Table of Contents |

When we compute unit product cost, the difference between variable costing and absorption costing is that fixed overhead is not included in the product costs for variable costing. Unit product cost for variable costing includes direct materials, direct labor, and variable manufacturing costs. On the other hand, unit product cost under absorption costing includes direct materials, direct labor, variable manufacturing overhead, and fixed manufacturing overhead.

EXAMPLE

Suppose Bradley Company, a toy manufacturer, has a direct materials cost of $5 per unit, direct labor cost of $10 per unit, variable overhead of $3 per unit, fixed overhead of $600,000 per year, and the company expects to produce 60,000 units per year.As we previously discussed, the difference between variable costing and absorption costing is that variable costing does not include fixed overhead while absorption costing does. Now we will take a look at how this difference impacts how we report income.

When the income statement is prepared, we consider what happens when units produced are equal to units sold, when they exceed units sold, and when they are fewer than units sold. Generally speaking, income differs between variable costing and absorption costing when inventory levels change. The differences in income are due to the timing of when the fixed overhead costs are reported in the company’s income statement. With the differences in timing, income under absorption costing is higher when more units are produced than sold, and income is lower when fewer units are produced than sold.

Companies can use variable costing for internal reporting and business decisions; however, according to GAAP, absorption costing must be used for external reporting, such as financial and tax reporting. Internal reporting consists of providing financial data inside the company to managers, owners, and employees. External reporting provides financial data to creditors or investors outside the company.

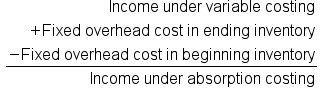

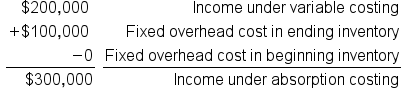

For most companies, it is time consuming and expensive to maintain both costing systems, so methods have been developed to convert reports that use variable costing into reports that use absorption costing. This is done by adding the fixed overhead cost in the ending inventory and subtracting the fixed overhead cost in the beginning inventory to the variable costing income.

EXAMPLE

Bradley Company has $200,000 in income using variable costing, with 10,000 units in the ending inventory, and nothing in the beginning inventory. The fixed overhead is $10 per unit, resulting in $100,000 fixed overhead costs in ending inventory (10,000 units x $10 per unit). The income under absorption costing is $200,000 (income using variable costing) + $100,000 fixed overhead costs in ending inventory = $300,000 income under absorption costing.

As a general rule, the difference in net income under absorption costing and variable costing is due to the change in inventories. Assuming a relatively constant level of production, if inventories increase during the year, then production exceeds sales and reported income will be less under variable costing than under absorption costing. On the other hand, if inventories decreased, then that means sales exceeded production, and income will be larger under variable costing than under absorption costing.

Variable costing is not currently acceptable for income measurement or inventory valuation in external financial statements that must comply with GAAP in the United States. However, managers often use variable costing for internal company reports.

When we prepare income statements under variable costing and absorption costing, we consider when the number of units produced is equal to, exceeds, or is less than the number of units sold. Income differs between the two methods when the inventory levels change, and the inventory level will change when units produced do not equal units sold.

When the income statement is prepared under variable costing, variable costs are reported separately from fixed costs. The contribution margin is used when reporting income under the variable costing method. The contribution margin can be calculated by subtracting variable costs from sales. The contribution margin income statement shows sales and variable expenses instead of the cost of goods sold. Fixed expenses are then subtracted from the contribution margin to determine the income.

The absorption costing income statement does not separate expenses into variable and fixed costs. Instead, it includes all manufacturing costs (direct materials, direct labor, variable manufacturing overhead, and fixed manufacturing overhead) in the cost of goods sold. Unlike variable costing, absorption costing records sales minus the cost of goods sold to show the company’s gross profit. Once gross profit is calculated, selling and administrative costs are subtracted to determine the income.

When units produced are equal to units sold, reported income is identical under both absorption costing and variable costing since all fixed costs are expenses under both methods. With both methods, the finished goods inventory is zero, and there are no manufacturing costs that are included in inventory accounts. All costs incurred are recorded as expenses and are deducted from net sales revenue on the income statement.

Below is a comparison between the income statement when variable costing is used and the same when absorption costing is used. We consider the scenario where units produced are equal to units sold.

EXAMPLE

We use the unit product costs that we calculated above: $18 for variable costing and $28 for absorption costing. In the current year, the company sold 60,000 units of inventory, had variable selling and administrative expenses of $2 per unit, and had fixed selling and administrative expenses of $200,000 per year.

If a company produces more units than it sells, the remaining units end up in the finished goods inventory. In this instance, income will be higher when absorption costing is used than when variable costing is used. This is because there is a difference in total expenses between the two methods.

EXAMPLE

In 2026, the company produced 60,000 units; however, it only sold 50,000 units, which means that 10,000 units were remaining in the company’s inventory at the end of the period. In the tables below, we will see the changes in the income statement when units remain in inventory.

When more units are sold than produced, operating income is less under absorption costing than it is under variable costing. The only way for a company to sell more units than what they produce is to sell some of the units that were already in inventory at the beginning of the year. With variable costing, the fixed manufacturing costs for the prior year were expensed in that year; therefore, only variable costs have been assigned to the units that remain. In this case, the unit product cost remains the same for all three years.

On the other hand, when absorption costing is used, the units in the beginning inventory have fixed manufacturing costs assigned to them. The units that are sold under absorption costing have a higher cost per unit, which increases the cost of goods sold and decreases operating income. The difference between the two methods is a result of the differences that show up when the fixed manufacturing overhead costs are expensed. When variable costing is used, the fixed manufacturing overhead costs from the prior period were expensed in the prior period, and therefore they are not reported in the current year's income statement. For absorption costing, the prior period's fixed manufacturing costs are attached to the beginning inventory and expensed in the current year.

EXAMPLE

In the third year, 2027, the company produced 60,000 units and sold 70,000 units, which included the 10,000 remaining units from 2026. In the income statements below, we will see the changes to the income statement when the company sold more units than they produced.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.