In this lesson, you will learn how to calculate and interpret the weighted average cost of capital (WACC) and why it serves as a critical benchmark for investment decisions. You’ll explore how internal and external factors, market conditions, and risk adjustments influence WACC and how businesses use it to evaluate profitability. Specifically, this lesson will cover:

1. Weighted Average Cost of Capital

Organizations have options available when it comes to finding funding for their operations. They can choose from debt options, such as taking out loans or offering long-term corporate bonds, or equity financing, such as preferred and common stock. Larger organizations tend to find a balance that is optimized for the best possible weighted average cost of capital (WACC) so they can operate at the scale that creates the best revenue opportunity.

-

In short, the WACC is a measure of what all capital inputs will cost the organization in terms of an average interest rate.

WACC is an extremely useful calculation for a business. It shows management the overall cost of borrowing capital. Depending on what a business is trying to calculate, the WACC can then be used as the minimum required return on any new operation or as the discount rate when calculating the net present value of an investment.

-

If the WACC is 8%, and a new project creates a 10% return, an organization can confidently borrow capital to fund its project. If the project only produces an 8% return, the firm will have a difficult decision to make. If the project returns 6%, it is quite easy to strategically argue against the new project.

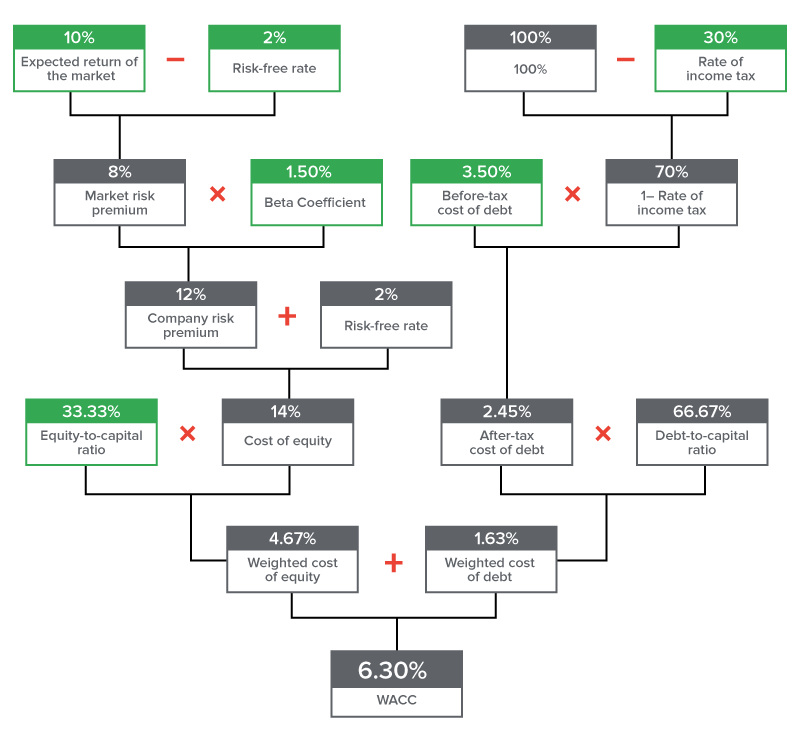

As you have previously learned, the equation for the weighted average cost of capital is:

To determine the WACC, the cost of debt and the cost of equity must be calculated.

-

In a previous lesson, you calculated the cost of debt after tax as:

And you calculated the cost of equity using the CAPM model as:

The cost of debt  is usually fixed, based on the terms of a given bond or loan contract. As a result, the cost of debt is usually both certain and predictable. The cost of equity

is usually fixed, based on the terms of a given bond or loan contract. As a result, the cost of debt is usually both certain and predictable. The cost of equity  is a little bit more complex, as it is speculative and often determined (to some degree) by investor behavior. The capital asset pricing model (CAPM) is a traditional approach to determining the cost of equity.

is a little bit more complex, as it is speculative and often determined (to some degree) by investor behavior. The capital asset pricing model (CAPM) is a traditional approach to determining the cost of equity.

-

EXAMPLE

A company is evaluating its cost of capital to determine whether it should proceed with a new investment project. The firm is financed through a mix of debt and equity, with 75% of its capital structure made up of debt and 25% from equity. The company pays an interest rate of 6% on its debt, and its corporate tax rate is 30%, which allows it to benefit from the tax deductibility of interest payments. On the equity side, investors require a 10% return to compensate for the risk of holding the company’s stock.

Using this information, what is the company’s weighted average cost of capital (WACC)? What is the minimum return the project must generate to be considered financially viable?

Step 1: Determine the relevant information.

- Cost of Debt Before Tax

0.06, or 6%

0.06, or 6%

- Corporate Tax Rate

0.30, or 30%

0.30, or 30%

- Cost of Equity

0.10, or 10%

0.10, or 10%

- Capital Structure:

- Debt (D): 0.75, or 75%

- Equity (E): 0.25, or 25%

Step 2: Calculate the WACC.

Calculate the after-tax cost of debt (WACC requires the after-tax cost of debt).

Calculate WACC:

Step 3: Interpret the results.

The company’s weighted average cost of capital (WACC) is 5.65%. This means the company must earn at least a 5.65% return on this investment to justify taking it on.

-

A company is considering a new investment project and wants to evaluate its cost of capital to determine whether the project is financially viable. The firm’s capital structure consists of 60% debt and 40% equity. The company pays an interest rate of 5% on its debt, and its corporate tax rate is 25%, allowing it to benefit from the tax deductibility of interest payments. Equity investors expect a 12% return due to the risk associated with holding the company’s stock.

2. The Weightings

To calculate the WACC, we must take into account the weight of each component of a company’s capital structure.

2a. The Variables

Referencing the formula from before:

-

E is the market value of equity.

-

D is the market value of debt.

-

V is the market value of equity plus the market value of debt.

-

is the cost of equity.

-

is the cost of debt.

-

is the company’s tax rate.

is the company’s tax rate.

-

If the market value of a company’s debt and equity is not available, the book value can be used.

The “weighting” varies based on how the company finances its activities. If the value of a company’s debt exceeds the value of its equity, the cost of its debt will have more “weight” in calculating its total cost of capital than the cost of equity. If the value of the company’s equity exceeds its debt, the cost of its equity will have more “weight.”

2b. Market Value Versus Book Value

Because the expected cost of new capital is being measured, the calculation of the WACC usually uses the market values of the various components rather than their book values. These may differ significantly.

Market value and market price are related but distinct financial concepts that describe how assets are valued in different contexts.

-

Market price refers to the current price at which an asset (stock, bond, etc.) is bought or sold in the open market. It is determined by supply and demand and reflects what buyers are willing to pay and sellers are willing to accept at a specific moment. Market price is dynamic and can fluctuate frequently based on investor sentiment, news, and economic conditions.

-

Market value, on the other hand, is a broader concept that represents the estimated worth of an asset, company, or investment in a competitive marketplace. For publicly traded companies, market value is often calculated as market capitalization, which is the market price per share multiplied by the total number of outstanding shares. Unlike market price, which applies to individual units, market value gives a holistic view of a company’s total equity value.

Book value refers to the value of an asset according to the account balance present on the balance sheet of a company. The balance sheet is a summary of the financial balances of a company and is described as a snapshot of a company’s financial condition. An asset’s initial book value is its actual cash value or its acquisition cost. Cash assets are recorded or “booked” at the actual cash value. Assets such as buildings, land, and equipment are valued based on their acquisition cost, which includes the actual cash cost of the asset plus certain costs tied to the purchase of the asset, such as broker fees.

-

- Market Price

- The current price at which an asset (stock, bond, etc.) is bought or sold in the open market, determined by supply and demand, reflecting what buyers are willing to pay and sellers are willing to accept at a specific moment.

- Market Value

- The estimated worth of an asset, company, or investment in a competitive marketplace, often calculated as market capitalization, which is the market price per share multiplied by the total number of outstanding shares.

3. Factors Controlled by the Firm

When pursuing financing, organizations encounter a variety of factors that impact the WACC. Some of these factors are within the firm’s strategic control, while others are external forces outside its control.

3a. Capital Structure

Understanding what capital structure options are available to a firm is critical in financial management.

Capital structure refers to the way in which an organization finances operations. This is generally illustrated via a balance sheet, where the overall assets are offset by the capital structure of liabilities and equity. It is through the decisions to acquire various forms of debt and equity that an organization can derive a WACC that is sustainable within the context of organizational profitability. If the cost of capital is higher than the returns from those investments, the organization lacks the profitability required to justify itself.

In the WACC equation, the first segment measures the cost of equity coupled with the percentage of the capital structure that is funded by equity. The second segment makes the same calculation, but this time with the cost of debt and the relative percentage of capital structure, which is funded via this source. The final segment applies a corporate tax rate.

-

By understanding the cost of each input of the capital structure, firms can control (to some degree) how they fund their operations and acquisitions of assets.

3b. Internal Rate of Return

Another important decision made by financial professionals in relation to the cost of capital revolves around the required rates of return of various projects. Investing capital into an operation always incurs the opportunity cost of investing in something else. As a result, organizations can control their operations by measuring and projecting the rate of return on each project and investing strategically in the most profitable projects.

An internal rate of return (IRR) calculation can be useful when doing this. The IRR looks at the net present value (NPV) of a given project and calculates it for a breakeven point (i.e., set the equation to zero when taking cost into account). By doing so, the organization can identify the anticipated rate of return on the project.

When solving for zero, the organization will identify what the rate of return is for each project. Deciding on projects that provide returns greater than the WACC derived from the capital structure will set the organization down a profitable path (assuming the forecasts are reliable).

-

If the investment return is higher than the WACC, the company should invest. If the WACC is higher than the investment return, the company should NOT invest.

-

- Internal Rate of Return (IRR)

- The rate of return on an investment that causes the net present value of all future cash flows to be zero.

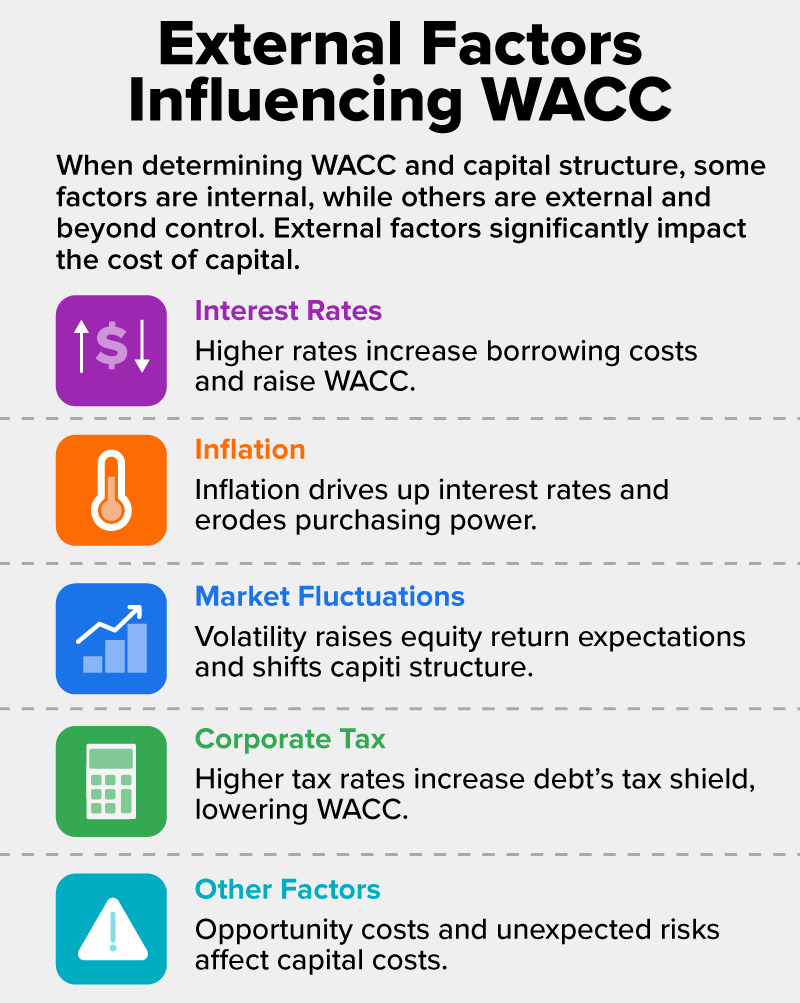

4. Factors External to the Firm

When organizations begin weighing the WACC and determining the overall capital structure, there are some factors that are within the control of the organization and some external factors that are not. When it comes to projecting the cost of capital, it is useful to assess some of the external factors that may influence the overall cost.

-

Interest rates: Interest rates fluctuate for a wide variety of reasons and are a primary tool of monetary policy. When interest rates rise, borrowing becomes more expensive, meaning companies must pay higher interest on new debt, which increases the after-tax cost of debt in the WACC formula. Since debt is typically a cheaper source of capital due to its tax deductibility, a rise in interest rates can significantly raise a company’s overall WACC, making financing new projects more costly and potentially less attractive. Higher interest rates can often lead to lower stock valuations and increased investor expectations for returns, which raises the required rate of return on equity.

-

Inflation: Inflation plays a critical role in shaping a company’s cost of capital, particularly through its influence on interest rates. As inflation rises, lenders demand higher interest rates, directly increasing the cost of debt for borrowers, which raises the overall cost of financing. Organizations must account for the time value of money, recognizing that the purchasing power of borrowed capital may erode over time. In WACC calculations, inflation-adjusted rates help ensure that future cash flows are evaluated in real terms, providing a more accurate picture of a project's viability.

-

Market fluctuations: Market fluctuations play a significant role in shaping a company’s weighted average cost of capital (WACC) because they directly affect the cost of both equity and debt. When markets are volatile, investor risk perception increases, which can lead to higher required returns on equity. In addition, market fluctuations can alter the capital structure weights used in the WACC. Since the WACC is based on the market value of equity and debt, a sharp drop in stock price reduces the market value of equity, potentially increasing the proportion of debt in the capital structure. This shift can raise the company’s financial risk and further increase its cost of capital.

-

Corporate tax: The corporate tax rate affects the weighted average cost of capital (WACC) primarily through its impact on the cost of debt. Interest payments on debt are tax-deductible, which means that companies effectively pay less for borrowed funds than the stated interest rate. This tax shield reduces the after-tax cost of debt, making debt a more attractive financing option compared to equity. The higher the tax rate, the greater the reduction in the cost of debt, lowering the overall WACC. If tax rates decrease, the benefit of the interest tax shield diminishes, potentially making equity financing more competitive relative to debt.

-

Other factors: The cost of capital is largely a simple trade-off between the time value of money, risk, return, and opportunity cost. Any external factors in the form of opportunity costs or unexpected risks can impact the overall cost of capital.

5. Making Risk Adjustments

The WACC is the minimum return that a company must earn on an existing asset base. This means that, when calculated, the WACC will produce a rate equivalent to the current level of risk present in a company’s activities. However, some new ventures will require taking on risks outside of the company’s current scope.

In this case, adjustments will need to be made to the WACC to account for the differing levels of risk. If the risk is very different, the company’s current WACC may be sidestepped altogether in favor of a WACC typical for companies with similar investments. It is possible to make such adjustments by figuring the differing risk into the company’s beta.

The beta coefficient, expressed as a covariance, is the risk of a new project in relation to the risk of the market as a whole. A company itself will be considered, for investment purposes, as a “portfolio of assets,” and its beta coefficient will represent the weighted average of each “asset’s” beta. Therefore, if a new project of differing risk is undertaken, the beta for that project will be weighted into the company’s overall cost of capital.

-

If the project is twice as sensitive to fluctuations in the market as the company as a whole, then the project’s beta should be twice that of the company during the valuation process. This will increase the risk premium on the project, its cost of equity, and, subsequently, the WACC. This increase in cost of capital will devalue the company’s stock unless this increase is offset by a higher expected return generated by the project.

6. WACC Considerations

The WACC is a common and highly useful approach to determining how much it will cost (as a percentage) to borrow money to fund a given operation or project. This overall cost of borrowing capital is a great tool for financial professionals who would like to understand how much a project will cost and how much it will provide in return. The overall goal is to maintain a certain level of profitability when it comes to making investments in organizational projects.

6a. Advantages

As a model, the WACC has quite a few advantages:

- The WACC considers the differences between the cost of debt and the cost of equity, allowing the firm to understand how much a project funded fully by debt would differ in terms of capital costs from a project that requires a great deal of equity. In general, debt is almost always cheaper.

- It takes into account the time value of money, normalizing cash flows for the present value.

- Upper management can quickly look at the WACC for a given project and compare that to the forecast of the profitability.

6b. Drawbacks

No forecast is perfect, and the WACC is no exception. The main problems in calculating WACC are the assumptions it relies on. These can include the following:

-

Profitability: The cost of capital is not particularly useful without an understanding of the return on that capital. Profitability in a future market is never certain, as the demands, needs, competition, and price of inputs could change.

-

Opportunity costs: Opportunity costs can significantly threaten the accuracy and usefulness of WACC calculations if they are not properly considered. The WACC is designed to reflect the minimum return a company must earn on its investments to satisfy its capital providers. However, if a company overlooks the opportunity cost of using internal funds instead of distributing them to shareholders or investing them elsewhere, it may underestimate its true cost of capital.

-

Amount required: Projects often encounter unforeseen hurdles, and jumping over these hurdles may require capital that hasn’t been considered in the forecast. As the amount of capital required increases, the financial risk from investors also increases. Higher risk means higher returns, and more capital requirements during the project may increase the overall average cost of capital.

-

While the WACC calculation does rely on quite a few assumptions, this is something of a necessary risk when it comes to financial projections. Forecasts are not sure things; they are intrinsically uncertain. It is exactly due to this uncertainty that capital investments are risky and require returns in the first place. When using this model to predict how much capital can be borrowed and at what rate, keep in mind that the situation can change any day.

In this lesson, you investigated the weighted average cost of capital (WACC), which represents the average rate a company must pay to finance its assets through debt and equity. You reviewed how weightings and variables, such as market value versus book value, affect WACC calculations, and how firms manage factors within their control, like capital structure and internal rate of return (IRR), to maintain profitability.

You also assessed external factors to the firm, including interest rates, inflation, taxation, and market volatility, which influence the cost of financing. The lesson discussed how companies make risk adjustments to the WACC for projects of varying risk levels. Finally, you reviewed WACC considerations, such as the advantages and drawbacks of using the WACC as a decision-making tool.

Overall, the WACC provides a key measure for determining minimum acceptable returns and aligning financing strategies with organizational goals.