Table of Contents |

Imagine this: You’re driving your car, enjoying the music and the open road. Suddenly, another car runs a red light and crashes into yours. Thankfully, you’re unharmed, but your car’s front end is destroyed. Now, imagine you don’t have car insurance. Not only are you dealing with a major headache, but you’re also stuck paying thousands of dollars to repair or replace your car.

This is where insurance steps in. It’s a safety net that protects you financially when life throws unexpected curveballs. Whether it’s a car accident, a medical emergency, or damage to your home, insurance ensures that you’re not left to cover the full cost alone.

Insurance is a contract between you and an insurance company. You pay a regular fee, called a premium, and in exchange, the insurance company promises to help cover specific financial losses if something unexpected happens.

Think of insurance like a financial umbrella. It doesn’t stop the rain (accidents, illnesses, or disasters), but it keeps you from getting drenched by the costs.

Insurance isn’t just about money—it’s about peace of mind. It helps you face life’s what-if situations without constant worry. Whether it’s a car accident, a medical bill, or damage to your home, insurance ensures you can recover without draining your savings or going into debt.

To truly understand how insurance works and what it covers, it’s important to familiarize yourself with some key terms. These terms are the building blocks of any insurance policy and will help you make informed decisions about the coverage you need.

Insurance can often seem confusing because of all the terms used with different insurance products. Insurance can feel overwhelming, especially when you’re faced with a sea of unfamiliar terms. Deductibles, premiums, exclusions—it’s enough to make anyone’s head spin. But understanding these terms is the key to choosing the right coverage and avoiding surprises when you actually need to use your insurance.

Here’s a guide to understanding all of the terms that you need to know when you go to purchase insurance.

1. Premium

This refers to the amount you pay (monthly, quarterly, or annually) to maintain your insurance coverage. Think of it as the cost of keeping your financial safety net in place.

EXAMPLE

You might pay $100 per month for health insurance. If you stop paying, your coverage will lapse, leaving you unprotected.2. Policy

This refers to the written contract between you and the insurance company. It outlines the terms of your coverage, including what is covered, what is excluded, and any specific conditions.

EXAMPLE

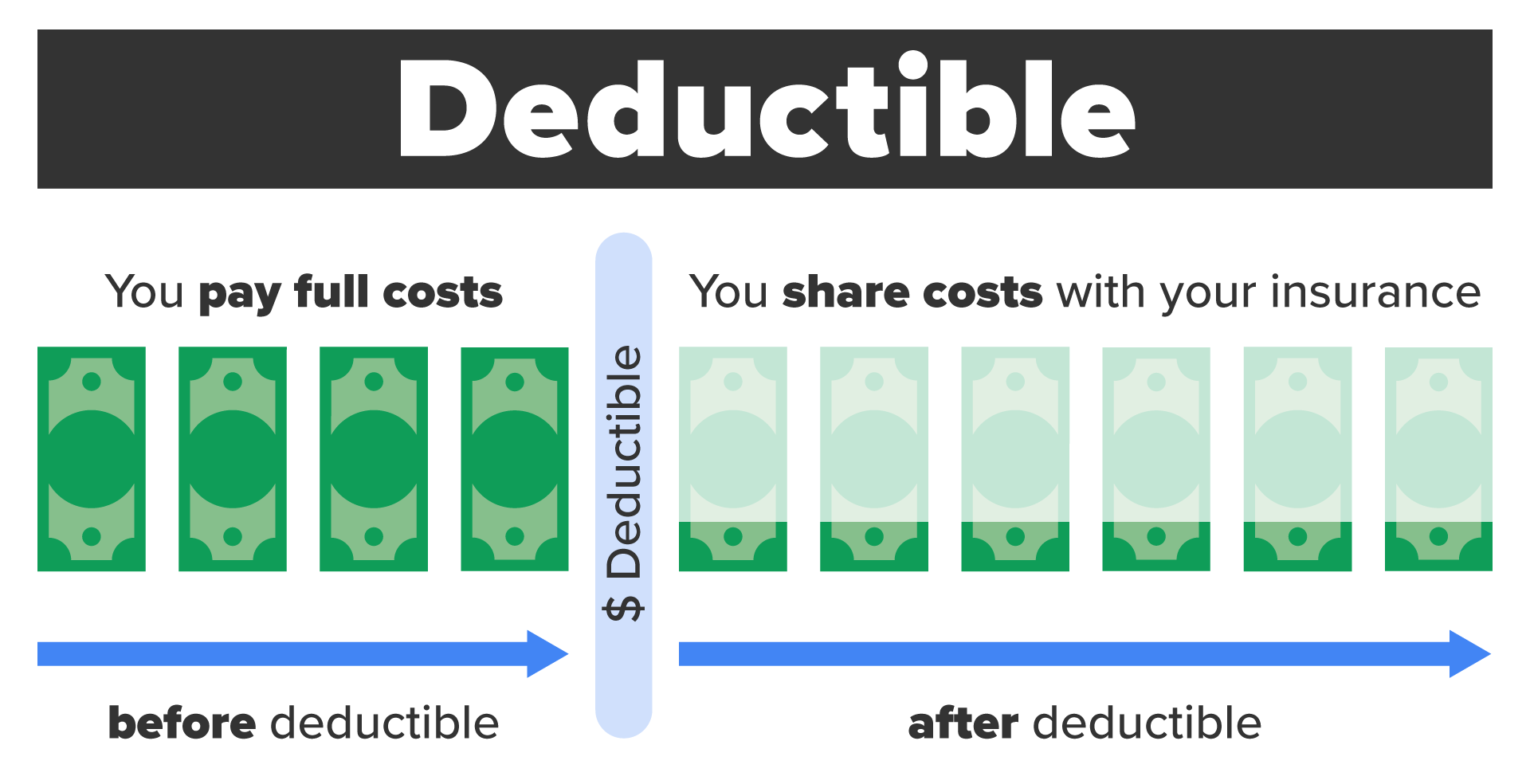

Your car insurance policy might include coverage for collisions and theft but exclude damage from off-road driving.3. Deductible

This refers to the amount you must pay out of pocket before your insurance begins to cover expenses. Higher deductibles often mean lower premiums, but you’ll need to pay more up-front in the event of a claim.

EXAMPLE

If your deductible is $500 and you have a $1,500 medical bill, you pay $500 and your insurance covers the remaining $1,000.4. Coverage Limit

This refers to the maximum amount your insurance will pay for a covered loss. Anything above this limit is your responsibility.

EXAMPLE

If your home insurance policy has a $300,000 coverage limit, the insurer will pay up to that amount to repair or rebuild your home after a disaster.5. Claim

This refers to the formal request you make to your insurance company to pay for a covered loss. The insurer reviews your claim to determine if it falls under your policy’s coverage.

EXAMPLE

You file a claim after a tree falls on your car during a storm. The insurance company assesses the damage and reimburses you for repairs.6. Beneficiary

This refers to the person or entity who receives the payout from a life insurance policy in the event of your death. It ensures that your loved ones are financially supported.

EXAMPLE

If you name your spouse as the beneficiary, they’ll receive the life insurance payout to cover expenses like the mortgage or childcare.7. Exclusions

This refers to the specific events or circumstances that your insurance policy does not cover. Always read the fine print to understand these.

EXAMPLE

A homeowner’s policy might exclude damage caused by floods, requiring you to buy separate flood insurance.8. Endorsement (or Rider)

This refers to an add-on to your insurance policy that provides additional coverage or modifies the original terms.

EXAMPLE

You might add an endorsement to your home insurance to cover expensive jewelry or electronics.9. Underwriting

This refers to the process that insurance companies use to evaluate your risk and determine the terms of your coverage, including premiums.

EXAMPLE

When applying for life insurance, the company may consider your age, health, and lifestyle during underwriting.Now that you have a clear understanding of the key insurance terms, you’re ready to explore the different types of insurance available. Each type is designed to protect a specific part of your life, from your health to your home, car, income, and more. Understanding these options will help you decide what coverage you need to safeguard the things that matter most. Let’s dive into the types of insurance and see how they work to keep you financially secure.

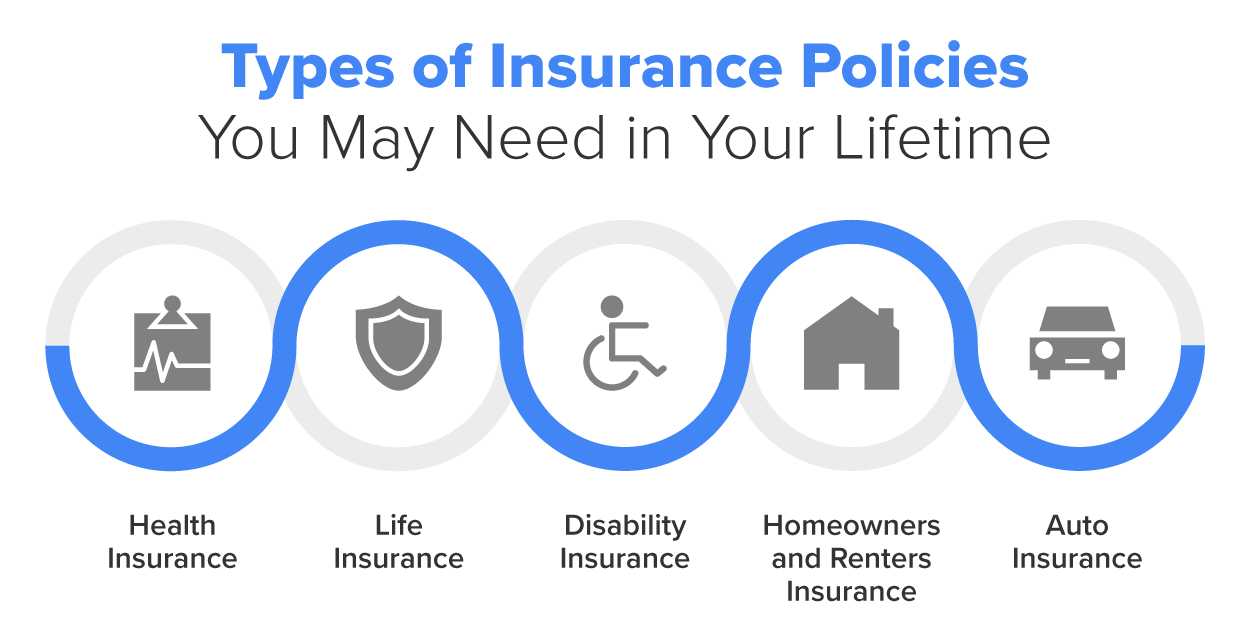

Just like you’d protect your phone with a sturdy case, insurance protects the important things in your life—your health, car, home, and even your income. In this section, we’re breaking down the different types of insurance so you know what’s worth protecting and why. Let’s make sure you have the right coverage for the life you’re building. We will go into more detail about each of these types of insurance in the following lessons. For now, here are the basics you need to know about the six most common types of insurance.

1. Health Insurance

Health insurance is a plan that helps pay for medical care, from doctor visits to hospital stays, so you’re not stuck footing massive bills.

Why it matters: Healthcare costs can add up fast. A simple hospital visit or prescription can quickly turn into thousands of dollars. Health insurance acts as your financial shield, keeping medical debt from taking over your life.

EXAMPLE

Sarah trips and breaks her arm, ending up in the ER. The total cost is $3,000, but her health insurance reduces her expenses to just her $200 deductible. The rest is covered, giving Sarah peace of mind and financial relief.2. Car Insurance

Car insurance is a must-have plan that covers damage to your car, property, or medical bills if you’re involved in an accident.

Why it matters: Most states legally require car insurance, but beyond that, it saves you from paying out of pocket for expensive repairs or lawsuits. Accidents happen, and car insurance is there to help you bounce back without breaking the bank.

EXAMPLE

After a fender bender, repairing your car costs $5,000. Your car insurance covers it, and you only pay a $500 deductible. It’s much easier to handle that than the full cost.3. Homeowners or Renters Insurance

Homeowners insurance or renters insurance are policies that protect your home, belongings, or both from damage caused by events like fire, theft, or natural disasters. Homeowners insurance covers the house, the property, and your belongings, while renters insurance solely focuses on your belongings.

Why it matters: Imagine losing everything in a fire or burglary. Replacing your belongings or rebuilding your home could wipe out your savings. This insurance helps cover the cost so that you’re not starting over from scratch.

EXAMPLE

A burst pipe floods your apartment and ruins your furniture. Renters insurance steps in to help you replace what’s damaged, sparing you a massive financial hit.4. Life Insurance

Life insurance is a policy that provides a financial payout to your loved ones if you pass away.

Why it matters: Life insurance ensures that your family is financially secure and can cover expenses like a mortgage, college tuition, or day-to-day living costs in your absence.

EXAMPLE

When the family’s main breadwinner passes away unexpectedly, their life insurance policy provides enough money to pay off the mortgage and maintain the family’s standard of living.5. Disability Insurance

Disability insurance is a plan that replaces part of your income if you can’t work because of injury or illness.

Why it matters: Your income is your lifeline. If an injury or illness prevents you from working for months, disability insurance helps cover your bills and living expenses so that you can focus on recovery.

EXAMPLE

John injures his back and can’t work for 6 months. His disability insurance kicks in, providing 60% of his income during that time and keeping him afloat financially.6. Liability Insurance

Liability insurance is a policy that protects you financially if you’re legally responsible for injuring someone or damaging their property.

Why it matters: Accidents happen, and lawsuits can be expensive. Liability insurance ensures that you’re not stuck paying massive legal or medical bills out of pocket.

EXAMPLE

Your dog bites a neighbor, and they sue you for medical expenses. Liability insurance covers the cost, saving you from a hefty personal expense.

It’s clear that insurance is all about protecting what matters most—your health, your home, your income, and your future. But knowing what insurance is isn’t enough. To make it work for you, you need to understand how it works—how premiums, deductibles, and coverage limits come together to create a plan that fits your life.

Insurance might seem complicated at first, but the process is designed to be straightforward once you break it down. Essentially, it’s a partnership between you and the insurance company: You pay for protection, and it helps cover the costs when something goes wrong. Let’s walk through the five key steps to understanding how it all comes together.

Step 1. You Buy a Policy

The first step is choosing the right type of insurance policy based on your needs. Whether it’s health insurance, car insurance, or renters insurance, the goal is to find a plan that provides the right amount of coverage for your specific risks. For example, if you’re a driver, you’ll want car insurance that covers potential accidents or damage to your vehicle.

When you purchase a policy, you’ll receive a document outlining all the details: what’s covered, what’s not, how much you’ll pay in premiums, and what your deductible will be.

Step 2. You Pay Premiums

Premiums, as you’ve learned, are the regular payments you make to the insurance company—usually monthly, quarterly, or annually. Think of them like a membership fee that keeps your policy active. As long as you pay your premiums on time, you remain protected under the terms of your policy.

Step 3. Something Happens

This is when your insurance policy goes into action. A covered event occurs—maybe you’re in a car accident, a storm damages your home, or you need emergency medical treatment. The key is that the event must be covered under your policy.

Step 4. You File a Claim

After the event, you notify your insurance company and file a claim. Filing a claim means providing details about what happened, including any necessary documentation like photos, medical bills, police reports, or repair estimates. The more detailed and accurate your claim, the faster it can be processed.

For example, if you’re in a car accident, you might include photos of the damage, a copy of the police report, and any repair estimates from a mechanic.

Step 5. The Insurer Pays

Once the insurance company verifies your claim and confirms that the event is covered, it steps in to cover the costs. This typically happens after you pay your deductible, which is the amount you agreed to pay out of pocket when you signed up for the policy.

Understanding how insurance works is the foundation for making informed decisions about the coverage you need. It’s all about partnership: You contribute by paying premiums, and the insurance company steps in when life takes an unexpected turn. From buying a policy to filing a claim, the process is designed to ensure that you’re financially protected when it matters most.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.