In this lesson, you will learn about what life insurance is and the difference between term and permanent life insurance. Specifically, this lesson will cover the following:

1. What Is Life Insurance?

Life insurance might sound complicated, but at its core, it’s pretty straightforward. It’s like a financial agreement between you and an insurance company. You agree to pay a set amount of money, called premiums, either monthly or yearly. In return, the insurance company promises to pay a large sum of money, known as a death benefit, to the people you care about most—your beneficiaries—after you pass away. This payout can help your loved ones with important financial needs, such as the following:

- Covering funeral and burial costs

- Paying off outstanding debts, like a mortgage, credit cards, or student loans

- Keeping up with daily living expenses (such as rent, groceries, or utilities)

- Funding future goals, such as your child’s college education or your partner’s retirement plans

-

The goal of life insurance is simple: to provide a financial cushion for your family so they can focus on healing and moving forward without the added stress of monetary worries.

Here’s a way to think about it: Imagine life insurance as a safety net, like the ones trapeze artists use at a circus. If something unexpected happens and you’re no longer there to support your loved ones financially, the policy steps in like the net, catching them and helping to prevent a free fall into financial hardship. It’s there to protect them from life’s what-if situations.

Two Main Types of Life Insurance: Like Picking Your Favorite Ice Cream

When it comes to life insurance, you’ve got two main options: term life insurance and permanent life insurance. Think of them as two different flavors of ice cream—both satisfying but suited for different tastes and needs.

-

Term Life Insurance: This is the simpler, more budget-friendly option. It lasts for a set period of time, like 10, 20, or 30 years (kind of like renting a house). If you pass away during this term, the policy pays out to your beneficiaries. If not, the policy ends, and you can choose whether to renew or let it go. Term life is great for specific needs, like making sure your kids are covered until they’re adults or your mortgage is paid off.

-

Permanent Life Insurance: This is like owning a home—it’s there for life. As long as you keep paying your premiums, the policy doesn’t expire. Plus, it often comes with a savings or investment component, allowing you to build cash value over time. While it’s more expensive than term life, it offers lifelong coverage and additional financial perks.

The key is to figure out which flavor of life insurance fits your needs and budget best. No matter which one you choose, the purpose remains the same: protecting the people you love most.

-

Here’s a key perk of life insurance: The money your loved ones receive (called the death benefit) is usually tax-free. If your policy pays $500,000, your family gets the full $500,000—no taxes are taken out. There are a few exceptions to this, but they are complex and don’t apply to most individuals.

Let’s take a closer look at term insurance and see what it is all about.

-

- Death Benefit

- The money paid to your beneficiaries when you pass away.

- Term Life Insurance

- Life insurance that provides coverage for a set period (e.g., 10, 20, or 30 years) with no payout if the term ends before you pass.

- Permanent Life Insurance

- Life insurance that lasts your entire life and includes a savings component (cash value) that you can use while alive.

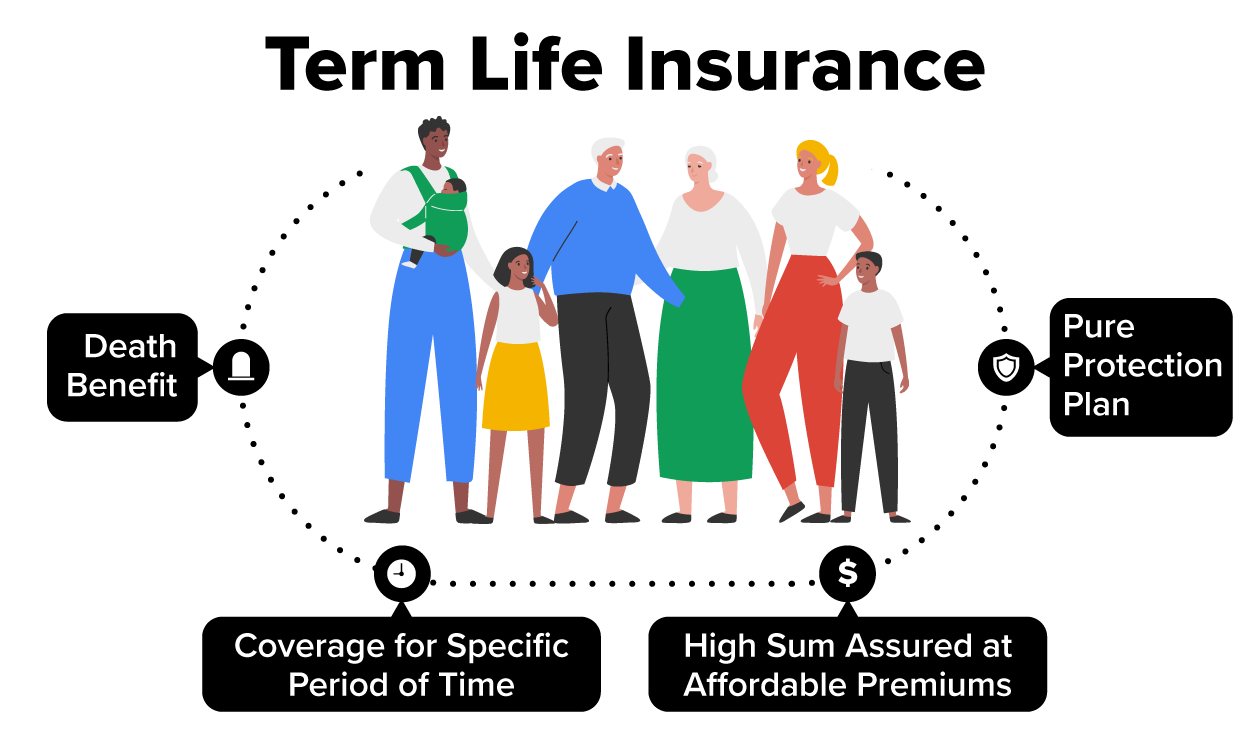

2. Term Life Insurance

Term life insurance is like the starter pack of life insurance—it’s straightforward, budget-friendly, and does exactly what it’s designed to do: provide financial protection for a set period of time. Unlike permanent life insurance, it doesn’t last forever or come with extra features like savings or investment components. Instead, you choose how long you want the coverage to last (the “term”)—typically, 10, 20, or 30 years—and pay a fixed premium during that time. If you pass away during the term, the insurance company pays out the agreed-upon death benefit to your beneficiaries. If the term ends and you’re still alive, the policy expires with no further obligations or payouts.

The appeal of term life insurance lies in its simplicity and affordability. It’s designed to cover specific financial responsibilities that might not last forever, such as the following:

- Raising children until they’re financially independent

- Paying off a mortgage or other large debts

- Replacing your income to help your family maintain their lifestyle

-

EXAMPLE

Let’s say you’re 35 years old, married, and have two young kids. You recently bought a home with a 30-year mortgage and want to make sure your family is financially secure if something happens to you. A 30-year term life insurance policy could be a great fit. Here’s why:

- If you were to pass away unexpectedly during that time, the death benefit could cover the remainder of your mortgage so your family doesn’t have to worry about losing their home.

- It could also replace your income, helping to cover everyday expenses like groceries, childcare, and utilities, so your partner isn’t left scrambling to make ends meet.

- If your goal is to provide for your kids’ future education, the death benefit could help fund college tuition or other big expenses.

Now, imagine you chose a $1 million, 30-year term policy for about $40 a month. That’s roughly the cost of a dinner out, but in exchange, you get peace of mind from knowing that your family would receive $1 million to cover their needs if you’re no longer there to provide for them.

-

Why Term Life Insurance Works for Specific Life Stages

The best part about term life insurance is that it’s flexible—it’s not meant to last forever because your financial needs likely won’t. For example, as your kids grow up, your mortgage gets paid off, and your savings grow, you may find that you no longer need as much life insurance coverage. That’s why term insurance is a great option for many people: It provides coverage during the most vulnerable stages of life when your family relies on your income and financial support the most.

Term life insurance is like renting a financial safety net when you know you need it the most. It’s a simple, cost-effective way to protect your loved ones from the what-if situations in life.

Now, let’s look at permanent life insurance and explore the differences.

3. Permanent Life Insurance

Permanent life insurance is like having a lifelong financial safety net with some built-in perks. It’s designed to cover you for your entire life, as long as you keep paying your premiums. Unlike term life insurance, which only lasts for a specific period, permanent life insurance never expires. It provides a death benefit for your loved ones, but it also does something unique: It builds cash value over time. Think of cash value like a savings account attached to your policy—it grows as you pay premiums, and you can tap into it for financial needs during your lifetime.

Permanent life insurance is great if you want lifelong protection and flexibility. Here’s why it stands out:

- Lifetime coverage: Your loved ones are guaranteed to receive the death benefit, no matter when you pass away, as long as the policy stays active. Most policies are designed to last until the age of 100 or 120.

- Cash value growth: Part of your premium goes into a savings-like account that grows tax-deferred. You can borrow or withdraw from this cash value for emergencies, retirement, or other big expenses.

- Predictable costs: Many permanent policies come with fixed premiums, so you don’t have to worry about rising costs as you get older.

-

EXAMPLE

Let’s say you’re in your 30s, have a growing family, and you’re thinking about the future. You decide to buy a whole life insurance policy (a type of permanent life insurance) with a $500,000 death benefit. You pay your monthly premiums, and over time, the policy’s cash value starts to grow. By the time you’re in your 50s, the cash value has built up to $50,000.

Now, imagine you need extra funds for a down payment on a vacation home or to help pay for your child’s college tuition. You can borrow against the $50,000 cash value at a low interest rate—no credit check needed. You’re essentially borrowing from yourself. Or, if you decide not to use the cash value, it keeps growing, adding more financial flexibility for the future.

Fast forward to retirement: In your 60s or 70s, that cash value could grow to $150,000 or more. You could use it to supplement your retirement income, cover unexpected medical expenses, or even fund that dream trip to Italy. And if you never use the cash value, your family will still receive the $500,000 death benefit when you pass away.

Permanent life insurance is more than just a safety net for your family—it’s a versatile asset that grows with you. For example:

- If you want to leave a financial legacy, the death benefit ensures that your loved ones are taken care of no matter when you pass away.

- If you’re planning for retirement, the cash value can act as a backup savings account or give you extra income when you need it most.

- If you want financial flexibility, you can use the cash value for things like starting a business, covering emergencies, or paying off debts.

-

Think of permanent life insurance as owning a home that builds equity over time. You have a place of security, but you can also use that equity (the cash value) when you need it. While it’s more expensive than term insurance, the added benefits—like lifelong coverage and a growing financial resource—make it a valuable tool for people who want protection and flexibility for every stage of life.

There are four main types of permanent life insurance. Let’s learn more about them.

-

- Cash Value

- A savings feature in permanent life insurance that grows over time and can be accessed or borrowed while you’re alive.

3a. Types of Permanent Life Insurance

Permanent life insurance isn’t a one-size-fits-all solution. It comes in a few different flavors, so you can choose the type that works best for your needs, goals, and budget. All of them provide lifelong coverage and build cash value, but the way they work—and how much flexibility they offer—can vary. Let’s break down the main types of permanent life insurance in a simple and relatable way.

1. Whole Life Insurance: The Reliable Choice

Whole life insurance is like the classic vanilla ice cream of the permanent life insurance world—simple, steady, and predictable. It offers the following:

- Fixed premiums: You’ll pay the same amount every month or year, so you never have to worry about rising costs.

- Guaranteed cash value growth: Your cash value grows at a steady rate, and you’ll know exactly how much it will be worth at any given time.

- A guaranteed death benefit: Your loved ones will receive a set amount of money when you pass away.

This type of insurance is great if you like structure and predictability. It’s ideal for people who want a straightforward policy that grows slowly and steadily over time.

Imagine you’re someone who loves routine and predictability—like knowing you’ll get your favorite coffee every morning. Whole life insurance gives you that same sense of stability. You pay the same premium, watch your cash value grow, and trust that your family will be financially secure no matter what.

2. Universal Life Insurance: The Flexible Option

Universal life insurance is like a build-your-own sundae bar. It offers more flexibility than whole life insurance, allowing you to adjust certain aspects of your policy as your life changes. Here’s what makes it unique:

- Flexible premiums: You can adjust how much you pay, as long as you meet the minimum requirement to keep the policy active.

- Adjustable death benefit: Need more coverage down the road? You can increase (or decrease) your death benefit.

- Cash value growth: The cash value grows based on interest rates, which can vary, so it’s a little less predictable than whole life insurance.

This type of insurance is great for people who want some control over their policy and need it to adapt as their financial situation changes.

Let’s say you’re a freelancer with an income that fluctuates. Some months are great and you can afford higher premiums, while other months are tighter. With universal life insurance, you have the flexibility to adjust your payments and still keep your policy active.

3. Variable Life Insurance: The Investor’s Choice

Variable life insurance is like the stock market version of permanent life insurance. It gives you the chance to grow your cash value faster by investing it in stocks, bonds, or other market-based options. We’ll discuss investing in an upcoming lesson, but for now, here’s how variable life insurance works:

- Investment opportunities: Your cash value is tied to investment accounts, which means that it can grow faster if the market does well.

- Higher risk, higher reward: While you could see big gains, there’s also the risk that your cash value might decrease if the market takes a downturn.

- Fixed premiums: Like whole life insurance, your premiums typically stay the same.

This type of insurance is ideal for people who are comfortable with investing and want their life insurance policy to work harder to grow wealth.

Picture yourself as someone who enjoys taking calculated risks, like playing the stock market or investing in real estate. Variable life insurance gives you the chance to grow your cash value faster—but you also need to keep an eye on your investments.

4. Indexed Universal Life Insurance: A Hybrid Approach

Indexed universal life insurance (IUL) combines the flexibility of universal life with the growth potential of investments—but without the full risk of the stock market.

This type of insurance is great for people who want a balance of growth potential and protection from market volatility.

Think of IUL as a safer version of investing. It’s like enjoying a roller coaster with seat belts and extra safety harnesses—you get some of the thrills of market growth but with guardrails to protect your cash value from big losses.

How to Choose the Right One:

Picking the right type of permanent life insurance depends on your financial goals and personality:

- If you value predictability, whole life might be your best bet.

- If you want flexibility, universal life could be the perfect fit.

- If you’re comfortable with investments and risk, variable life could help you grow wealth faster.

- If you’re looking for a balance between growth and safety, indexed universal life offers the best of both worlds.

No matter which type you choose, the goal remains the same: lifelong protection and financial peace of mind for you and your family.

Life insurance is an essential part of your financial tool kit. Whether you choose term or permanent insurance, the goal is the same: to protect your loved ones and give yourself peace of mind. By understanding the differences between these two options, you’re better equipped to make a choice that aligns with your goals and budget.

If you’re just starting out, term insurance is often the easiest and most affordable way to get the coverage you need. As your financial situation evolves, you can explore adding permanent insurance to the mix if it makes sense for your goals.

-

- Whole Life Insurance

- A permanent life insurance policy with fixed premiums, a guaranteed death benefit, and cash value that grows at a set rate.

- Universal Life Insurance

- A flexible permanent policy where you can adjust premiums and death benefits, with cash value that grows based on interest rates.

- Variable Life Insurance

- A permanent policy with cash value that you can invest in options like stocks and bonds, making it riskier but with higher growth potential.

- Indexed Universal Life Insurance

- A permanent policy with cash value growth tied to stock market indexes, offering the potential for higher returns with some protection against market losses.

In this lesson, you discovered what life insurance is. You also learned what term life insurance and permanent life insurance are, as well as the different types of permanent life insurance.