Table of Contents |

Think about the thrill of finding a new place to live—the excitement of fresh beginnings and creating a cozy space that feels like home. But then reality steps in: How much can I actually afford without stretching myself too thin?

Whether you’re moving to a new city, upgrading to a bigger space, or buying a first home, understanding how much to spend on housing is critical. If you get this part right, you’ll be able to cover other essentials, save for the future, and feel in control. If you overspend, you risk falling into the trap of being “house-poor,” where your money is tied up in housing, making it hard to enjoy life or plan for the future.

The good news? There are tried-and-true rules that can guide you, helping you find a housing budget that works for your life, goals, and financial situation. In this lesson, we’ll explore some popular rules of thumb (eight of them), review eight examples, and discuss tips for making each rule work for you.

1. The 30% Rule: The Popular Starting Point

The 30% rule is probably the most well-known guideline for housing expenses. It suggests that you spend no more than 30% of your gross monthly income on housing. Remember from a previous lesson that gross income is income before taxes and other deductions, such as health care costs, are subtracted.

The idea of the 30% rule is to keep rent or mortgage payments low enough that you can afford other living costs, like food, utilities, transportation, and fun.

EXAMPLE

Let’s take Derrick, who recently got a job as a marketing coordinator. He’s making $4,000 per month before taxes and eager to move into a trendy city apartment. To figure out how much he should spend on housing, Derrick takes his income and multiplies it by 0.30:The 30% rule is straightforward and quick to calculate, which makes it easy for almost anyone to follow. It’s a reliable starting point, especially if you’re in a location where housing costs are manageable. However, this rule may not work great for you if you’re carrying significant debt or living in a high-cost area where rents are above average.

Let’s say Derrick is looking at rentals in a major city like New York or San Francisco. He quickly realizes that most apartments within his budget are in far-off neighborhoods or tiny spaces that might compromise his comfort or safety. In situations like these, the 30% rule might need some flexibility.

2. The 28/36 Rule: Balancing Housing and Debt

If you have significant debt—think student loans, car payments, or credit cards—the 28/36 rule might be a better fit. This rule takes a more comprehensive approach by factoring in both housing and total debt.

Here’s how it works:

EXAMPLE

Let’s look at Maria, who earns $5,000 per month and has monthly student loan payments of $300. Maria uses the 28/36 rule:The 28/36 rule is often recommended for anyone juggling multiple debts, as it helps keep everything manageable. Many mortgage lenders also use this rule to determine if someone can afford a loan, so understanding it can be helpful if you’re considering buying a home in the future. We’ll talk in depth about the mortgage process in an upcoming lesson.

However, this rule may not be flexible enough if you’re debt-free and want to allocate more of your income to housing. Or if you live in a city where rents are high, sticking strictly to the 28% housing limit could be challenging.

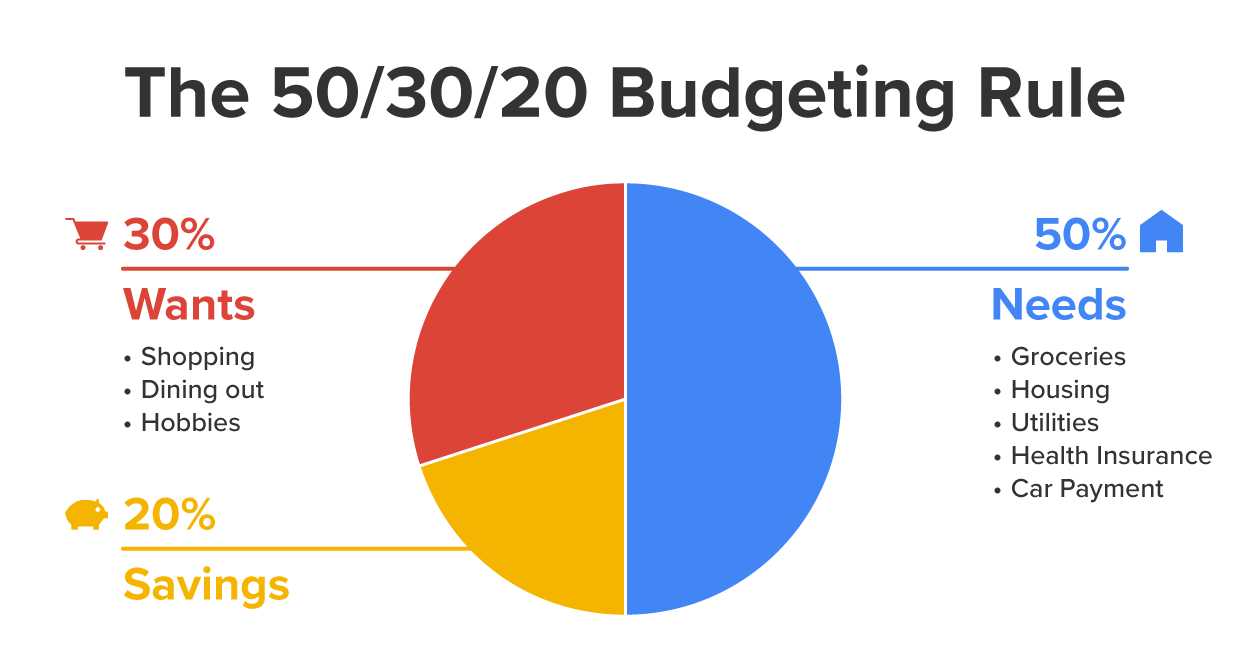

3. The 50/30/20 Rule: Budgeting for the Bigger Picture

While the 30% and 28/36 rules focus on housing specifically, the 50/30/20 rule that you’ve already learned about back in Unit 1 is a general budgeting framework that divides your income into three broad categories. Let’s review:

The 50/30/20 rule is ideal if you want to see your whole budget laid out. It provides a more flexible structure, so if your housing needs are higher, you could cut back slightly on wants to make room.

4. The One Week’s Paycheck Rule: A Fast, Easy Option

The one week’s paycheck rule is a simple alternative that suggests your monthly housing payment should be no more than one week’s worth of your gross income.

EXAMPLE

If Jose makes $4,000 a month, his weekly income is $1,000. Using the one-week rule, Jose would aim for a monthly housing budget of $1,000.This rule is straightforward and doesn’t require much math, making it perfect for a quick budget check. However, it doesn’t account for other expenses or debt, so it might not be the most accurate for everyone.

5. The Rent-to-Income Ratio Rule: A Renter’s Staple

If you’re renting, the rent-to-income ratio rule might be the simplest choice. This rule is often used by landlords and suggests that your rent should be no more than 25%–30% of your gross monthly income.

EXAMPLE

Consider Lily, who earns $5,000 a month. Using a 30% cap:6. The 25% Rule for Homebuyers: Planning for a Mortgage

For those planning to buy a home, the 25% rule recommends keeping your monthly mortgage payment at or below 25% of your take-home pay. This rule includes principal, interest, taxes, and insurance (often referred to as PITI). Not to worry, we’ll dive into how this works in more detail in an upcoming lesson.

EXAMPLE

Let’s say Chloe brings home $4,500 per month after taxes. Based on this rule, her ideal monthly mortgage payment would be around $1,125 or less.The 25% rule helps you avoid becoming house-poor and allows you to maintain a balanced budget even after buying a home.

7. The Savings-First Rule: Putting Goals First

The savings-first rule takes a unique approach by focusing on your savings goals before setting a housing budget. This rule helps you prioritize future goals, ensuring that the housing costs don’t crowd out savings.

Here’s how it works: Decide on your monthly savings target, subtract that from your income, and use what’s left for housing and other expenses.

EXAMPLE

Jaime is aiming to save $1,500 per month and earns $6,000. By saving first, he’s left with $4,500 to cover other expenses, including housing. He can then apply one of the housing rules—like 25%–30% of that remaining amount—to find a comfortable housing budget.8. The Location-Adjusted Rule: Flexibility for High-Cost Areas

If you live in a high-cost area with steep housing prices, the location-adjusted rule allows for a more flexible approach, often suggesting 40%–50% of your income for housing if necessary. To balance, you’ll likely need to cut back on nonessentials.

EXAMPLE

Take Benji, who earns $7,000 in Los Angeles. He spends 40% of his income on rent, or $2,800, which allows him to live in a safe, well-connected neighborhood. To offset this, Benji minimizes dining out and uses public transit.There are many ways to budget for housing, each with its benefits depending on your situation. From the simple 30% rule to the savings-first approach, these guidelines are like tools—some may fit perfectly, while others might need tweaking.

Now that you know the options, it’s time to pick the one that suits you best. Your financial goals, lifestyle, and location all play a role. Let’s explore some quick tips to help you choose the right rule for your ideal housing budget.

Now that you’ve explored a variety of housing budget guidelines, you might be wondering, “Which one should I actually follow?” Each rule has its strengths, but the right choice really depends on your unique circumstances, financial priorities, and lifestyle. Whether you’re balancing debt, saving for future goals, or navigating a high-cost city, there’s a rule (or combination of rules) that can work for you. Let’s dive into six (6) tips for picking the best approach to find your housing sweet spot.

1. If You’re Renting With Minimal Debt

The 30% rule or rent-to-income ratio rule might be the simplest choice if you’re renting and have little to no debt. These rules provide a clear budget cap without adding complexity, helping you ensure that rent fits comfortably within your overall budget. Plus, many landlords favor tenants whose rent is within 30% of their income, so following these rules can make it easier to secure an apartment.

2. If You’re Balancing Multiple Debts

The 28/36 rule is ideal if you’re managing debts like student loans, car payments, or credit card balances. This rule prioritizes your total debt-to-income ratio, keeping housing costs in check while accounting for your other obligations. By capping housing at 28% of your income and total debt at 36%, you create a buffer that prevents you from overcommitting to housing expenses.

3. If You Want an All-in-One Budgeting Approach

The 50/30/20 rule offers a full budgeting framework, not just for housing but for your entire income. This rule’s 50% allocation to essentials (including housing) helps ensure that other important needs are covered while still leaving room for savings and lifestyle expenses. This approach is perfect if you’re looking to maintain a balanced financial life without overfocusing on any one category.

4. If You’re Prioritizing Savings Goals

For savers, the savings-first rule helps you stay focused on your financial goals before setting a housing budget. By allocating a set amount to savings each month and then budgeting for housing based on what’s left, this rule ensures your housing choices won’t interfere with your future goals, like building an emergency fund or investing for retirement.

5. If You’re Buying a Home

The 25% rule for mortgage payments is a solid choice if you’re buying a home and want to avoid becoming house-poor. By limiting your mortgage to 25% of your take-home pay (after taxes), you’ll have a manageable payment that leaves room for other essentials. This rule considers total monthly expenses for principal, interest, taxes, and insurance, helping you maintain financial stability as a homeowner.

6. If You’re in a High-Cost City

The location-adjusted rule allows for more flexibility by suggesting that you allocate 40%–50% of your income to housing, if necessary, with the understanding that you’ll need to cut back on other expenses. In high-cost areas, spending more on housing can help you maintain a higher quality of life in a desirable location.

No single rule will be perfect for everyone, and your budget might benefit from a blend of these guidelines. Consider starting with one rule as your base, then adapt it to fit your unique needs. Remember, your housing budget is just one part of your financial life—finding the right balance can help you enjoy a comfortable home without compromising your financial future.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.