Table of Contents |

The trial balance is a list of the debit and credit balances of all the general ledger accounts at a given time.

The trial balance is used as a summary or a checkpoint that all of the account totals--all of the debits and credits--equal.

The trial balance is also used to identify any errors or inconsistencies in journalizing and posting. Did you make any errors? Did you miss anything through the journalizing and posting process? Do your debits not equal your credits?

The trial balance is also used to identify any balances that seem incorrect.

EXAMPLE

Suppose you have an understanding of the natural balances of your different types of accounts, and when looking at your trial balance, you notice that those accounts aren't fitting with your understanding of their natural balance. This might mean you need to dive deeper into that specific account and identify any potential issues.So, who uses the trial balance? Well, the trial balance is used exclusively by internal users; it is not provided to external users or for external reporting purposes.

There are two types of trial balances:

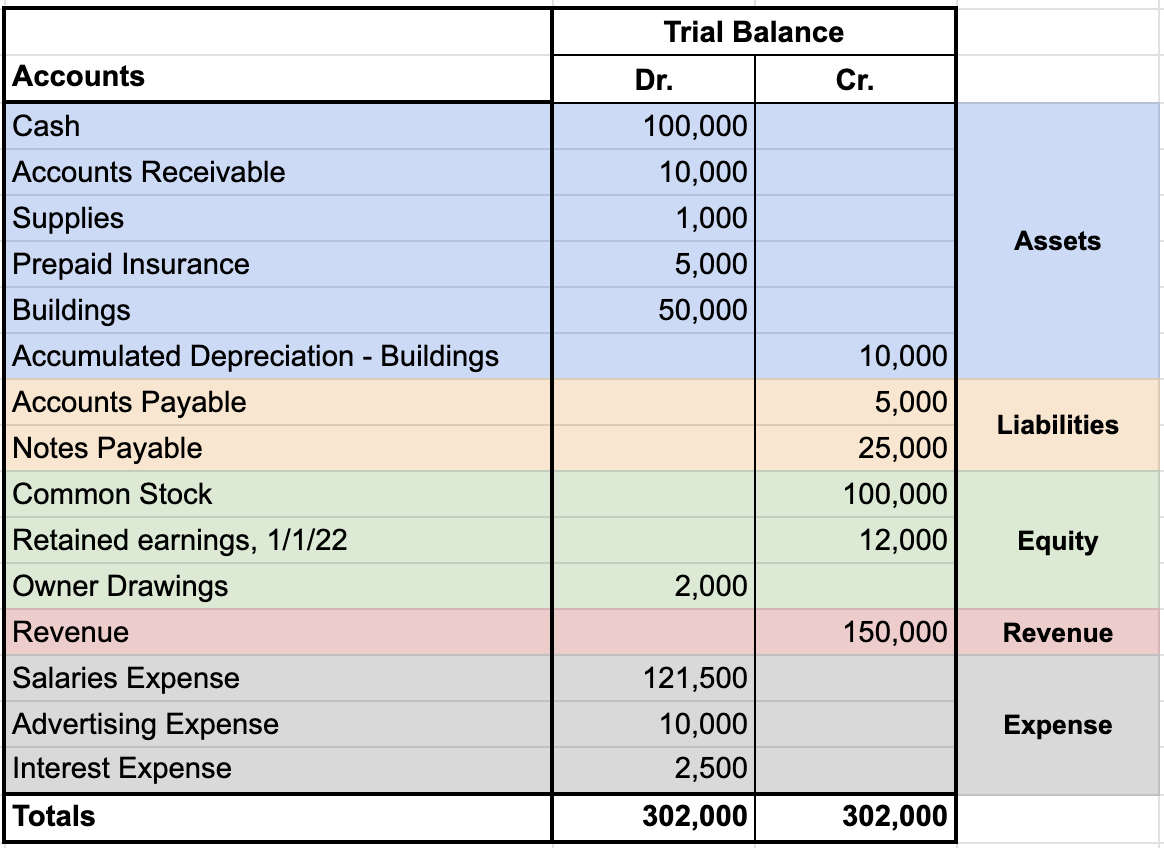

Let's look at an unadjusted trial balance worksheet example, below. Any trial balance worksheet starts with a list of all of the general ledger accounts, listed on the left side. Along with listing those general ledger accounts, the balance in each of those accounts is reflected, indicating whether it is a debit balance or a credit balance.

Next, we will examine the different account categories:

| Trial Balance Category | Description | Examples |

|---|---|---|

| Assets | Listed from most liquid (cash) to least liquid (in this case, buildings). This refers to how quickly an asset can be converted to cash. The natural balance of these asset accounts is a debit balance. | Cash, Accounts Receivable, Supplies, Prepaid Insurance, Buildings, and Accumulated Depreciation - Buildings |

| Liabilities | Listed in their correct order, from short-term to long-term. Liabilities have a natural credit balance, so you can see the credits reflected in the liabilities. | Accounts Payable and Notes Payable |

| Equity | Has a natural balance of credit, as is the case with the common stock and retained earnings. As you may recall, owner draws refers to when the owner pulls cash out of a business, so this is going to be a debit to the equity. | Common Stock, Retained Earnings 1/1/24, and Owner Drawings |

| Revenue | Has a natural credit balance | Sales |

| Expense | Has a natural debit balance. | Salaries Expense, Advertising Expense, and Interest Expense |

Source: THIS TUTORIAL WAS AUTHORED BY EVAN MCLAUGHLIN FOR SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.