Table of Contents |

Debt has this sneaky way of creeping into your life and sticking around, making it feel like you’re in a hamster wheel—working hard but never getting anywhere. You’re not alone in feeling this way, and here’s the truth: Getting out of debt is possible, no matter how overwhelming it feels right now. Whether it’s the weight of student loans, high-interest credit card balances, or those nagging car payments, the first step to freedom is facing your debt head-on.

Think of it as starting a new fitness routine: You need to step on the scale to see where you’re at. It might not be fun, but it’s necessary to move forward. Facing your debt isn’t about shame—it’s about taking control of your financial story. Let’s look at two simple steps for getting clear about what debt you have.

Step 1: Get a Clear Picture

The first step to tackling your debt is getting crystal clear about what you owe. It’s time to lay it all out—every balance, big or small. Think of this as your financial reality check. Most of us either underestimate how much debt we have or don’t fully understand the details, like interest rates or payment terms. But don’t worry, this isn’t about judgment; it’s about taking control. The clearer you are, the stronger your plan will be—because clarity really is your superpower!

EXAMPLE

Here’s an example of what your debt list might look like:

Step 2: Find Your “Why”

Getting out of debt isn’t just about the numbers—it’s about freedom. Why do you want to be debt-free? Is it to stop the late-night anxiety about money? To save for a house? To finally quit that job you hate and start your own business?

Your “why” is the thing that will keep you going when paying off debt feels hard. It’s your North Star, guiding you toward the life you want to create.

EXAMPLE

“I want to be debt-free so I can save for a down payment on a house and give my kids the stability I never had growing up.”Now that you’ve taken the brave step of listing your debts and understanding exactly where you stand, give yourself a moment to breathe. Yes, seeing the total might feel overwhelming, but remember this is the first step toward changing your financial future. You now have the clarity and knowledge you need to move forward.

The next step is all about action. Knowing your debt is one thing, but tackling it with a plan that fits your personality and situation is where the magic happens. You don’t need to wing it or guess your way through—you can use proven debt payoff strategies to build momentum and crush those balances one by one. Let’s talk about them.

We’re going to dive into two of the most effective debt payoff strategies: the snowball method and the avalanche method. Both are designed to help you pay off debt in a structured, manageable way, but they take slightly different approaches. By understanding how they work, you’ll be able to choose the one that fits your goals and keeps you motivated.

Ready to find your path to debt freedom? Let’s explore each method in detail.

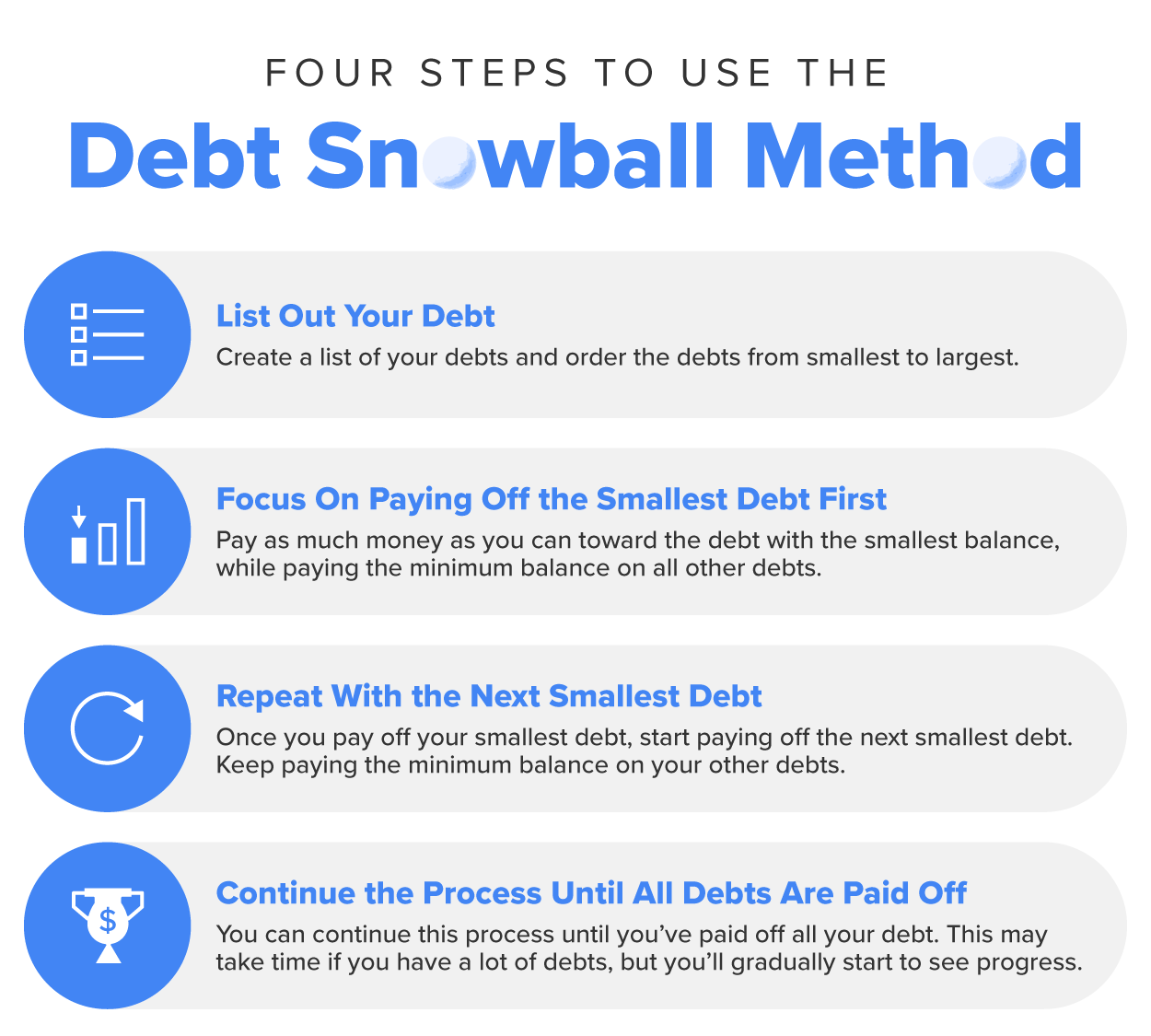

The snowball method focuses on building confidence by tackling your smallest debts first. Think of it as rolling a tiny snowball down a hill—it starts small, but as it picks up speed, it grows bigger and stronger.

How It Works

EXAMPLE

For this example, let’s say you have the following debts:The snowball method is effective because it provides quick wins that give you instant gratification. When you pay off a small debt, it feels like a huge accomplishment, and that sense of victory helps you build momentum to tackle the next debt. Each debt you pay off becomes a confidence boost, reminding you that progress is possible. This approach keeps your motivation high and makes the process feel manageable, even when the total debt feels overwhelming.

Potential Drawbacks

The main downside to the snowball method is that you might pay more in interest over time. Since this strategy focuses on the smallest balances rather than the highest interest rates, you’re not necessarily eliminating the most expensive debts first. However, the tradeoff is often worth it if staying motivated is your biggest challenge.

Who It’s Best For

The snowball method is ideal for people who feel overwhelmed by debt and need emotional wins to stay motivated. If you’re someone who loves the satisfaction of crossing things off a to-do list or seeing quick results, this method can help you stay focused and energized throughout your debt payoff journey.

Now that you’re a pro at the snowball method, let’s talk about the second debt payoff strategy, the avalanche method.

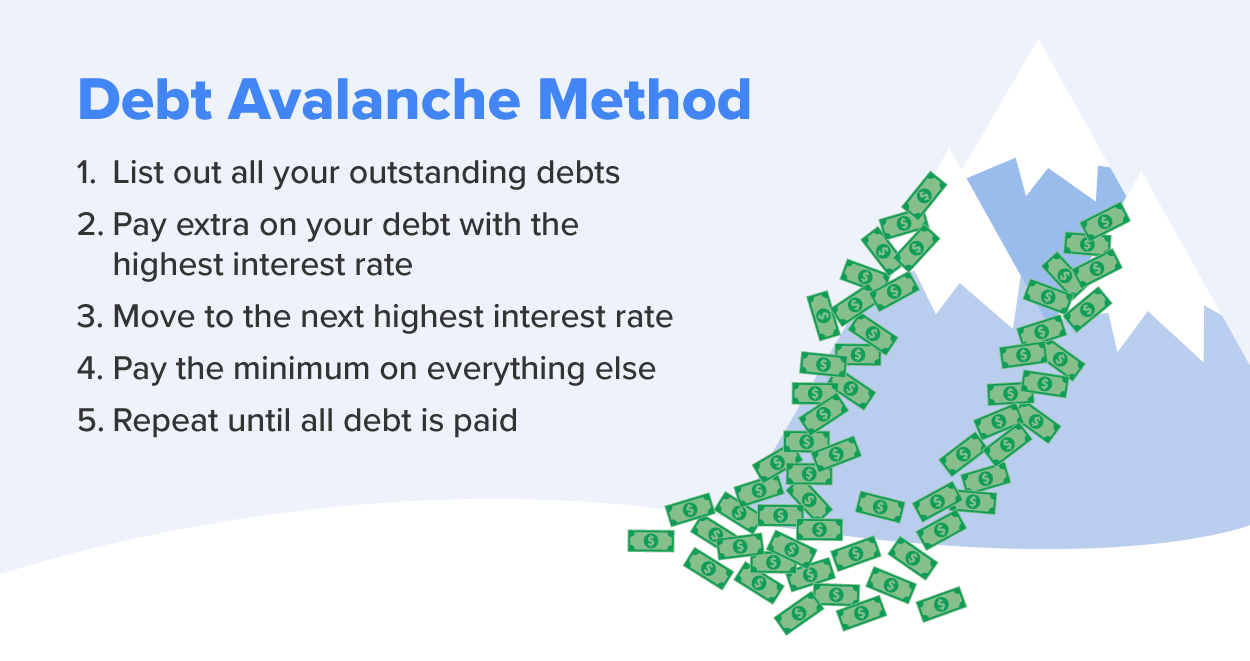

The avalanche method is for people who love efficiency and want to minimize the total cost of their debt. Instead of focusing on balances like the snowball method, this method prioritizes high-interest debts.

How It Works

EXAMPLE

For this example, let’s revisit the debts from the previous example, organized by interest rate:The avalanche method is highly effective because it saves you the most money over time. By focusing on the debts with the highest interest rates first, you reduce the total amount you’ll pay in interest. This makes it the most mathematically efficient way to pay off debt, ensuring that every extra dollar you put toward your balances works harder for you.

Potential Drawbacks

One challenge with the avalanche method is that progress can feel slower, especially if your highest-interest debt has a large balance. It might take longer to pay off your first debt, which can be discouraging if you thrive on immediate results. Without quick wins, there’s also a risk of losing motivation before you see the payoff.

Who It’s Best For

The avalanche method is perfect for people who are focused on saving as much money as possible in the long run. It’s also a great fit for those who are comfortable with delayed gratification and are motivated by the bigger picture rather than immediate results.

Now that you have an understanding of both methods, let’s look closer at which method you should choose. Remember, there isn’t a right or wrong method, only the method that will work best for you and keep you motivated while you’re paying off debt.

You’ve learned about the two payoff methods; the next big question is which method you should use. Choosing the right debt payoff method comes down to understanding what drives you and keeps you motivated.

Both the snowball method and the avalanche method are effective in their own ways, but their success depends on how well they fit your personality and financial goals.

Do you thrive on the excitement of quick wins and need those small victories to stay energized?

Or are you more focused on long-term efficiency and saving as much money as possible, even if progress feels slower at first?

Let’s explore how to make this decision and set yourself up for success.

Your debt payoff strategy should match your unique financial reality. Whether you’re struggling to make ends meet or have some extra cash to throw at your balances, there’s a plan that works for you.

Here are three common scenarios and strategies to help you decide:

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.