Table of Contents |

In the last lesson, you learned all about the power of personal finance. Now, let’s look at it from a psychological lens.

Money is more than numbers in a bank account or the paper bills in your wallet. It’s emotional, psychological, and deeply tied to who you are and how you make decisions. It’s about your emotions, upbringing, beliefs, and fears. If you’ve ever wondered why you feel anxious about spending, why saving feels impossible, or why you can’t break free from financial mistakes, you’re not alone. Understanding the psychological aspects of money, your financial behaviors, and the factors that influence your financial decisions can be life changing.

Before we dive into behaviors and external influences, let’s start with what’s closest to home: your mindset and how it’s shaped. How you think and feel about money influences every decision you make, whether you realize it or not.

Your Money Story

Everyone has a money story—the narrative you’ve unconsciously built about what money means to you. These stories are shaped by your upbringing, cultural influences, personal experiences, and even societal expectations. Did you grow up hearing “Money doesn’t grow on trees”? Were you taught to save every penny, or were you encouraged to spend because “you can’t take it with you”? These messages become the foundation of how you think, feel, and act with money today.

Your money story isn’t just about numbers; it’s deeply emotional and personal. It influences the choices you make every day—whether you’re budgeting, saving, spending, or even talking about money with others. It’s not just about what you do with money but why you do it. Understanding your money story is the first step to taking control of your finances and shifting patterns that may be holding you back.

Let’s look at a few examples of money stories:

Scenario 1: Emily’s Story

Emily grew up in a household where her parents fought about money constantly. Discussions about bills and spending would escalate into heated arguments that filled her with anxiety. As an adult, Emily avoids checking her bank account altogether because money feels stressful and overwhelming. She often ignores financial issues until they become urgent, reinforcing her sense of dread.

Scenario 2: Marcus’s Story

Marcus was raised with a “work hard, spend hard” mentality. His parents believed that life is short, so you might as well enjoy it. Vacations, gadgets, and nights out were always prioritized over savings. Now, Marcus lives paycheck to paycheck, thinking, “What’s the point of saving if you can’t enjoy it?” He struggles to break free from this cycle, even though he dreams of owning a home and building wealth.

Scenario 3: Priya’s Story

Priya grew up in a family where saving was a badge of honor. Her parents clipped coupons, hunted for sales, and kept a spreadsheet of every expense. While this taught Priya the value of financial discipline, she now feels paralyzed when making decisions about spending. She agonizes over every purchase, afraid of “wasting money,” which keeps her from fully enjoying her hard-earned income.

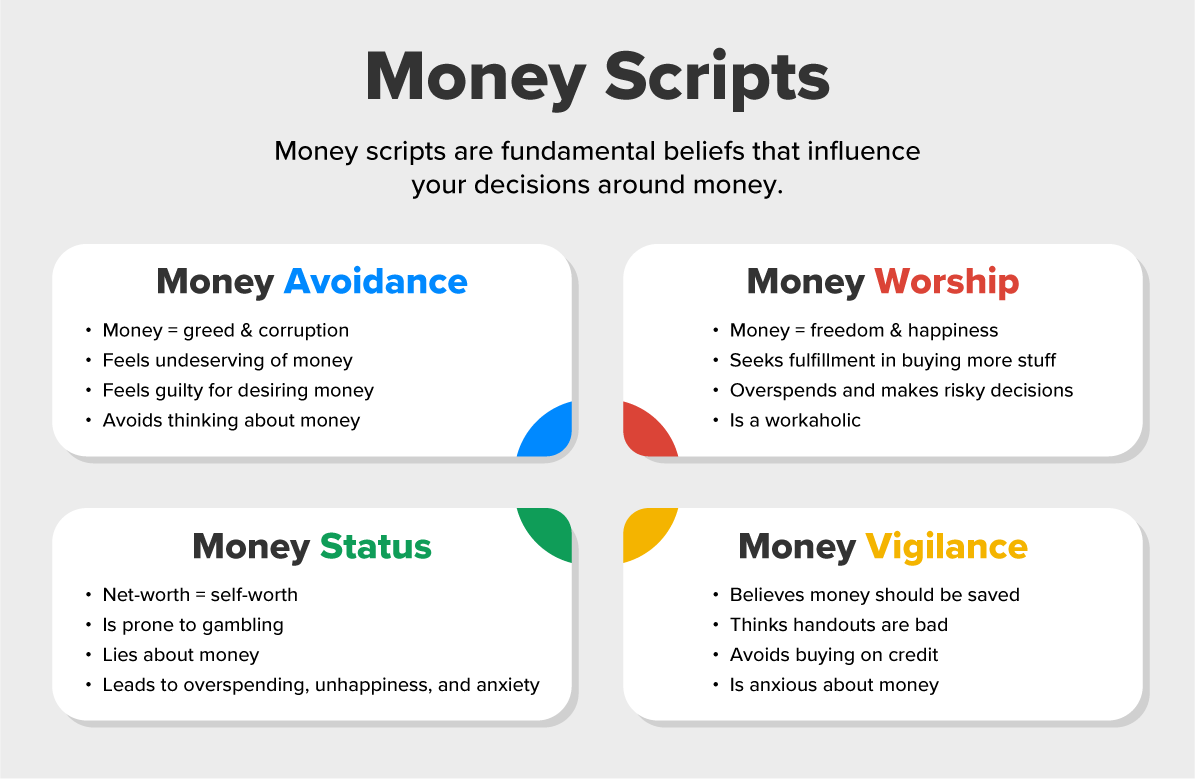

Money Scripts

In addition to your money story, you likely have money scripts—those deeply ingrained beliefs about money that influence your behavior, often without you realizing it. These scripts are the “rules” you’ve internalized about money based on childhood experiences, societal influences, or even trauma. While some money scripts can be empowering, many are limiting and can hold you back from achieving your financial goals or living the life you want.

Money scripts are sneaky. They shape how you make decisions—what you spend on, what you save for, and even how you feel about financial success. The key is recognizing your dominant money scripts and evaluating whether they’re truly serving you or sabotaging your financial health.

The Four Major Money Scripts

There are four major money scripts to be aware of. You might relate to one script or another, and that might change throughout your lifetime.

Once you recognize a limiting money script, challenge it by looking for evidence to the contrary.

For example:

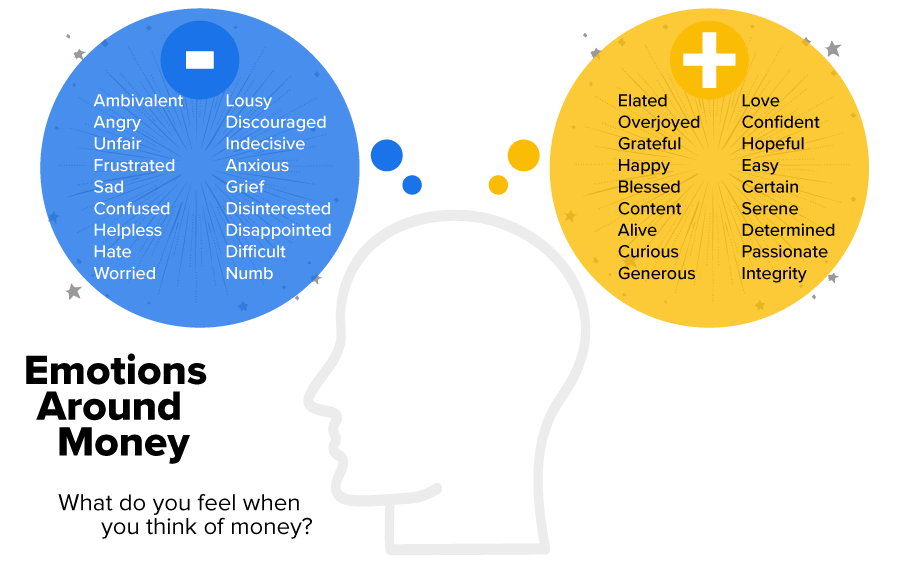

Money can trigger a whirlwind of emotions—shame, guilt, anxiety, fear, excitement, or even joy. These emotions aren’t inherently bad; they’re simply signals that something deeper is happening. However, when we let emotions dictate our financial decisions, we often act in ways that aren’t aligned with our goals or values.

As we’ve already discussed, money isn’t just numbers on a spreadsheet; it’s tied to our sense of security, self-worth, and even identity. This is why money decisions can feel so loaded. Recognizing the emotional triggers behind our financial choices is a key step toward creating a healthier relationship with money.

EXAMPLE

Let’s say it’s Friday evening. You’ve had a tough week at work, your inbox is still overflowing, and your boss has been particularly demanding. You’re scrolling through an online store, convincing yourself, “I deserve this.” You hit “Buy” on something expensive—maybe it’s a new gadget, outfit, or subscription you’ve been eyeing. At that moment, it feels good, even empowering. But the next day, regret kicks in. Why did I spend that much? I didn’t really need it. This is emotional spending in action—using money to soothe emotions rather than addressing the root cause.This is just one example of how emotions can influence our behavior with money.

Here are more ways it might show up:

Emotions aren’t the enemy—they’re a natural part of your financial journey. But left unchecked, they can lead to patterns that keep you stuck. By recognizing and managing the emotional side of money, you can make intentional choices that move you closer to the financial life you want.

Now that we’ve explored the emotional side of money, let’s dive into how those emotions translate into financial behaviors—unpacking why we make the choices we do and how to shift those patterns to align with our goals.

Having uncovered the emotional and psychological foundations of money, it’s time to focus on the actions those beliefs inspire. Your daily financial habits—whether intentional or not—are a direct reflection of these deeper patterns. When left unchecked, these behaviors can keep you stuck in cycles of stress, avoidance, or overspending. Let’s explore four common financial behaviors and how they show up, so you can start identifying and shifting them in your own life.

1. Spending Habits

Spending is often tied to how we feel in the moment. Think of the last time you treated yourself to something unexpected. Was it a reward for a tough day or a way to feel better in the moment?

2. Psychological Triggers

Let’s bring this concept closer to home with a relatable scenario: Sarah gets a bonus at work. She feels she’s been working so hard and deserves a splurge. She spends the entire bonus on a luxury handbag. A week later, she regrets the decision because she realizes it could have gone toward her debt. The handbag purchase wasn’t about need—it was about rewarding herself emotionally.

What Sarah didn’t realize is that her spending was tied to a mindset of lack. She thought, “If I don’t spend it now, I might not get another chance.” Understanding this trigger can help her make more thoughtful choices next time.

3. Saving Habits

Saving money can feel boring, but it’s the foundation of financial security. Why, then, is it so hard? For example, Nadia knows she should save but spends her entire paycheck each month. Why? Because saving feels like she’s depriving herself, and she grew up in a household where there was never enough.

EXAMPLE

You’re setting aside $20 a week for savings. At first, it feels pointless. But over time, you notice the balance growing. It starts to feel like a safety net—something you’re building for yourself. This keeps you motivated to keep saving money and make intentional choices with your spending.For some, saving feels restrictive. You might think, “If I save, I can’t enjoy my life now.” The trick is to reframe saving as a form of self-care. By saving, you’re saying, “I care about my future self enough to provide security and freedom.”

4. Debt Cycles

Debt often feels like a trap, but it’s rarely just about numbers. It’s about behaviors, too. Why do so many people fall back into debt after paying it off? For example, Carlos pays off his credit card but immediately charges it back up. Why? Because he hasn’t addressed the underlying behavior: using credit to feel “wealthy” when he’s actually overspending.

Debt can also feel overwhelming, which leads to avoidance. Many people don’t open their bills or look at their balances because it triggers anxiety. This avoidance makes the problem worse, creating a vicious cycle.

Breaking the Cycle

Imagine breaking free from these patterns. What would it feel like to:

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.