Table of Contents |

If you’ve ever set aside money for a future purchase—a dream vacation, a new laptop, or even a down payment on a home—you’ve already started thinking like an investor. Investing is about taking the money you have today and putting it to work so that it grows over time, ideally at a rate faster than inflation (the silent money thief that makes everything more expensive while your cash sits stagnant).

But before we get into stocks, real estate, bonds, or crypto, let’s strip investing down to its simplest form: what it actually means and why it’s a game changer for your financial future.

What Does Investing Actually Mean?

At its core, investing is using your money to acquire assets—things that have the potential to increase in value or generate income over time. The goal? To make your money work for you instead of just working for your money.

Imagine you have $100. You could do three things with it:

People invest for all kinds of reasons, but at the core, investing is about expanding your financial possibilities and giving yourself more freedom and security. Here’s why it matters:

Building Wealth

Investing allows your money to grow over time, helping you build wealth without having to work harder for every dollar. Imagine you put $500 in a basic savings account earning 0.01% interest—you might have an extra 50 cents after a year. But if you invest that same $500 in a well-performing stock or index fund, it could grow into thousands over time, thanks to compound growth. The key is time and patience.

Beating Inflation

Inflation means that the cost of everything—groceries, rent, travel—goes up over time. If your money isn’t growing at least as fast as inflation, you’re actually losing purchasing power. Think about your grandparents’ stories of how a loaf of bread used to cost a quarter. If they had stashed all their money under a mattress instead of investing it, that money would be worth far less today. Investing helps you stay ahead so your money doesn’t lose value.

Creating Financial Security

One of the biggest benefits of investing is that it can generate income beyond your regular paycheck. If you’ve ever worried about losing your job or unexpected expenses, investments like dividend-paying stocks, rental properties, or even a side business can create additional streams of income. This gives you more flexibility and control over your financial future.

Funding Life Goals

Whether it’s buying a home, starting a business, traveling, or sending your kids to college, investing helps you afford the things that matter most. Let’s say you want to take a dream trip to Europe in 5 years. Instead of just saving for it, you could invest a portion of your money in a stock index fund. With a solid annual return, your investment could grow significantly over those 5 years, making it easier to fund the trip without derailing other financial goals.

Investing isn’t just about making money—it’s about creating opportunities and ensuring that your future self has more choices, not fewer.

Let’s dive deeper into the power of compound interest when you start investing.

Albert Einstein supposedly called compound interest “the eighth wonder of the world.” If you’ve ever wondered why some people seem to build wealth effortlessly while others struggle, compound interest is a big part of the answer.

You’ve already learned about compound interest in terms of savings, but now let’s look at it through the lens of investing—because this is where the real magic happens.

What Makes Compound Interest So Powerful?

Unlike simple interest, where you only earn money on your initial investment, compound interest allows your earnings to generate more earnings. In other words, you’re not just making money on what you invested—you’re making money on the money your investment already earned.

Think of it like a snowball rolling down a hill. At first, it’s small and slow moving, but as it picks up snow, it grows bigger and faster. The longer it rolls, the more unstoppable it becomes. That’s exactly how compound interest works with investing. The earlier you start, the more time your money has to multiply.

EXAMPLE

Let’s say you invest $1,000 in a fund that earns an average return of 10% per year. At first, that might not seem like much, but here’s how it actually plays out:In investing, time is your greatest ally. The earlier you start, the more you benefit from compounding. That’s why many wealthy investors say that time in the market matters more than trying to “time” the market.

Timing the market is when investors try to guess the best time to buy low and sell high to make the most money. The problem is that no one can predict exactly when prices will go up or down, so it’s risky and often leads to mistakes. Instead, investing regularly over time is usually a smarter and safer strategy.

Think of these two friends:

Take a look at the image below for another visual explanation of the power of compound interest plus starting to invest earlier in life.

.")

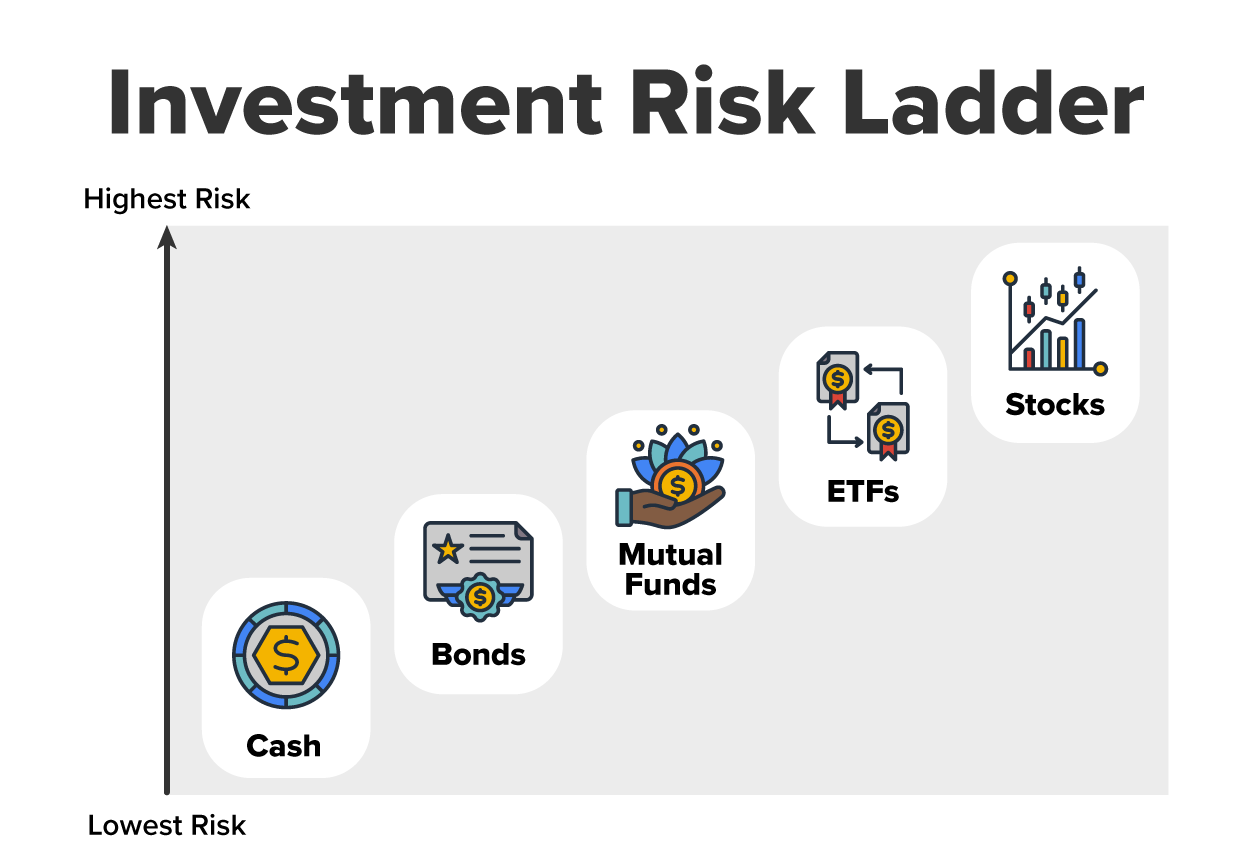

Investing isn’t just about putting your money into something and hoping for the best. It’s about understanding the relationship between risk and reward—how much uncertainty you’re willing to take on in exchange for potential gains.

At its core, higher risk often means higher potential rewards but also a greater chance of losing money. Lower-risk investments are more stable but usually grow much more slowly. Your job as an investor is to find the right balance based on your comfort level, timeline, and financial goals.

EXAMPLE

Imagine you’re choosing between three different ways to grow your money. Each one has different levels of risk:

To make this even easier to understand, think about it like choosing how to travel to a destination:

Choosing the right investments comes down to your risk tolerance—how comfortable you are with the possibility of losing money in exchange for the chance of higher returns. We covered this term in a previous lesson, but let’s explore it in terms of investing.

Ask yourself these questions:

The bottom line? Risk is part of investing, but understanding your comfort level and diversifying wisely can help you grow wealth without unnecessary stress.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.