In this lesson, you will learn about the key risks in investing and understand why they are essential for making smart financial decisions. You’ll also learn about business cycles and how market booms and crashes affect the economy. Specifically, this lesson covers the following:

1. Inherent Risks in Investing

-

Just like a roller coaster has twists and turns, investing brings its own set of risks that everyone should know about. One of the biggest risks is market risk—when the overall market goes up and down based on things like economic changes, company performance, or even global events. If the market drops, the value of your investments can fall too, which might affect your financial plan if you’re relying on that money for a specific goal.

Then, there’s company-specific risk, which happens when a particular company you’ve invested in faces challenges, like management issues or product recalls. This might not affect the entire market, but it could still have a big impact on your investment in that company.

Understanding these risks is important because they remind us that investments won’t always go up. Planning for the inevitable ups and downs can help you create a financial plan that stays on track even when things get unpredictable. That’s why many people choose to spread out their investments across different companies—so that if one area struggles, the whole portfolio doesn’t take a hit. By knowing these risks ahead of time, you’re better prepared to handle the bumps and make smart choices that keep your financial goals in sight.

Let’s examine the most common types of risks in investing in more detail.

1a. Market Risk

Market risk refers to the possibility that your investment will lose value due to economic conditions such as inflation, recessions, and changes in interest rates. Market risk is unavoidable as it impacts almost all investments.

-

EXAMPLE

A recent event of market risk happened during the COVID-19 pandemic in 2020. When the pandemic hit, it created a lot of uncertainty, and people started pulling money out of the market. Within weeks, the value of most stocks dropped sharply as businesses closed, jobs were lost, and the economy slowed down. Even strong companies that were doing well before COVID saw their stock prices fall just because the entire market was affected by the crisis.

Think about it like this: Imagine you invested in a popular tech company or a big retailer that seemed like a safe choice. Despite the company being strong, its stock price still dropped because the whole market was reacting to COVID-19. This is market risk—the idea that even good investments can lose value when something big happens to the economy.

The COVID-19 market crash reminded us that it’s smart to be prepared for surprises. Even if you’ve picked strong investments, market risk can affect them all at once, and being diversified can help cushion the impact.

-

- Market Risk

- The chance that the overall value of investments, like stocks or bonds, will go down due to changes in the economy or events that affect the entire market.

1b. Sector Risk

Sector risk applies to industries like technology, health care, or energy, which may go through periods of significant disruption and change. If an entire sector struggles due to specific challenges, investments in that sector can underperform, causing a decline in the stock’s value.

-

EXAMPLE

In 2015, the energy sector experienced a downturn when oil prices collapsed. Investors who had invested heavily in energy companies saw significant losses, even though other sectors performed well during that same time.

The energy sector did eventually recover after the 2015 crash, but it took time. When oil prices dropped, energy stocks fell hard, and it took a while for them to bounce back as oil prices slowly improved. This is a reminder that some sectors can be riskier than others, and not every investment recovers quickly.

Here’s a quick look at different types of sectors to help you understand:

- Sectors like health care, utilities (electricity and water), and consumer staples (things we buy regularly, like food or toothpaste) tend to be more stable. People need these products and services no matter what’s happening in the economy, so these sectors don’t usually drop as much in downturns. They’re often seen as safer bets.

- Sectors like energy, technology, and financials are more “up and down.” They do well when the economy is strong but can struggle in tough times. For example, energy companies are affected by changes in oil prices, and tech companies can be hit when people spend less.

Many investors like to spread their money across different sectors to balance out the risks. That way, if one area (like energy in 2015) goes down, other areas (like health care) might stay steady, helping keep your overall investments from losing too much value.

-

- Sector Risk

- The risk that investments in a specific industry will lose value if that entire sector faces challenges, like new regulations or declining demand.

1c. Stock-Specific Risk

Stock-specific risk, also called company risk, relates to the performance of an individual company. If a company experiences internal problems like leadership changes, product failures, or lawsuits, it can cause its stock to drop, regardless of what’s happening in the general market.

-

EXAMPLE

Imagine you’ve invested in a popular coffee company called BeanCo. One day, BeanCo has to recall thousands of its coffee products due to a quality issue. This recall costs the company a lot of money, makes customers hesitant to buy their products, and affects their reputation. As a result, BeanCo’s stock price drops.

This is a stock-specific risk because it only affects BeanCo and no other companies in the coffee industry or the broader stock market. If you had invested only in BeanCo, you’d feel the full impact of this drop. But if you had investments in other companies, like a tech company or a retail store, those stocks wouldn’t be affected by BeanCo’s recall.

-

- Stock-Specific Risk

- The risk that a particular company’s stock will drop in value due to issues unique to that company, like poor management or product recalls.

1d. Liquidity Risk

Liquidity risk is the risk that you won’t be able to quickly sell an investment without losing value. Highly liquid assets, like shares of large and recognized companies, can usually be sold easily at market price. However, some investments, like real estate or shares in small companies, may be harder to sell quickly.

-

EXAMPLE

Imagine you own a rare collectible car that’s worth a lot of money—let’s say $50,000. This car is valuable, but it’s not something you can sell quickly like you would with cash or stocks. If you suddenly need cash for an emergency, you might struggle to find a buyer right away or may have to sell it for less than it’s worth just to get cash quickly.

This represents liquidity risk. Liquidity risk is the chance that you won’t be able to quickly sell an asset for its full value when you need cash. Some investments, like real estate or collectibles, are harder to sell quickly. Cash and stocks, on the other hand, are easier to turn into cash quickly.

-

- Liquidity Risk

- The risk of not being able to sell an investment quickly for its full value, especially in an emergency, like trying to sell property or rare collectibles.

1e. Inflation Risk

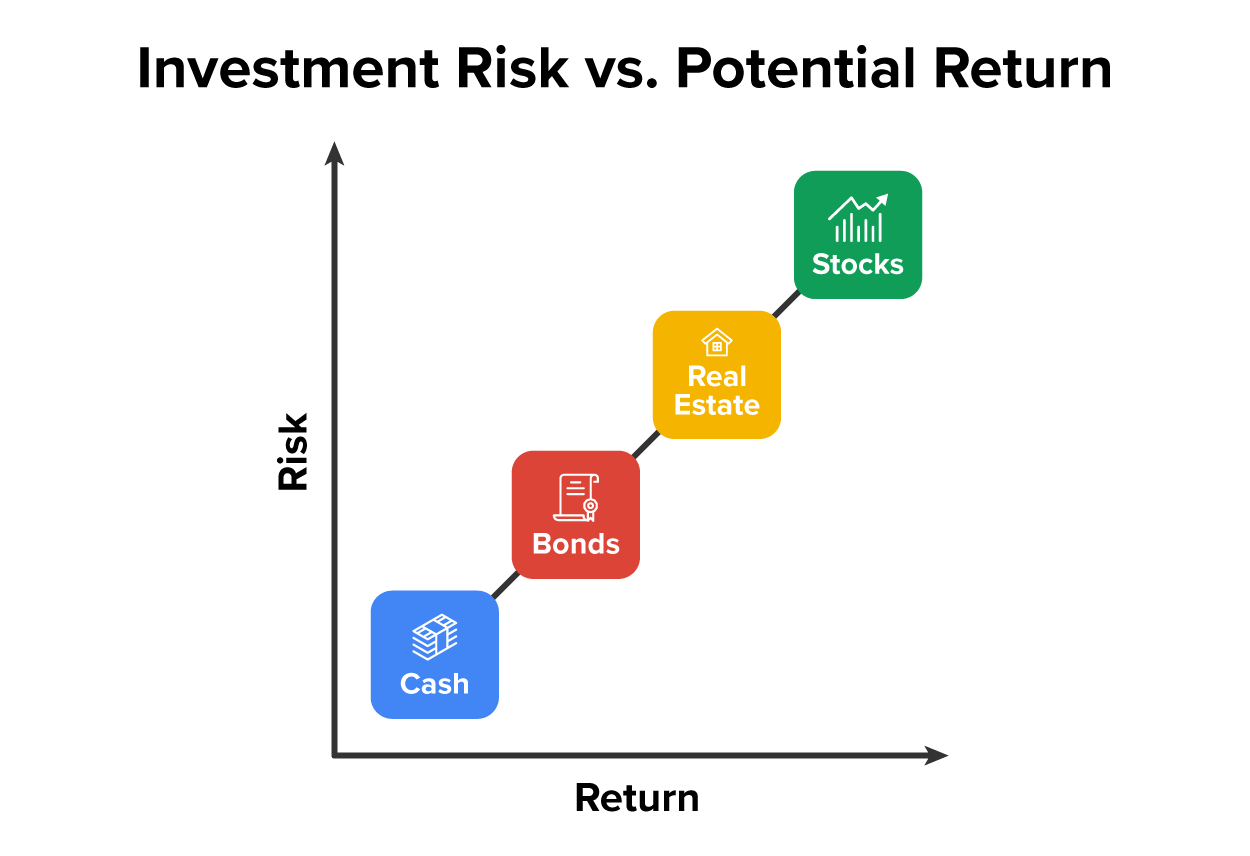

Inflation risk occurs when the return on your investment doesn’t keep up with inflation. When this happens, you have less purchasing power. This risk is particularly relevant for investments that have fixed returns, like bonds, which may not rise in value fast enough to outpace inflation. For reference, bonds are loans you give to a company or government. In return, they pay you back with interest over time. It’s a way to earn steady returns, usually with less risk than stocks. We’ll learn all about them in an upcoming lesson.

-

EXAMPLE

Imagine you have $1,000 saved up, and you plan to use it in the future to buy a new laptop. But over the next few years, prices went up because of inflation, and the laptop that cost $1,000 now costs $1,200.

This is inflation risk—the chance that the money you save now won’t be able to buy as much in the future because prices have increased. Inflation risk means your savings might lose buying power over time if they don’t grow at the same rate as inflation.

-

- Inflation Risk

- The risk that rising prices over time will reduce the purchasing power of your money, meaning your savings may buy less in the future.

2. What Investment Risk Means to You

Understanding the risks of investing is like knowing the rules of a game before playing it. When you recognize different risks, you can make smarter financial choices.

-

EXAMPLE

If you know that certain industries are more volatile and subject to stock market swings, you might avoid putting all of your money in that certain sector. Knowing about company-specific risk means you won’t panic if one stock in your portfolio drops—you’ll recognize it as a normal part of investing. In the end, being aware of these risks helps you stay levelheaded, avoid rash decisions, and keep your investments on track even when the market gets rocky. It’s all about taking control and setting yourself up for long-term success.

-

Understanding these risks is like having a map to navigate your financial future. When you know what could go wrong with different types of investments, you’re better prepared to make smart decisions and avoid surprises.

- For example, if you’re thinking about investing in a popular industry, like tech, knowing about sector risk helps you understand that if the tech industry hits a rough patch, your investment might take a hit. This way, you don’t put all your money in one basket and can spread it across other sectors to protect yourself.

- Knowing about stock-specific risk is also important. Imagine investing heavily in a single company because it seems like a safe bet. But if that company runs into trouble—like a major product failure—your investment can lose value quickly. Understanding this helps you see why investing in a few different companies can lower your risk.

- Liquidity risk is key for big purchases or emergencies. Let’s say you have a rare item worth a lot of money, but if you suddenly need cash, selling it could be tough. By recognizing liquidity risk, you know it’s smart to have some money in easily accessible forms, like savings, so you don’t end up stressed in a pinch.

- Finally, inflation risk reminds you that the money you save today might not buy as much in the future. Knowing this helps you plan to invest some of your savings in options that have a chance to grow, so your money keeps up with rising costs.

Understanding these risks makes you a smarter planner, helping you avoid big setbacks and keep your financial goals on track, even when the unexpected happens. It’s like having a toolkit to build a solid, balanced financial future!

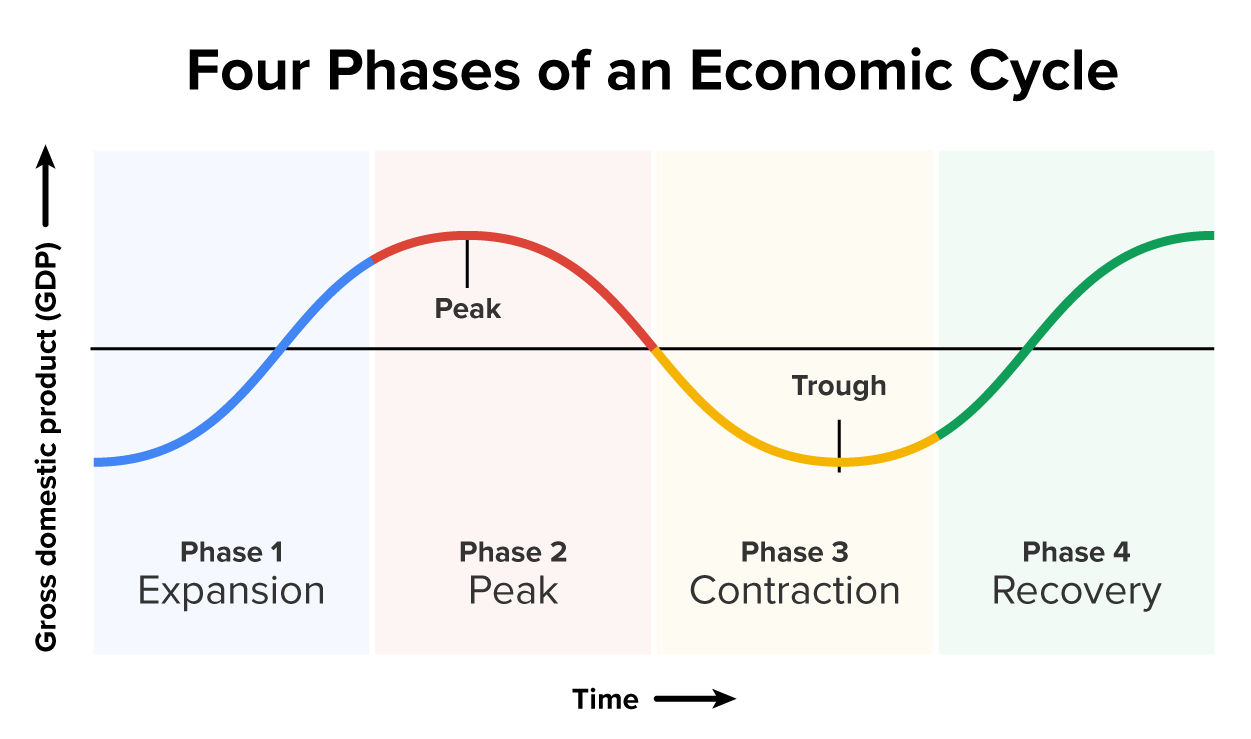

3. Business Cycles

Understanding risks is key to managing your investments, but it’s also important to see how these risks interact with the bigger picture—the business cycle. Business cycles are the natural ups and downs of the economy, moving through periods of growth and decline. These cycles influence all types of risk: During a downturn, market and sector risks are often higher, while inflation risk might decrease as prices stabilize.

By knowing how business cycles affect risk, you can make smarter choices about when to invest, save, or adjust your financial plan. Let’s dive into how these cycles work and how they shape the risks we face.

There are four main business cycles, just like seasons.

- During the expansion phase, the economy is growing, people are spending money, businesses are hiring workers, and investments tend to perform well.

- Then comes the peak, where everything starts to slow down, signaling the economy may have reached its highest point for a while.

- After that, we enter a contraction (or recession), where the economy shrinks, unemployment rises, and investments often lose value.

- Finally, at the trough, the economy bottoms out and begins to recover, setting the stage for the next expansion.

Understanding these cycles can help you manage your investments better. Knowing where we are in the cycle allows you to make smarter decisions—whether you’re being cautious of your spending during peaks or looking for investment opportunities during recoveries.

To get a sense of where you are in the business cycle and how it impacts your finances, start by looking at things like job availability, consumer spending, and inflation in the news or reports. If people are spending a lot and prices are going up, we’re probably in a growth phase; if layoffs are common and people are spending less, it might be a downturn.

Here are some relatable questions to ask yourself to see how the business cycle affects your money:

- Is my income steady? If you’re in a stable job, you might feel comfortable investing during any phase. But if your income depends on the economy, like in sales or hospitality, you might want to save more during uncertain times.

- How comfortable am I with risk? Some people see downturns as a chance to invest while prices are low. Others prefer to play it safe until things feel more stable. Knowing your own comfort with risk helps guide you when to buy, hold, or wait.

- Am I noticing higher prices? Inflation often goes up in growth periods, which can make everyday expenses harder to manage. If prices are rising, it might be time to investigate investments that help keep your savings’ value steady.

- What are my financial goals right now? Different phases suit different goals. For example, a growth period might be a good time to invest for the long term, while in a downturn, building an emergency fund could be the smart move.

By thinking about these questions and paying attention to where we are in the business cycle, you can make financial choices that feel right for you, no matter what phase we’re in.

-

- Business Cycles

- The regular ups and downs in economic activity over time, including periods of growth (expansion) and decline (recession).

- Expansion

- A period in the business cycle when the economy is growing, with rising production, employment, and spending.

- Peak

- A point in the business cycle when economic growth reaches its highest level before slowing down or declining.

- Contraction

- A period in the business cycle when the economy slows down, with decreases in production, employment, and spending.

- Trough

- The lowest in the economy during a business cycle before it starts to grow again, marking the end of a contraction.

4. Market Booms and Crashes

-

Imagine the stock market as a party—when things are good, everyone’s having fun, the music’s loud, and people are pouring in, expecting the good times to last forever. But just like any party, things can get out of hand quickly. Suddenly, the music stops, the lights come on, and people scramble to leave, realizing the excitement was not all it was cracked up to be. This is what happens during a market boom and crash.

Understanding business cycles gives us a clearer view of the wild swings that sometimes happen—market booms and crashes. While business cycles move up and down gradually, booms and crashes are those big, sudden changes that can shake things up quickly. Learning how these intense highs and lows fit into the bigger economic picture helps you know what to expect and how to handle your money if the market suddenly soars or takes a dive.

A market boom is when stock prices rise quickly, fueled by excitement and optimism. Everyone wants to buy this stock, and it seems like the sky’s the limit. But booms can’t last forever. Eventually, the market gets too hot—prices rise too high, and reality sets in. That’s when the market crash happens. The bubble bursts, prices drop, and panic sets in as investors rush to sell, trying to get out before losing more money. An example of a market crash is when the stock market took a big hit in August 2024, with the Dow dropping 1,000 points in one day—its worst fall since 2022. This crash was part of a global market dip, sparked by worries about a slowing U.S. economy.

The next day, the market bounced back a bit, showing just how quickly things can change. This event reminds us that markets can be unpredictable, and having a mix of investments can help protect you when sudden drops happen.

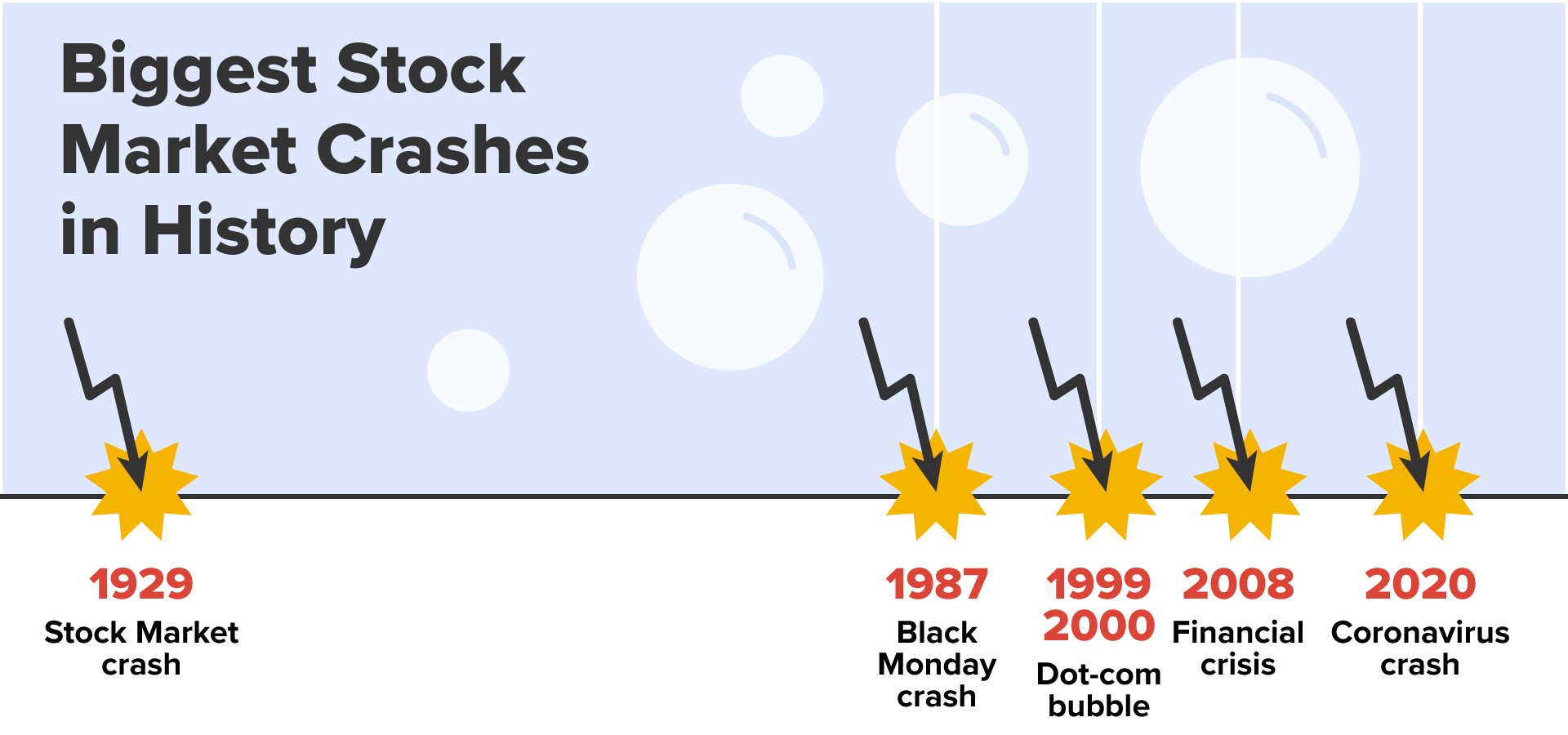

Two famous examples of this are the stock market crash of 1929 (Black Friday) and the dot-com bubble in the early 2000s.

-

Black Friday Stock Market Crash

The 1920s were a period of economic prosperity in the United States, often called the “Roaring Twenties.” However, stock prices inflated due to excessive speculation and

margin trading (borrowing money to invest in stocks). On October 29, 1929, known as Black Friday, the stock market crashed, erasing billions of dollars in wealth and contributing to the

Great Depression.

The Dot-Com Bubble

In the late 1990s, long before Facebook and Google existed, internet companies were the future, and investors poured money into tech stocks. However, many companies were overvalued and had no real business model. By 2000, the bubble burst, and the NASDAQ, home to many tech stocks, lost almost 80% of its value over 2 years.

-

- Market Boom

- A period of rapid growth in the stock market, with rising prices, high investor confidence, and increased trading activity.

- Market Crash

- A sudden and severe drop in stock prices, often due to panic selling, leading to significant losses in market value.

- Margin Trading

- When you borrow money from a broker to buy more stocks than you could with just your own cash.

- Great Depression

- A severe worldwide economic downturn in the 1930s, marked by massive unemployment, business failures, and widespread poverty.

In this lesson, you learned how investing comes with inherent risks. You also learned about the different types of risks in investing, including market, sector, liquidity, inflation, and stock-specific risks, and why understanding what investment risk means to you is crucial for making sound financial decisions. You also explored how the economy moves through business cycles and how these cycles impact your investments. Additionally, you learned about the causes and consequences of market booms and crashes.