Table of Contents |

Understanding the time value of money (TVM) is crucial for making informed financial decisions. At its core, the concept highlights how money today is worth more than the same amount in the future because of its earning potential. But why does this matter in our everyday lives? Let’s unpack this powerful idea and explore how you can harness it to achieve financial freedom.

Before we dive into the technical aspects, let’s start with a simple story.

Imagine someone offers you $1,000 today or $1,000 5 years from now. Which would you choose? Most of us would instinctively take the money today. Why? Because that $1,000 can be put to work. You could invest it, let it grow, and have more than $1,000 in 5 years.

This simple scenario captures the essence of TVM—money is worth more now because of its potential to grow and because it’s more reliable.

Now, let’s break it down:

Why It Matters:

1. Opportunity Cost

Think of opportunity cost as the cost of missing out on something you could have had, simply because you didn’t take action. Let’s say you have $100 right now. You have two choices:

If you invest that $100 today in something like a savings account or an investment earning 5% interest, by next year, your $100 will have grown to $105. That extra $5 is money you earned simply by letting your money sit and grow.

But if you decide to hold on to that $100 and wait a year before investing, you’re giving up the chance to earn that $5. It’s as if someone said, “Hey, here’s $5 for free,” and you said, “Nah, I’m good.”

So, the opportunity cost is not just about losing $5—it’s about what that $5 could have done for you in the long run. Because guess what? If you had invested the $105 (your $100 plus the $5 you earned) in the second year, it would earn even more interest—building a snowball effect.

EXAMPLE

Imagine you’re saving up for something fun, like a vacation. If you keep your money in a jar at home for a year, that’s fine—you’ll still have the same $100. But if you had put that $100 in an account that earned interest, you could have had $105. Now, that $5 might not seem like a big deal, but over time, this difference really adds up. It’s like your money is missing out on working shifts for you.2. Risk

Imagine this: Someone says, “I’ll give you $100 right now, no strings attached,” and someone else says, “I’ll give you $100 in a year, but trust me, it’ll be there.” Which sounds better? Most people would take the money now because it’s less risky.

Money you have in your hand right now is certain. You can see it, use it, and make it work for you immediately. Money promised in the future? Well, things could happen—a job might fall through, the deal might change, or they might simply forget. That future money is a promise, not a guarantee, and carries with it more risk.

Having cash now also gives you the power of choice. Let’s say you come across an opportunity, like investing in a business, snagging a property deal, or grabbing a once-in-a-lifetime vacation discount. If you have the money ready to go, you can jump on it. But if all you have is a promise of money in the future, you might miss out because you don’t have cash on hand when you need it.

EXAMPLE

Imagine you’re walking through your favorite store and you see a $300 gadget on sale for just $200 today. You’ve got $200 in your wallet, so you grab it, saving $100. But if you were waiting for payday or some money someone promised you in the future, you’d miss the sale and have to pay full price later—or not buy it at all. Having money now means you can act quickly and take advantage of the opportunity and not risk missing the sale.TVM is a powerful tool for prioritizing decisions. For example, should you pay off debt or invest? Should you splurge on something now or save for a bigger goal later? By understanding TVM, you can weigh these choices based on what will grow your wealth the most and make decisions that set you up for long-term success.

TVM gives you a powerful insight: The sooner you start using your money, the more it can grow. But how do we measure that growth? Think about it like planning a road trip—you need to know where you’re starting, where you want to end up, and how long it will take to get there. That’s exactly what future value helps with. It shows you the destination of your financial journey and helps you understand how today’s decisions can shape tomorrow’s outcomes. Next, we’ll explore how to calculate and use future value to turn your financial goals into reality.

Imagine you’re saving for a big goal, like buying your dream car or taking an unforgettable vacation. You’ve put some money aside but you’re curious: How much could it grow over time if you let it sit and earn more?

This is where future value (FV) comes in—it’s like a sneak peek into your money’s future. It tells you how much your savings could grow based on how much they earn, whether from a simple interest rate in a savings account or bigger returns from investing. The key is understanding how the growth rate (what your money earns) and the time you let it grow work together to make your dream savings a reality.

FV is a way to answer questions like, “If I invest $5,000 now, how much will I have in 10 years?” or “How much should I set aside today to reach my savings goal in the future?” By calculating FV, you can visualize the power of your money working for you—and it makes saving and investing feel more achievable. Let’s break down how it works and how you can use it to plan your financial journey.

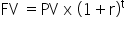

Using the FV formula above, let’s calculate the FV, or the amount grown by an interest rate over time to a later period, of a savings amount using 10% interest as an example. Although interest rates vary given current economic conditions, we will use 10% since the calculations are simpler.

EXAMPLE

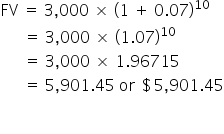

What is the value of an account at the end of 3 years that earns 10% compounded annually on $5,000 deposited today?

Let’s try some situations that you may want to consider yourself.

EXAMPLE

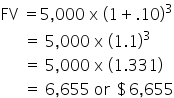

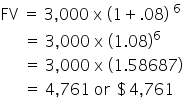

Take Alex, who is 25 years old and saved $3,000. He would like his savings to grow to $5,000 so he can return to community college part-time when his children attend elementary school in 6 years. What will Alex have in his savings account in 6 years if he figures he can earn 8% in a savings account at his local bank?

EXAMPLE

Saving for 10 years at 5% earns you more than saving for 5 years at the same rate.EXAMPLE

Saving for 5 years at 3% earns you less than saving for 5 years at 6%.Knowing how to calculate FV helps you set realistic savings goals and understand what your investments can achieve over time. It’s a tool to keep your financial plans grounded in reality while still inspiring action. Now that you know how to solve for FV, let’s learn how to solve for present value.

Imagine you know exactly how much money you’ll need in the future for a specific goal—whether it’s a dream vacation, a child’s college education, or even a down payment on a house. The big question becomes, how much do you need to save today to reach that goal? This is where present value (PV) comes into play.

PV is like reverse engineering your financial future. Instead of wondering whether you will have enough money later, you can confidently say, “Here’s what I need to set aside now to meet that goal.” It’s a powerful tool for planning and taking control of your finances.

PV determines how much a future sum of money is worth today. It’s like working backward to figure out what you need now to reach a goal later.

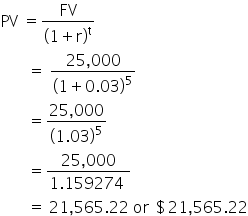

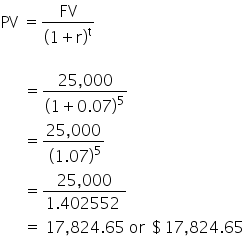

Imagine you want to buy a house and need $25,000 for a down payment in 5 years. Instead of saving bit by bit, you plan to invest a lump sum today that will grow over time. How much would you need to invest now to reach your $25,000 goal, assuming you could earn a 3% interest rate?

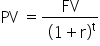

To calculate the PV, we adjust the formula for FV, which is as follows:

Now, to solve for PV, we rearrange the formula:

Using this formula, let’s say our annual rate of interest is 3%.

Using the PV formula:

To reach $25,000 in 5 years at a 3% annual interest rate, you’d need to invest $21,565.22 today.

PV helps you determine how much to save today to fund future expenses—such as a car, a home, or retirement.

PV is the ultimate planning tool. It reminds you that starting now, even with smaller amounts, can make big dreams attainable.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.

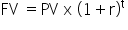

Where:

FV is the future value

PV is the present value (this is simply the amount of money you’re starting with today, which will grow into the FV based on the interest rate and time)

r is the annual rate of interest as a decimal (5% is .05)

t is the number of years your money is invested

Note: The “t” or time value is an exponential value

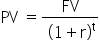

Where:

FV is the future value

PV is the present value

r is the annual rate of interest as a decimal (5% is .05)

t is the number of years your money is invested

Note: The “t” or time value is an exponential value