-

In this lesson, you will learn what bonds are and the different types of bonds. Specifically, this lesson will cover the following:

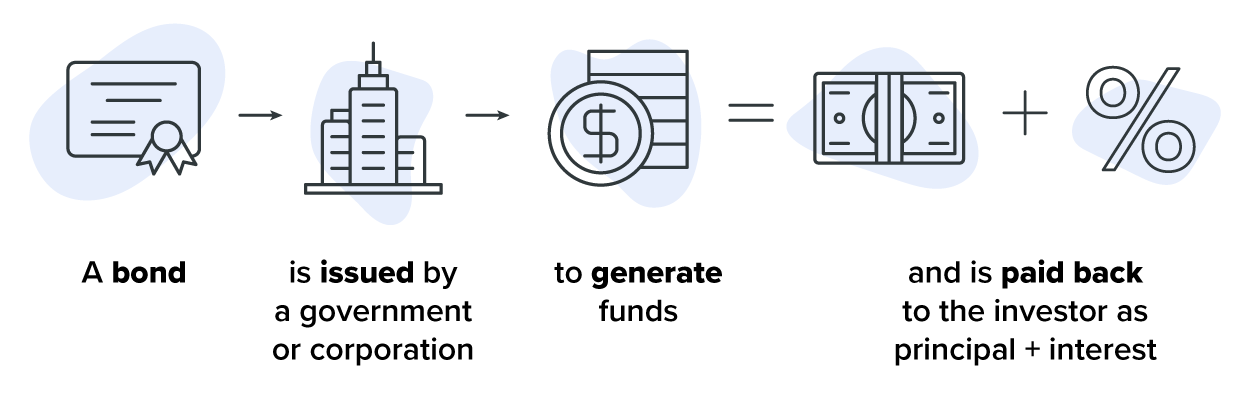

1. What Is a Bond?

Investing can feel overwhelming, but it doesn’t have to be. If you’ve ever felt like the stock market is too risky, bonds might be your new best friend. Bonds are often considered a safer investment than stocks because they provide a steady, predictable income. They can be a great way to diversify your portfolio and reduce risk while still growing your money over time.

But what exactly are bonds, and how do they work? Let’s break it down in the simplest way possible so you can decide if they’re right for you.

Bonds are a type of investment where you lend money to an entity—like a company, a city, or the federal government—in exchange for interest payments over time and the return of your original investment (called the principal) when the bond matures.

-

EXAMPLE

Imagine your friend wants to open a small bakery but doesn’t have enough money to get started. They ask you to lend them $1,000 and promise to pay you back in 5 years. To thank you for the loan, they also agree to pay you $50 each year as a token of appreciation for your help. That yearly $50 payment is like the interest you earn from a bond, and the $1,000 you get back after 5 years is your principal.

Bonds work in the same way, just on a much larger scale with companies, cities, or governments borrowing money from investors like you.

When you buy a bond, you’re making a loan for a fixed period of time (called the maturity date). In return, you earn interest payments (known as the coupon rate) at regular intervals—often yearly or twice a year. The longer you hold the bond, the more interest payments you’ll receive.

Here are the key parts of a bond:

-

Face value (principal): This is the amount you lend and will get back at maturity. Most bonds have a face value of $1,000.

-

Coupon rate: This is the fixed interest rate that the bond pays annually (e.g., 5% means you get $50 per year on a $1,000 bond).

-

Maturity Date: This is the date when the bond’s principal is repaid to you. Bonds can mature in just a few months or take decades.

- Issuer: This is the entity borrowing money—this could be a corporation, a city, or the federal government.

-

Yield: This is the return you earn from the bond based on its price and interest payments. If bond prices go up or down, the yield changes too.

-

EXAMPLE

Let’s say you invest in a 10-year bond with a 5% coupon rate and a $1,000 face value. Here’s how it works:

Every year, you receive $50 in interest payments ($1,000 (face value) x 5% (coupon rate).

After 10 years, you also get back your $1,000 principal.

If you want to sell the bond before it matures, the price of your bond may have gone up or down, depending on interest rates and market conditions.

If you hold a bond until maturity, you’ll get its full face value, no matter how its price has changed over time. However, if you sell before maturity, the price may be higher or lower depending on the interest rates and market conditions.

-

- Annual Interest Bond Payment

-

Let’s put your knowledge to the test! Imagine you are investing in a bond and want to figure out how much interest you’ll earn.

You decide to invest in a corporate bond with the following details:

- Face value: $1,000

- Coupon rate: 4%

- Maturity: 5 years

Question 1. Calculate your yearly interest payment.

- a. Use the annual interest bond payment formula:

- b. How much will you receive each year?

Answer:

Question 2. Find out your total interest earned over 5 years.

- a. Multiply the annual interest by the number of years the bond is held.

- b. How much money will you have made just from interest by the time the bond matures?

Answer:

Now that you understand how bonds work, you might be wondering, “Are all bonds the same?” Not quite! There are different types of bonds, each with its own risk level, interest rate, and purpose. Some are backed by the government, making them ultrasafe, while others come from companies and offer higher returns but with added risk.

Let’s take a look at the different types of bonds so you can choose the right one for your investment goals.

-

- Bond

- A loan you give to a government, company, or city in exchange for interest payments and the return of your money later.

- Face Value (Principal)

- The amount of money you lend and will get back when the bond matures.

- Coupon Rate

- The fixed interest rate a bond pays each year.

- Maturity Date

- The date when the bond’s principal is repaid to you.

- Yield

- The return on a bond based on its price and interest payments.

2. Types of Bonds

Bonds come in different varieties, each serving different purposes and offering various levels of risk and reward. Some bonds are as safe as putting money in a savings account, while others offer higher returns but come with more risk. Let’s break them down into easy-to-understand categories so you can figure out which might be a good fit for your financial goals.

1. Government Bonds (Treasury Bonds)

- Best for: Investors who want a safe, steady return with little risk.

- Government bonds are issued by the U.S. Treasury and are considered one of the safest investments because they are backed by the government. If you’re looking for a way to grow your money without much risk, these could be a good option.

-

The U.S. Treasury is the government department responsible for managing the country’s finances. It collects taxes through the IRS, prints money, and oversees the U.S. Mint. It also issues Treasury bonds, notes, and bills to borrow money for government spending. These bonds help fund programs like Social Security, infrastructure, and national defense. The Treasury ensures the government can pay its bills and manages the national debt. Investors, banks, and foreign governments buy Treasury bonds because they are considered a safe investment backed by the U.S. government.

- Types of Government Bonds:

-

Treasury Bills (T-Bills): These are short-term bonds (1 year or less). Instead of paying interest, they are sold at a discount. For example, you buy a T-bill for $950, and when it matures in a year, you get $1,000—the difference is your profit.

-

Treasury Notes (T-Notes): These are medium-term bonds (2–10 years) that pay interest every 6 months.

-

Treasury Bonds (T-Bonds): These are long-term bonds (10–30 years) that also pay interest twice a year.

-

Series I Savings Bonds: Designed to protect against inflation by adjusting their interest rate based on inflation levels. Series I savings bonds have a maturity date of 30 years from the issue date. However, you can cash them in after 12 months, but if you redeem them before 5 years, you’ll lose the last 3 months of interest as a penalty.

-

EXAMPLE

If you invest in a 10-year Treasury note with a 3% coupon rate, you will receive $30 per year in interest for 10 years. At the end of 10 years, you also get back your original investment.

2. Municipal Bonds (Munis)

- Best for: Investors who want tax-free income and are comfortable with a bit more risk than government bonds.

-

Municipal bonds (or “munis”) are issued by cities, states, or local governments to fund public projects like schools, roads, or hospitals. The big advantage? The interest you earn is usually tax-free at the federal level and sometimes at the state level, making them a great option for people in higher tax brackets.

-

EXAMPLE

A city issues a municipal bond with a 4% coupon rate to build a new park. If you invest $5,000, you earn $200 per year tax-free plus your $5,000 back when the bond matures.

-

Municipal bonds can be a great way to earn tax-free interest, but they come with some added risks. Unlike U.S. government bonds, they depend on state or local governments to pay you back, which means there’s a chance of default if the government struggles financially. Also, if interest rates rise, the value of your bond may drop if you need to sell before maturity. For example, during the COVID-19 pandemic, some cities faced major budget shortfalls due to lower tax revenue, raising concerns about their ability to repay municipal bondholders. Always check the bond’s rating and the financial health of the issuer before investing.

3. Corporate Bonds

- Best for: Investors who want higher returns and are willing to take on more risk.

-

Corporate bonds are issued by companies looking to raise money for expansion, research, or other business needs. They usually offer higher interest rates than government or municipal bonds but come with more risk—if the company goes bankrupt, it may not be able to pay back its bondholders.

- Types of Corporate Bonds:

-

Investment-grade bonds: These are issued by financially strong companies (lower risk, lower return).

-

Junk bonds (high-yield bonds): These are issued by companies with lower credit ratings (higher risk, higher return).

-

EXAMPLE

A tech company issues a corporate bond with a 6% coupon rate. If you invest $2,000, you will receive $120 per year in interest plus your $2,000 back at maturity.

4. Savings Bonds

- Best for: Individuals who are saving for the long term, such as for education or retirement.

- Savings bonds, like Series I bonds and Series EE bonds, are issued by the U.S. Treasury. They grow in value over time and are meant to be held for many years. They don’t pay out regular interest like other bonds, but they do increase in value over time, making them great for long-term savings goals.

-

EXAMPLE

You buy a Series I bond for $500, and after 20 years, it has grown to $1,200, thanks to interest and inflation adjustments.

5. International Bonds

- Best for: Investors looking for global diversification and willing to take on currency risk.

-

International bonds are issued by foreign governments or companies. While they can offer good returns, they come with extra risks—like changes in currency value. If the U.S. dollar strengthens, your returns could be worth less when converted back to dollars.

-

EXAMPLE

You invest in a Japanese government bond and earn 2% interest per year. However, if the value of the Japanese yen falls compared to the U.S. dollar, the money you receive back may be worth less when exchanged. You can exchange the bond for cash at any time by selling it on the market, but its value will depend on the interest rates, market conditions, and currency exchange rates. If you hold the bond until maturity, you will receive the full face value in Japanese yen, but if the yen has weakened against the U.S. dollar, your returns can be worth less when converted.

-

Here is a video that discusses the five common types of bonds:

Now that you know the different types of bonds, the next step is figuring out which one fits your financial goals.

- If you want low risk and security, government bonds might be your best bet.

- If you like tax-free income, municipal bonds could work for you.

- If you want higher returns and can handle some risk, corporate bonds may be appealing.

- If you’re saving for the long term, savings bonds are a great option.

- If you want to diversify globally, international bonds can add variety to your investments.

-

Buying bonds is simple! Here are the easiest ways to get started:

- U.S. Treasury Bonds (Safest Option)

- Buy directly from TreasuryDirect.gov (no broker needed). Remember, a broker is a person or company that helps you buy and sell investments like stocks and bonds.

- Choose T-Bills, T-Notes, T-Bonds, or Series I Bonds.

- Pay from your bank and get interest automatically.

- Municipal and Corporate Bonds

- Buy through a broker (Fidelity, Vanguard, or Schwab).

- Search for bonds from cities, states, or companies.

- Get interest payments until the bond matures.

- Bond Mutual Funds and ETFs (Easiest for Beginners)

- Buy a bond fund through a broker.

- Invest in multiple bonds at once for diversification.

Which is best?

- For safety, go with Treasury bonds on TreasuryDirect.gov.

- For higher returns, try corporate or municipal bonds through a broker.

- For easy investing, pick a bond mutual fund or ETF.

No matter which type of bond you choose, they can all be valuable tools to balance your portfolio, reduce risk, and create a steady stream of income. The key is to align your bond investments with your financial goals and risk tolerance.

-

- Government Bonds (Treasury Bonds)

- Bonds issued by the government and considered low-risk investments.

- U.S. Treasury

- The department that manages government money and issues Treasury bonds.

- Treasury Bills (T-Bills)

- Short-term government bonds (mature in a year or less), sold at a discount instead of paying interest.

- Treasury Notes (T-Notes)

- Government bonds that last 2–10 years and pay interest twice a year.

- Treasury Bonds (T-Bonds)

- Long-term government bonds (10–30 years) with interest paid twice a year.

- Series I Savings Bonds

- Government bonds that adjust for inflation to protect your money’s value.

- Municipal Bonds

- Bonds issued by cities and states to fund public projects, often with tax-free interest.

- Corporate Bonds

- Bonds issued by companies to raise money, usually paying higher interest than government bonds.

- Investment-Grade Bonds

- Safer corporate bonds issued by financially strong companies, offering lower returns.

- Junk Bonds (High-Yield Bonds)

- Riskier corporate bonds that pay higher interest.

- Series EE Bonds

- Long-term savings bonds that earn interest over time and are backed by the U.S. government.

- International Bonds

- Bonds issued by foreign governments or companies, offering diversification but with currency risk.

In this lesson, you learned all about what bonds are, how they work, and the different types of bonds.