear path to success. Here’s a sneak peek of what’s in store:

This course is your road map to financial empowerment. Here’s what you can expect:

Personal finance may seem daunting, but it’s a journey worth taking. Each step you take brings you closer to financial freedom and the life you envision. Let’s dive in and start building your financial future!

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.

REFERENCES

Dickler, J. (2023, September 27). 60% of Americans are still living paycheck to paycheck as inflation hits workers’ wages. CNBC. www.cnbc.com/2023/09/27/60percent-of-americans-are-still-living-paycheck-to-paycheck.html

Hinson, K. (2023, September 19). 54% of engaged americans disagree with partner on financial goals. Nerdwallet. www.nerdwallet.com/article/finance/54-of-engaged-americans-disagree-with-partner-on-financial-goals

Kahneman-Treisman Center for Behavioral Science & Public Policy Princeton University. (2023, March 8). Kahneman resolves conflict on income-wellbeing study, finds point at which unhappiness stops decreasing for unhappy people. behavioralpolicy.princeton.edu/news/DK_wellbeing0323#:~:text=Daniel%20Kahneman%20and%20Angus%20Deaton%20%2C%20both,which%20there%20was%20no%20increase%20in%20well-being

Money and Mental Health Policy Institute. (n.d.). The facts. What you need to know. www.moneyandmentalhealth.org/money-and-mental-health-facts/