In this lesson, you will learn how the payback method evaluates investments based on how long it takes to recover the initial cost. You’ll explore the advantages and limitations of this approach, how to calculate the payback period, and how to adjust the method to account for the time value of money using the discounted payback period. Specifically, this lesson will cover:

1. Defining the Payback Method

In the context of capital budgeting, the payback period refers to the amount of time it takes to recover the cost of an initial investment—in other words, the length of time it takes for an investment to reach its breakeven point.

-

- Payback Period

- The amount of time it takes to recover the cost of an initial investment.

1a. Advantages

The payback period is often determined using a tool of analysis called the payback method, because it is easily applicable and understandable for most people, regardless of their level of academic training or particular field of endeavor. The payback method can be beneficial in comparing similar investments, when applied carefully. The only explicit criterion required when utilizing the payback method as a self-contained tool to compare an investment is that the payback period should be less than infinity; other than this qualifier, the payback method has no specific criteria for decision making.

1b. Disadvantages

As a method of analysis, there are, however, some significant limitations and qualifications attached to using the payback method; namely, it fails to account for considerations such as the time value of money, risk, financing, and opportunity cost. Now, the issue with the time value of money can be remedied by applying a weighted average cost of capital discount. Prevailing opinion dictates that this particular tool for investment decisions should not be used in a vacuum or in isolation. Alternatively, economists prefer measures of return like net present value and internal rate of return.

When utilizing the payback method, it is implicitly assumed that returns to the investment persist after the payback period. Lastly, it should be noted that the payback method does not make the required comparisons to either other investments or to the scenario of not having made an investment at all.

2. The Payback Period

The payback period is usually expressed in years. Start by calculating the net cash flow for each year, which is the cash inflow subtracted from the cash outflow for that year. Then, calculate the cumulative cash flow:

-

- Cumulative Cash Flow

Accumulate by year until the cumulative cash flow is positive; this year will be the payback year.

-

EXAMPLE

Eagle Landscaping is considering investing $150,000 in an excavator that will yield the anticipated net cash flows:

- Year 1: $60,000

- Year 2: $30,000

- Year 3: $45,000

- Year 4: $35,000

- Year 5: $50,000

What is the payback period in years for the investment?

Step 1: Determine the relevant information.

- Cash outflow: $150,000

- Year 1 cash inflow: $60,000

- Year 2 cash inflow: $30,000

- Year 3 cash inflow: $45,000

- Year 4 cash inflow: $35,000

- Year 5 cash inflow: $50,000

Step 2: Calculate the payback period in years.

|

Year

|

Investment

|

Cash Flow

|

Cumulative Cash Flow

|

|

Year 0

|

−$150,000

|

0

|

−$150,000

|

|

Year 1

|

0

|

$60,000

|

−$90,000

|

|

Year 2

|

0

|

$30,000

|

−$60,000

|

|

Year 3

|

0

|

$45,000

|

−$15,000

|

|

Year 4

|

0

|

$35,000

|

$20,000

|

|

Year 5

|

0

|

$50,000

|

$70,000

|

Step 3: Interpret the results.

Eagle will be “paid back” for its investment during Year 4 since the investment is recovered during this period. Eagle must be careful in using this payback period, as it does not reflect the time value of money.

-

Tumblin’ In, a manufacturer of clothing dryers, is considering investing $120,000 in a new automated machine that will produce dryers more rapidly. The investment is expected to generate the following net cash flows:

- Year 1: $35,000

- Year 2: $25,000

- Year 3: $30,000

- Year 4: $20,000

- Year 5: $20,000

What is the payback period, in years, for this investment?

Step 1: Determine the relevant information.

- Initial Investment: $120,000

- Year 1 Cash Inflow: $35,000

- Year 2 Cash Inflow: $25,000

- Year 3 Cash Inflow: $30,000

- Year 4 Cash Inflow: $20,000

- Year 5 Cash Inflow: $20,000

Step 2: Calculate the payback period.

|

Year

|

Investment

|

Cash Flow

|

Cumulative Cash Flow

|

|

0

|

-$120,000

|

$0

|

-$120,000

|

|

1

|

$0

|

$35,000

|

-$85,000

|

|

2

|

$0

|

$25,000

|

-$60,000

|

|

3

|

$0

|

$30,000

|

-$30,000

|

|

4

|

$0

|

$20,000

|

-$10,000

|

|

5

|

$0

|

$20,000

|

$10,000

|

Step 3: Interpret the results.

Tumblin’ In will be paid back during Year 5 since the cumulative cash flow turns positive in that year. This means the investment is recovered sometime in Year 5. While the payback period is a useful tool for understanding how quickly an investment is recouped, it does not account for the time value of money or cash flows beyond the payback point, so it should be used alongside other evaluation methods like NPV or IRR.

-

To calculate a more exact payback period, use the following formula: Divide the amount to be initially invested by the estimated annual net cash inflow.

The payback period method does not take into account the time value of money. Some businesses modify this method by adding the time value of money to get the discounted payback period. They discount the cash inflows of the project by a chosen discount rate (cost of capital) and then follow the usual steps of calculating the payback period.

The calculation becomes more complex when the cash flow fluctuates between positive and negative values multiple times—that is, it contains outflows in the middle or at the end of the project’s lifetime. In this situation, the modified payback period algorithm can be applied:

-

- Calculate the sum of all the cash outflows.

- Determine the cumulative positive cash flows for each period.

- Calculate the modified payback period as the point at which the cumulative positive cash flow surpasses the total cash outflow.

3. The Discounted Payback Period

The payback method is quite a simple concept. The majority of business projects (or even entire business plans for an organization) will require capital. When investing capital in a project, it will take a certain amount of time before the profits from the endeavor offset the capital requirements. Of course, if the project never makes enough profit to cover the start-up costs, it is not an investment to pursue. In the simplest sense, the project with the shortest payback period is most likely the best of the possible investments, or has the lowest risk, at any rate.

Time is a commodity with a cost from a financial point of view. Having the money sooner means more potential investment and, thus, less opportunity cost. The shorter-time-scale project would also appear to have a higher profit rate in this situation, making it better for that reason as well.

-

EXAMPLE

A project that costs $100,000 and pays back within 6 years is not as valuable as a project that costs $100,000 and pays back in 5 years.

If the payback method does not take into account the time value of money, the real net present value (NPV) of a given project is also not being calculated. This is a significant strategic omission, particularly relevant in longer-term initiatives. As a result, all corporate financial assessments should discount payback to weigh the opportunity costs of capital being locked up in the project.

One way to do this is to find the discounted payback period by discounting projected cash flows into present dollars based upon the cost of capital using the following formula:

-

- Discounted Cash Flow Analysis

-

EXAMPLE

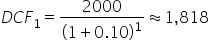

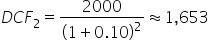

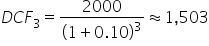

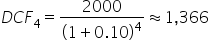

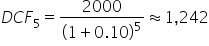

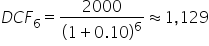

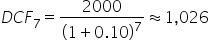

To The Point, a pencil manufacturer, is considering investing in a pencil sharpening machine that costs $10,000. If it returns $2,000 each year in profit (after all expenses and taxes), then this means it will take a total of 5 years without a time value of money discount being applied. If To The Point’s cost of capital is 10%, what is the payback period, taking into account the time value of money?

Step 1: Determine the relevant information.

- Cash outflow (Day 0): $10,000

- Cash inflows (CF years 1–8): $2,000 per year

- Cost of Capital/Discount rate (r): 10%

Step 2: Calculate the payback period, using discounted cash flows.

Use the present value of future cash flows formula to determine discounted cash flows per year.

Use the discounted cash flows to determine the payback period.

|

Year

|

Investment

|

Discounted Cash Flow

|

Cumulative Cash Flow

|

|

0

|

-$10,000

|

$0

|

-$10,000

|

|

1

|

$0

|

$1,818

|

-$8,182 (-$10,000 + $1,818)

|

|

2

|

$0

|

$1,653

|

-$6,529 (-$8,182 + $1,653)

|

|

3

|

$0

|

$1,503

|

-$5,026 (-$6,529 + $1,503)

|

|

4

|

$0

|

$1,366

|

-$3,660 (-$5,026 + $1,366)

|

|

5

|

$0

|

$1,242

|

-$2,418 (-$3,660 + $1,242)

|

|

6

|

$0

|

$1,129

|

-$1,289 (-$2,418 + $1,129)

|

|

7

|

$0

|

$1,026

|

-$263 (-$1,289 + $1,026)

|

|

8

|

$0

|

$933

|

$670 (-$263 + $933)

|

Step 3: Interpret the results.

At the expected $2,000 each year, it will take To The Point over 7 years for full payback. If they did not discount the cash inflows, they would have incorrectly determined the payback period to be 5 years.

-

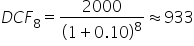

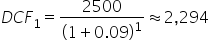

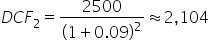

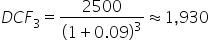

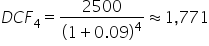

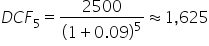

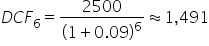

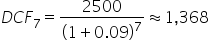

Pen-Sylvania is a manufacturer of sustainable pens that are made from wood. They are considering investing in new software that will help make their supply chain much faster and more efficient. This new software will have an initial cost of $12,000. The after-tax profit of the new software will realize $2,500 per year for the next 8 years. Pen-Sylvania's cost of capital (discount rate) required to invest in this software is 9%.

What is the discounted payback period (in years) if Pen-Sylvania invests in this software?

Step 1: Identify the relevant information.

- Cash Outflow (Day 0): $12,000

- Annual Cash Inflows, After-Tax (Years 1–8): $2,500 per year

- Cost of Capital/Discount Rate (r): 9%

Step 2: Calculate the payback period in years.

Discounted Cash Flows:

Payback Period (years):

|

Year

|

Investment

|

Discounted Cash Flow

|

Cumulative Cash Flow

|

|

0

|

-$12,000

|

$0

|

-$12,000

|

|

1

|

$0

|

$2,294

|

-$9,706 (-$12,000 + $2,294)

|

|

2

|

$0

|

$2,104

|

-$7,602 (-$9,706 + $2,104)

|

|

3

|

$0

|

$1,930

|

-$5,672 (-$7,602 + $1,930)

|

|

4

|

$0

|

$1,771

|

-$3,901 (-$5,672 + $1,771)

|

|

5

|

$0

|

$1,625

|

-$2,276 (-$3,901 + $1,625)

|

|

6

|

$0

|

$1,491

|

-$785 (-$2,276 + $1,491)

|

|

7

|

$0

|

$1,368

|

$583 (-$785 + $1,368)

|

Step 3: Interpret the results.

The cumulative discounted cash flow becomes positive between Years 6 and 7, so the discounted payback period is just over 6 years. If we did not take into consideration the time value of money, the undiscounted payback period would be $12,000 ÷ $2,500 = 4.8 years. Considering the time value of money enables us to calculate a more accurate payoff period.

-

Discounting the payback period can have enormous impacts on profitability. Understanding and accounting for the time value of money is an important aspect of strategic thinking.

-

- Discounted Payback Period

- The amount of time that it takes to cover the cost of a project by adding positive discounted cash flow coming from the profits of the project.

In this lesson, you defined the payback method, which measures how long it takes to recover the initial cost of an investment through cumulative cash inflows. You explored the advantages of this method, including its simplicity, ease of use, and ability to provide a quick comparison between similar projects. You also considered its disadvantages, such as its failure to account for the time value of money, risk, or opportunity cost, making it less suitable for complex investment decisions.

Next, you examined the payback period, where cumulative cash flow is tracked annually until it becomes positive, signaling the breakeven point. While this approach offers a straightforward measure of liquidity and risk, it does not incorporate the cost of capital or post-payback profitability. You then studied the discounted payback period, which improves accuracy by discounting cash inflows using a firm’s cost of capital to reflect the time value of money. This method provides a more realistic measure of investment recovery time and helps firms assess opportunity costs and capital efficiency.

Together, these sections show how the payback method serves as a practical first step in evaluating project feasibility but should be paired with more comprehensive tools, like net present value (NPV) or internal rate of return (IRR) for sound capital budgeting decisions.