Table of Contents |

The statement of cash flows is a vital financial report that explains how changes in the balance sheet and income statement affect a company’s cash position over a specific accounting period. It provides a detailed account of the cash inflows and outflows, offering insight into how a business generates and uses cash.

Among the three primary financial statements, the statement of cash flows is often considered the most critical for assessing a company’s liquidity and financial health. While a company may appear profitable on paper (income statement and balance sheet), it must also maintain sufficient cash to meet its obligations. Without adequate cash, a business may struggle to pay suppliers, service debt, or compensate employees, regardless of its reported profits.

A positive cash flow indicates that more cash is entering the business than leaving it, which is generally a healthy sign. Conversely, a negative cash flow suggests that the company is spending more cash than it is receiving. However, even a strong cash flow does not guarantee long-term success. It must be evaluated in the context of the company’s overall strategy and financial goals.

Like the income statement, the statement of cash flows is typically prepared on a quarterly and annual basis. It highlights both the sources of cash (cash receipts) and the uses of cash (cash payments), helping stakeholders understand how the business manages its cash resources.

The statement is organized into three main categories of business activities:

There are two primary methods used to prepare the operating section of the statement of cash flows: the direct method and the indirect method. While both approaches arrive at the same bottom line, they differ in how they present the sources and uses of cash. Understanding these methods enhances financial literacy and allows you to analyze a company’s ability to sustain operations, meet obligations, and invest in future growth.

The direct method lists actual cash receipts and cash payments from operating activities. This method provides a clear and straightforward view of cash inflows and outflows, making it easier for users to understand how cash is being generated and spent in day-to-day operations.

The indirect method starts with net income from the income statement and adjusts it for non-cash items and changes in working capital (current assets and liabilities). This method is more commonly used in practice because it links the income statement to the cash flow statement.

| Feature | Direct Method | Indirect Method |

|---|---|---|

| Starting Point | Cash transactions | Net income |

| Detail Level | Shows specific cash inflows/outflows | Shows adjustments to net income |

| Common Usage | Less common | Most commonly used |

| Clarity for Users | More intuitive | Less intuitive, but links to net income |

| Required by GAAP? | Allowed, but reconciliation to indirect is required | Allowed and widely used |

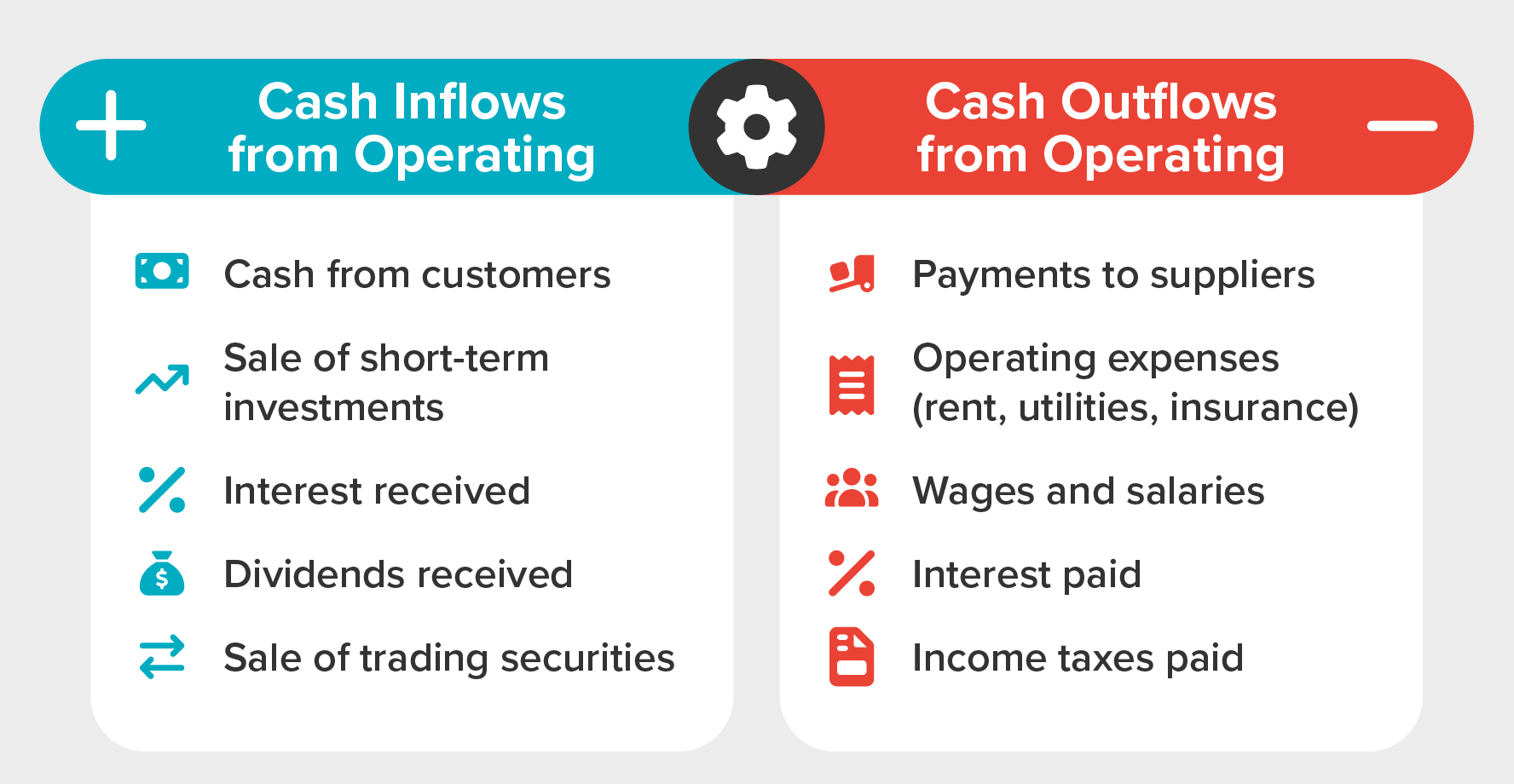

Cash flows from operating activities represent the cash generated or used by a company’s core business operations during a specific period. These activities reflect the day-to-day functions that drive revenue and incur expenses (the cash impact of delivering goods or services).

Unlike net income, which includes noncash items like depreciation or accruals, operating cash flow focuses solely on actual cash transactions. It shows how much cash the business brings in from its operations and how much it spends to keep those operations running.

Common cash inflows from operating activities (+) include:

These cash flows are crucial for assessing a company’s ability to sustain operations, pay debts, and reinvest in growth without relying on external financing.

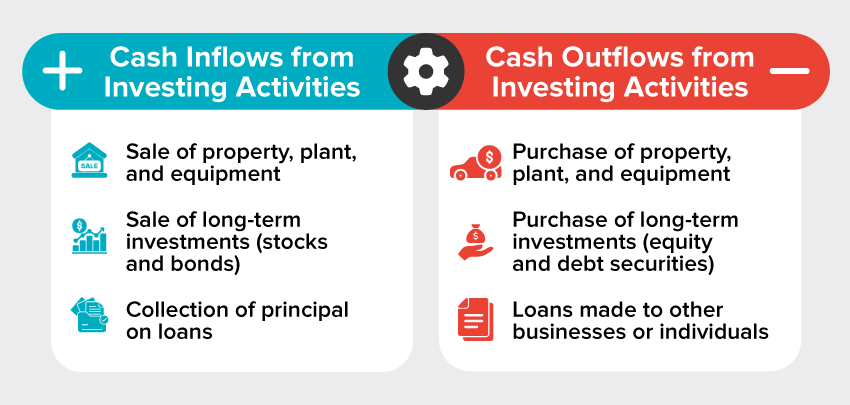

Investing activities reflect how a company allocates cash to acquire and dispose of long-term assets and investments. These activities are associated with changes in noncurrent assets, such as property, plant, and equipment, as well as financial investments like stocks, bonds, and loans made to others. While these transactions may not occur as frequently as operating activities, they are crucial for understanding a company’s growth strategy and long-term financial planning.

Investing activities also include returns on investments, such as dividends received from other entities and gains from the sale of long-term assets. These cash flows are reported in the investing section of the statement of cash flows—not the income statement—even though they may influence net income.

Common cash inflows from investing activities (+) include:

These cash flows help stakeholders assess whether a company is investing in its future or liquidating assets to generate cash. A healthy balance of investing inflows and outflows often signals a company that is both growing and managing its resources wisely.

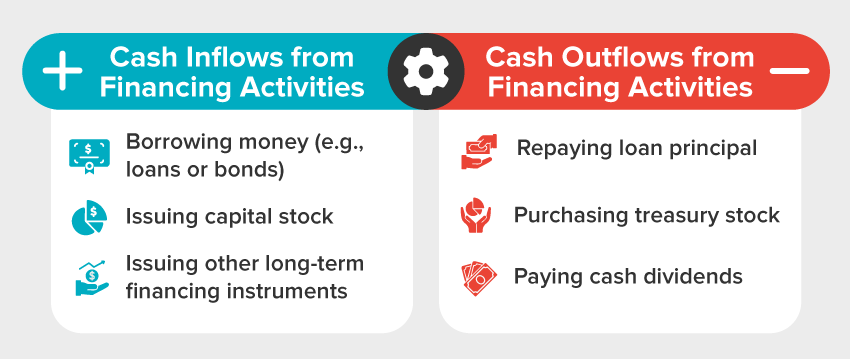

Financing activities represent the ways a company raises capital and returns value to its investors. These activities involve transactions related to noncurrent liabilities and equity, and they are essential for understanding how a business funds its operations and growth over time.

In the context of the statement of cash flows, financing activities include borrowing money, repaying debt, issuing or repurchasing stock, and paying dividends. These transactions reflect strategic financial decisions that affect the company’s capital structure and long-term financial stability.

Changes in financing activities are typically reflected in both the cash flow statement and the statement of changes in equity.

Common cash inflows from financing activities (+) include:

These cash flows help stakeholders evaluate how a company finances its operations, whether through debt, equity, or a combination of both and how it returns value to investors.

If a business runs out of cash, it must either borrow or cease operating, thus making the analysis of its cash flows highly important. Analyzing a cash flow statement involves understanding how changes in accounts affect a company’s cash position. A few general rules guide this analysis:

As you have learned, the statement is divided into three sections: operating, investing, and financing activities. Each of these sections offers insights into different aspects of the business.

An analyst looking at the cash flow statement will first care about whether the company has a net positive cash flow. Having a positive cash flow is important because it means that the company has at least some liquidity and may be solvent.

Regardless of whether the net cash flow is positive or negative, an analyst will want to know where the cash is coming from or going. The company may have a positive cash flow from operations but a negative cash flow from investing and financing. This gives important insight into how the company is making or losing money.

The analyst will continue breaking down the cash flow statement by examining the specific factors that affect the cash flow. For instance, cash flows from operating activities provide feedback on a company’s ability to generate income from internal sources. Thus, these cash flows are essential for helping analysts assess the company’s ability to meet ongoing funding requirements, contribute to long-term projects, and pay dividends.

As you will learn in upcoming lessons, an analysis of cash flows from investing activities focuses on ratios when assessing a company’s ability to meet future expansion requirements.

Analysts often calculate free cash flow (cash from operations minus capital expenditures) to assess how much cash is available for dividends, debt repayment, or reinvestment. This metric is especially important because a company can be profitable yet still have negative free cash flow, which may signal liquidity issues.

Ultimately, cash flow analysis helps determine whether a company can sustain operations, invest in growth, and return value to shareholders, all without jeopardizing its financial stability.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM "BOUNDLESS FINANCE" PROVIDED BY LUMEN LEARNING BOUNDLESS COURSES. ACCESS FOR FREE AT LUMEN LEARNING BOUNDLESS COURSES. LICENSED UNDER CREATIVE COMMONS ATTRIBUTION-SHAREALIKE 4.0 INTERNATIONAL.