In this lesson, you will learn what a collection agency is, how they work, and how to handle a collection agency. Specifically, this lesson will cover the following:

1. What a Collection Agency Is

Imagine your favorite coffee shop. They know you by name, they know your go-to order, and they trust you. One day, you forget your wallet, but the barista says, “Don’t worry, pay us next time!” Weeks go by, and you keep forgetting to pay them back. Eventually, the shop decides it’s no longer worth chasing you down. Instead, they call in a “friend” to help collect the money.

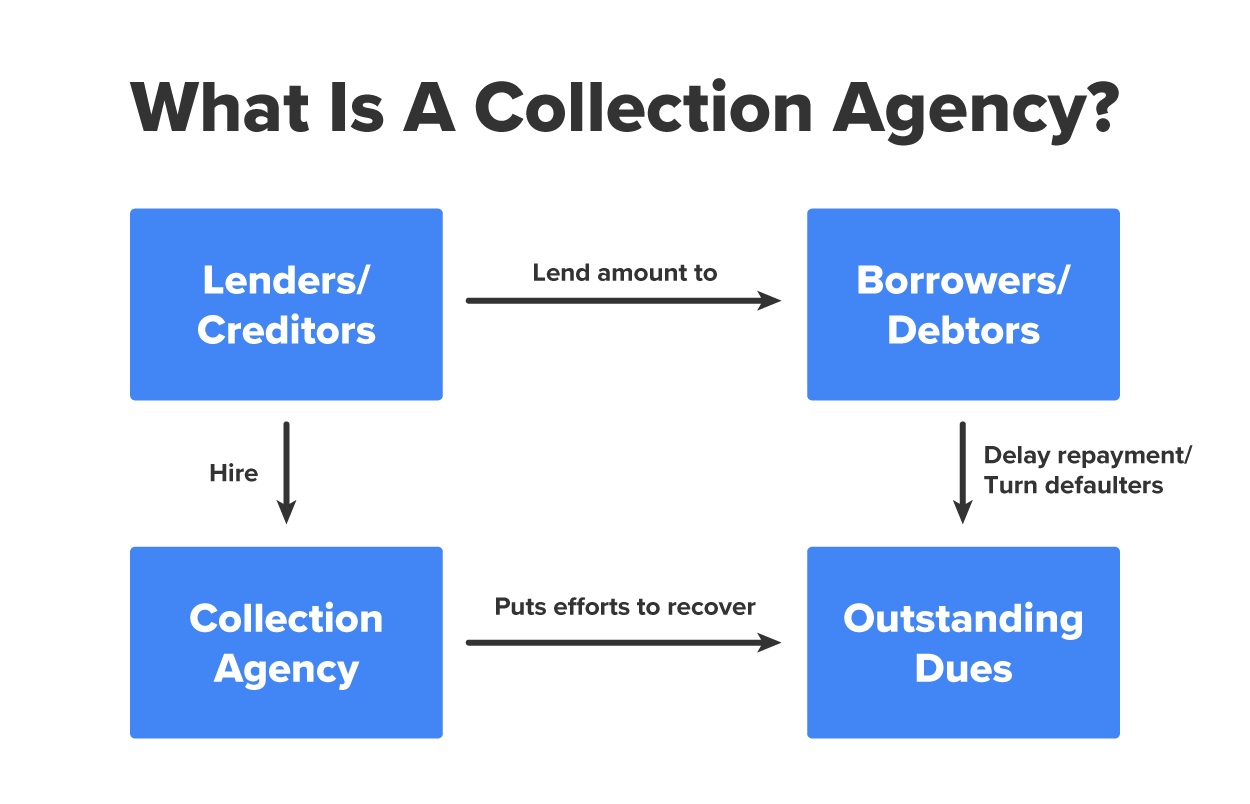

That friend is essentially a collection agency. Collection agencies are businesses that step in to recover unpaid debts for companies that don’t have the time, resources, or patience to track down payments themselves.

Let’s break down collection agencies into simple terms, using examples and relatable stories to help you grasp what they do, why they exist, and how to handle them confidently.

Businesses thrive when their customers pay their bills on time. But what happens when customers don’t? Companies lose money, and chasing those unpaid bills can eat up valuable time. Imagine running a small business where half your customers haven’t paid for their services. How would you keep the lights on?

Here’s where collection agencies come in. By hiring these agencies, businesses can hand off the burden of debt collection and focus on what they do best. Think of it like hiring movers when you need to relocate—it saves time, energy, and stress.

1a. How Collection Agencies Work

Imagine you loaned your friend $500 to help with an emergency, and they promised to pay you back in 2 months. This turns into 6 months, your texts go unanswered, and now you’re frustrated because you don’t have the time or energy to keep chasing them. What if you could call in a professional to handle it for you? That’s essentially how collection agencies operate.

When businesses can’t collect on unpaid debts, they turn to collection agencies. These agencies specialize in tracking down debtors, recovering money, and sometimes even negotiating payments. It’s not magic—it’s a systematic process that combines persistence, negotiation skills, and a bit of detective work.

-

Let’s break down how it all works step by step.

Step 1. Assigning or Purchasing Debt

Let’s say you forgot to pay a $100 utility bill. After several reminders, the utility company decides to hire a collection agency to recover the money. This is called assigning the debt. Alternatively, the agency might buy your debt outright, often for pennies on the dollar. If the debt is purchased, the agency now owns the right to collect it.

Step 2. Locating the Debtor

Let’s say you moved to a new city and forgot to update your address with your credit card company. You owe $500, but the company can’t reach you. Collection agencies use a technique called

skip tracing to track you down through databases, public records, and even social media.

Step 3. Contacting the Debtor

You start getting phone calls, emails, or letters from the agency explaining that you owe money. They might say, “This is an attempt to collect a debt. Please call us to discuss repayment options.”

Step 4. Negotiating Payment

Agencies know that collecting something is better than collecting nothing, so they often offer settlements or payment plans. Let’s say you owe $1,000; the agency might say, “If you can pay $700 now, we’ll consider the debt settled.”

Step 5. Taking Legal Action

As a last resort, collection agencies might sue you for unpaid debt, especially if it’s a large amount. This step requires going through the court system, so it’s not taken lightly.

IN CONTEXT

Debt can catch anyone off guard, often from small, forgotten bills or unexpected charges. Whether it’s an overlooked gym membership, a surprise medical bill, or a neglected store credit card, these situations show how quickly unpaid debts can land in the hands of a collection agency. Let’s explore a few relatable examples.

-

EXAMPLE

Example 1: The Gym Membership That Won’t Quit

- You joined a gym last year, but after a few months, you stopped going and forgot to cancel. The membership fee kept piling up. One day, you get a letter from a collection agency saying you owe $300. You had no idea your old gym was still charging you!

Example 2: The Medical Bill Surprise

- You went to the emergency room for a minor injury, assuming your insurance covered everything. Months later, a collection agency contacts you about a $1,200 bill you didn’t know existed.

Example 3: The Credit Card You Forgot About

- Years ago, you opened a store credit card for a discount. You stopped using it but forgot to pay off a small balance. Over time, interest and fees ballooned the amount, and now a collection agency is calling about your “forgotten” $800 debt.

Understanding how collection agencies work can take some of the fear and mystery out of the process. At the end of the day, they’re just doing their job—recovering money for creditors—and while their methods may feel persistent or even frustrating, knowing their approach gives you the upper hand.

Whether it’s skip tracing, negotiating payments, or sending letters, their goal is to close out the debt. But here’s the key: The more you know, the better equipped you’ll be to handle them. If a debt ever goes to collections, you don’t have to panic. Instead, you can face the situation with clarity, confidence, and a plan. Let’s dive into what to do if that happens.

-

- Collection Agencies

- Companies hired by creditors to recover unpaid debts from individuals or businesses.

- Skip Tracing

- The process of locating individuals who have moved or changed contact information.

2. How to Handle a Collection Agency

Now that you understand what a collection agency is and how it works, let’s talk about what to do if you have a debt that goes to collections. Getting contacted by a collection agency can feel overwhelming. Maybe you see an unfamiliar number on your phone or a letter with bold words like “DEBT COLLECTION NOTICE” in your mailbox. The initial reaction is often panic, followed by a flood of questions: “Is this real? How did this happen? What do I do now?”

Here’s the good news—you have options and rights, and with the right approach, you can manage this situation calmly and confidently. Let’s break it down step by step with relatable examples and practical tips, so you can handle a collection agency like a pro.

-

- Step 1. Stay Calm and Don’t Panic

- It’s easy to feel defensive or scared when a collection agency contacts you. You might immediately think, “What if they ruin my credit? What if I can’t pay?” But panicking won’t help—and the situation is often less dire than it feels.

- Imagine getting pulled over for speeding. Your heart races, but the best approach is to stay calm, provide your license, and handle the situation rationally. Dealing with a collection agency is similar: Stay composed and focus on the steps ahead.

- Step 2. Verify the Debt

- Before you pay anything, confirm that the debt is real and that the collection agency has the right to collect it. Mistakes happen, and sometimes debts are already paid or don’t belong to you.

-

- Request a debt validation letter, which the agency is legally required to provide. This letter should include details like the original creditor, the amount owed, and proof that the agency has the right to collect the debt.

-

EXAMPLE

You receive a call saying you owe $1,000 on a credit card you haven’t used in years. Before paying, you ask for a validation letter. Upon reviewing it, you realize that the debt was already settled years ago but wasn’t properly recorded.

- Think of this like double-checking a receipt after grocery shopping. If something looks off, don’t assume it’s correct—ask questions and get clarity.

- Step 3. Know Your Rights

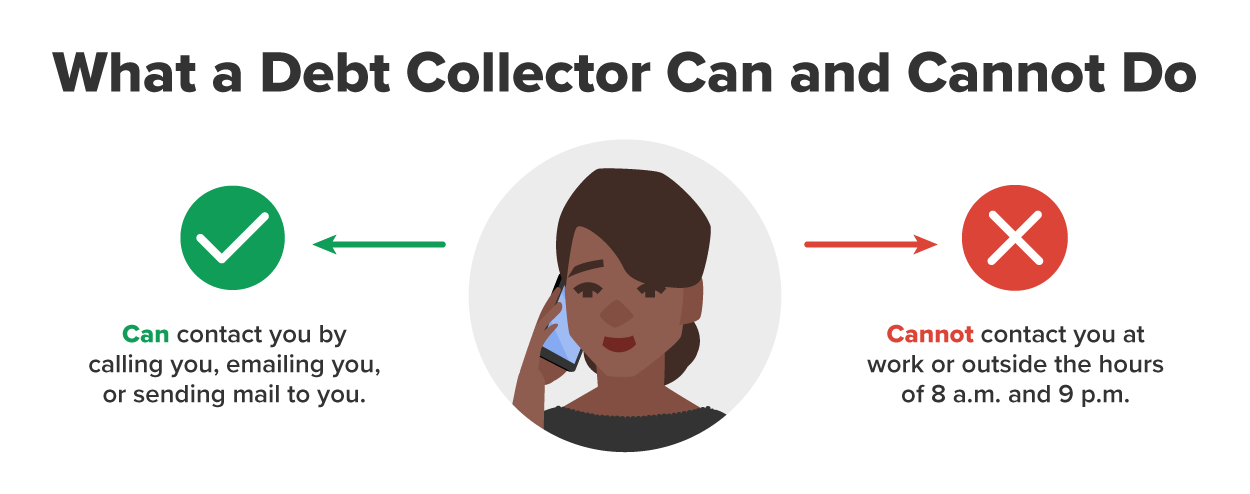

- Collection agencies must follow strict rules under laws like the Fair Debt Collection Practices Act (FDCPA) in the United States. Knowing these rights can help you feel more empowered during interactions.

- Key Rights to Remember:

- They can’t harass you, threaten you, or use abusive language.

- They can’t call you before 8 a.m. or after 9 p.m.

- If you ask them to stop contacting you at work, they must comply.

- Imagine you’re dealing with an aggressive salesperson at a car dealership. If they cross a line, you’d walk away or ask for a manager. Similarly, if a collection agency oversteps, you can file a complaint with the Consumer Financial Protection Bureau (CFPB).

- Step 4. Communicate Without Emotion

- When interacting with a collection agency, stay professional and keep your emotions in check. It’s easy to get frustrated, but remember, you’re in control of how you respond.

-

Communicate in writing whenever possible. This creates a paper trail that can protect you if there’s a dispute.

-

EXAMPLE

You receive a phone call about a $500 debt. Instead of discussing it over the phone, you ask the agency to send details in writing. This gives you time to review the information without feeling pressured.

- Think of it like negotiating with a landlord. It’s always better to get agreements in writing—verbal promises can easily be forgotten or misinterpreted.

- Step 5. It’s OK to Negotiate

- Collection agencies are often willing to settle debts for less than the full amount. If you can’t pay the entire balance, explain your situation and offer a reasonable amount you can afford.

-

EXAMPLE

You owe $2,000 on a credit card debt. You can’t pay it in full, so you negotiate a monthly payment plan of $150.

- Think of this like haggling at a flea market. The seller might want $50 for an item, but they’d rather take $35 than lose the sale. Collection agencies often have the same mindset—they’d rather collect something than nothing.

-

-

To see an example script of what to say when you call a collection agency and negotiate with them, select the drop-down “+” button to the right.

Important: Keep in mind that this is only a scenario and every interaction with a collection agency can be different; however, it helps to identify the importance of keeping calm and what to ask for. Always remember to be friendly and kind.

In this scenario, Jullian is calling the collection agency.

Step 1: Confirm the Debt

Start the conversation by verifying the details of the debt.

Jullian: “Hi, I’m calling about a debt I was contacted about. Can you confirm the original creditor, the amount owed, and the date of the debt?”

If they cannot provide details:

Jullian: “I’ll need written validation of this debt before I can discuss it further. Please send me a validation letter. Thank you.”

Step 2: Express Willingness to Resolve

Once the debt is confirmed, show you want to address it but explain your financial limitations.

Jullian: “Thank you for confirming the details. I want to resolve this debt, but I’m not in a position to pay the full amount. Are there settlement options available?”

Step 3: Negotiate

Make a counteroffer if their initial settlement isn’t workable for you.

Jullian: “The amount you’ve offered is still more than I can manage. I’d like to propose [insert offer, e.g., 50% of the debt] as a one-time payment to settle this debt.”

If they counter your offer:

Jullian: “I understand your position, but [insert reason, e.g., ‘I’m facing financial challenges’]. I can pay [insert new amount] to resolve this today. Would that be acceptable?”

Step 4: Request Written Confirmation

Before paying, ensure you have the agreement in writing.

Jullian: “I’d like written confirmation of the settlement terms, including the agreed amount, the payment deadline, and confirmation that the debt will be marked as paid in full and reported to the credit bureaus. Can you send this to me by mail or email?”

Step 5: Finalize the Payment

Once you’ve received written confirmation, make the payment and follow up.

Jullian: “I’ve sent the payment as agreed. Can you confirm that it has been received and that the account is now resolved? Please send me a letter confirming that the debt is closed and will be reported as paid in full.”

- Step 6. Keep Detailed Records

- Every phone call, email, letter, or agreement with a collection agency should be documented. Keeping records ensures you have proof of what was said or agreed upon, which can protect you if disputes arise.

-

- What to Record:

- Dates and times of phone calls

- Names of representatives you spoke with

- Details of payment plans or settlements

-

EXAMPLE

You agree to settle a $700 debt for $500. However, 2 months later, the agency claims you still owe $200. Because you saved the confirmation email, you can prove the agreement and resolve the issue quickly.

- Step 7. Monitor Your Credit Report

- Debts sent to collections can affect your credit score, but paying them off or settling them doesn’t always update your credit report automatically. After resolving a debt, check your credit report to ensure that the information is accurate.

- Take action: After paying off a $1,000 debt, you notice it’s still listed as “unpaid” on your credit report. You contact the agency and request that they update the status with the credit bureaus.

- Think of this like returning an item to a store. You wouldn’t assume that the return was processed correctly without checking your receipt or bank statement, right? The same goes for your credit report.

Handling a collection agency isn’t just about resolving debt—it’s about staying in control of the situation. By staying calm, verifying the debt, knowing your rights, and negotiating smartly, you can protect your finances and your peace of mind.

Remember, everyone makes financial mistakes or faces unexpected challenges. Dealing with a collection agency doesn’t define you—it’s just another step in your financial journey.

-

- Debt Verification Letter

- A document you can request from a collection agency to confirm the details and legitimacy of a debt before making payments.

- Fair Debt Collection Practices Act (FDCPA)

- A U.S. law that protects consumers from harassment, abuse, or deceptive practices by debt collectors.

- Consumer Financial Protection Bureau (CFPB)

- A government agency that ensures fair treatment in financial matters.

In this lesson, you learned what a collection agency is and how collection agencies work. You also got a detailed explanation of how to handle a collection agency if you have a debt that goes to collections.