Many companies offer retirement plan benefits to employees. These plans may be qualified or nonqualified. Let’s examine the differences between the two.

The primary difference between qualified employer-sponsored plans and nonqualified plans is the way they are treated for tax purposes. Qualified plans receive more favorable tax treatment because they meet the requirements of both of the following:

A nonqualified plan is basically the opposite of a qualified plan. Nonqualified plans do not meet the requirements of IRC §401(a) and ERISA and do not qualify for favorable tax treatment.

Nonqualified plans are:

Employers are generally not eligible to deduct contributions to nonqualified plans until the employee takes a withdrawal.

We do not cover nonqualified plan contributions in this course.

Qualified plans offer several tax advantages. Employers who offer qualified plans to their employees benefit by being able to deduct the annual allowable contributions they make for each plan participant.

Participating employees enjoy the following tax benefits:

EXAMPLE

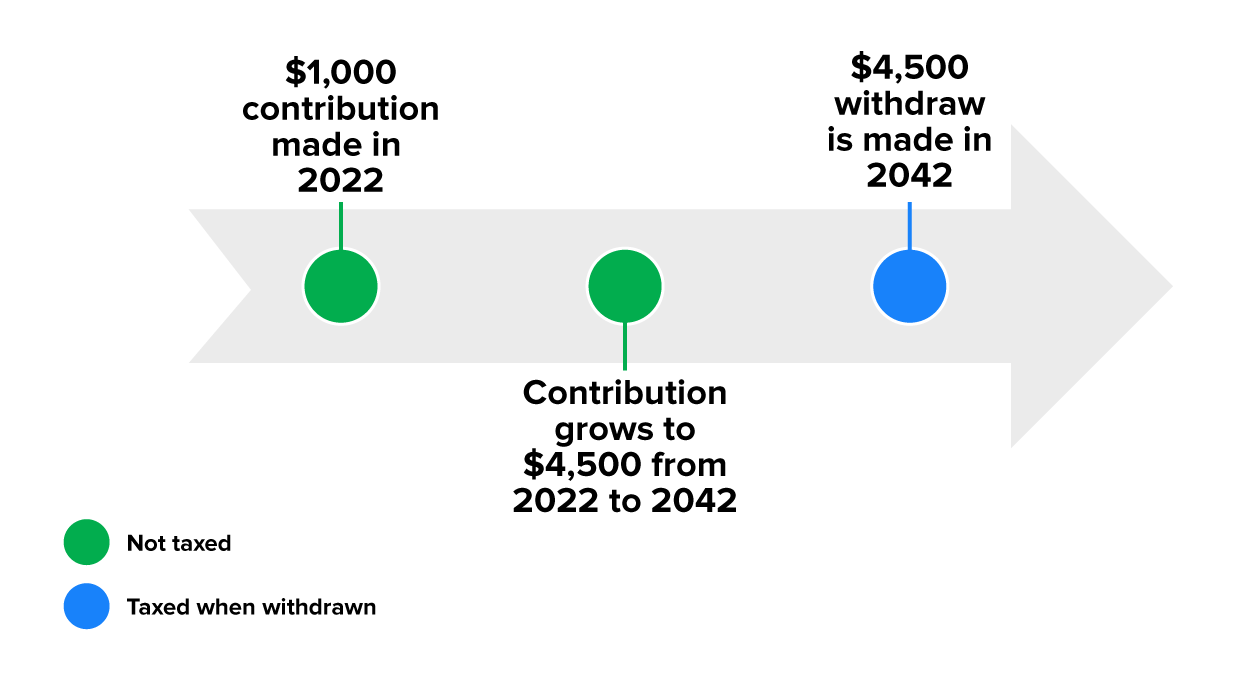

Bertha contributes $1,000 during the year to her employer’s qualified retirement plan. The $1,000 she contributed will not be included in her taxable income. Rather, the income will be taxed when she starts to withdraw money from the retirement plan, so the tax on the $1,000 income is deferred, i.e., tax-deferred.

There are two kinds of qualified plans—defined benefit and defined contribution.

A defined benefit plan is a retirement plan in which the employee receives a predetermined, formula-based benefit at retirement. The most common type of defined benefit plan is a pension, in which the retirement benefit is calculated using a formula based on the number of years worked, the taxpayer’s age, and the taxpayer’s history of earnings with the employer. Another type of defined benefit plan is an annuity. An annuity is a series of payments under a contract, made at regular intervals over a period of more than one year. The taxpayer can buy the annuity contract alone or with the help of their employer. Annuities are often purchased from life insurance companies. For these types of retirement accounts, generally, the employer or employee makes payments to fund the pension or annuity.

A defined contribution plan (also called a deferred compensation plan) is a retirement plan in which the employee or employer makes pretax contributions into a retirement account where the contributions and earnings grow tax-deferred until the money is withdrawn. The most commonly known type of deferred compensation plan is a 401(k). The following information provides more details about 401(k) plans and other common types of deferred compensation plans.

The 401(k) plan takes its name from IRC §401(k), which governs its existence. As a qualified plan, the 401(k) offers the tax-deferred advantages mentioned above.

In addition to the contributions the employee makes, the employer can also contribute to the employee’s account.

The employer may opt to match all or part of the employee’s contributions to the account.

This may be done by:

EXAMPLE

Ted’s employer offers its employees a 401(k) plan. The employer offers a matching contribution for each percent the employee contributes, up to 5%, of their annual salary to the plan.A 403(b) plan is a tax-advantaged retirement savings plan available for employees of the following types of organizations:

Note: Technically, 403(b) plans are not qualified plans. However, their main features are identical to those of qualified plans. For our purpose, we are going to treat 403(b) plans the same as a qualified plan.

457 plans are tax-advantaged, deferred compensation retirement plans available primarily to government employees. These 457 plans are not qualified plans, but their primary features are identical to qualified plans. Contributions to the plan, and earnings on those contributions, are tax-deferred until the employee receives distributions from the plan.

As wonderful a deal as a deferred compensation plan is, employees are not allowed to contribute an unlimited amount to their plan. The IRS sets annual maximum limits on the amount that can be contributed. These amounts are indexed for inflation and generally rise each year. Taxpayers who exceed retirement contribution limits may be subject to penalties if the excess amount is not withdrawn by April 15th of the following tax year.

For 2022, the maximum annual allowable contribution is $20,500. Taxpayers aged 50 or older are allowed an additional “catch up” contribution of $6,500, for a maximum annual allowable contribution of $27,000.

Allowable contributions to plans are generally set as a percentage of an employee’s salary. Therefore, the maximum amount any one taxpayer can contribute is a function of both the maximum annual limit and the allowable percentage of salary that may be contributed.

EXAMPLE

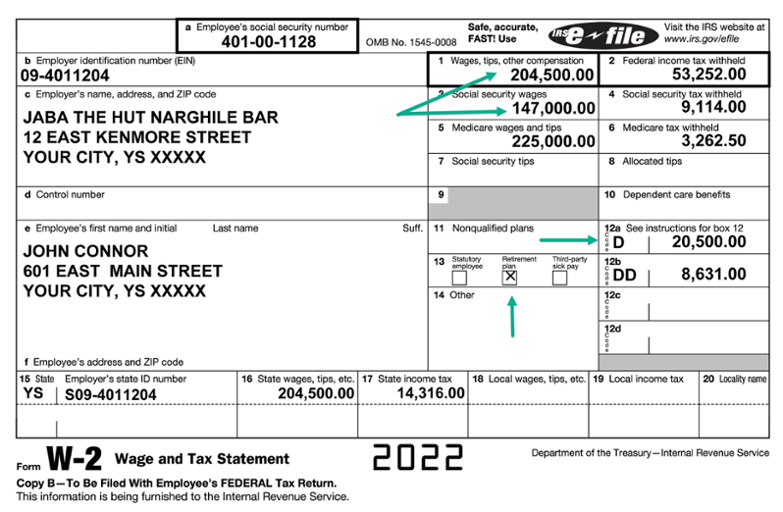

John Connor’s annual salary is $225,000. John is 47 years old. His employer sponsors a 401(k) plan, which allows each employee to contribute a percentage of their annual salary up to the IRS annual contribution limit. John wants to contribute 10% of his annual salary. His contribution will be limited since 10% of his annual salary is more than the $20,500 maximum allowable contribution ($225,000 × 10% = $22,500).Many contributions to deferred compensation plans are reported on the Form W-2 in box 12a.

The following illustration shows John Connor’s Form W-2 (from our earlier example). Notice the difference between the amount in box 1 and the amounts in boxes 3 and 5. The difference in box 3 is due to the limit on wages subject to Social Security tax, which in 2022 is $147,000. The $20,500 difference in box 5 is the amount John contributed on a tax-deferred basis to his 401(k) plan. The $20,500 401(k) contribution is reported in box 12 with the code D, and the retirement plan box is marked on John’s Form W-2.

See the list below of the box 12 codes. Note that codes D through H are all deferred compensation plans.