This lesson discusses the uses of standard costs, the advantages and disadvantages of using standard costs, and the method of computing the difference or variance between an actual cost and a standard cost. We will discuss how managers can improve efficiency by investigating variances and taking corrective action. Specifically, we will discuss the following:

1. Standard Costs

In the previous lesson, we discussed setting goals and creating budgets to help us achieve those goals. In this lesson, we learn how to evaluate the results of budget setting by comparing our actual costs to established standards. This will allow us to diagnose why we did or did not reach our goals and determine where the problem might lie.

Whenever an organization has set goals it has sought to achieve, these goals can be called standards. Periodically, you can measure your actual performance against these standards and analyze the differences to see how close you are to your goal. Similarly, management sets goals, such as standard costs, and compares actual costs with these goals to identify possible problems.

A standard cost is a carefully predetermined measure of what a cost should be under stated conditions. Standard costs are not only estimates of what costs will be but also the goals to be achieved. When standards are properly set, their achievement represents a reasonably efficient level of performance.

Usually, effective standards are determined by running engineering studies and time and motion studies; these are studies that observe and measure all the tasks and motions completed by worker and robot labor in order to identify inefficiencies. These studies are undertaken to determine the amounts of materials, labor, and other services required to produce a product, and the results are used to develop standards. General economic conditions are also considered in setting standards because these conditions affect the cost of materials and other services that must be purchased by a manufacturing company.

Manufacturing companies determine the standard cost of each unit of product by establishing the standard cost of direct materials, direct labor, and variable manufacturing overhead necessary to produce that unit.

-

- Standards

- Set goals an organization wishes to achieve.

- Standard Cost

- A predetermined measure of what the cost should be under stated conditions.

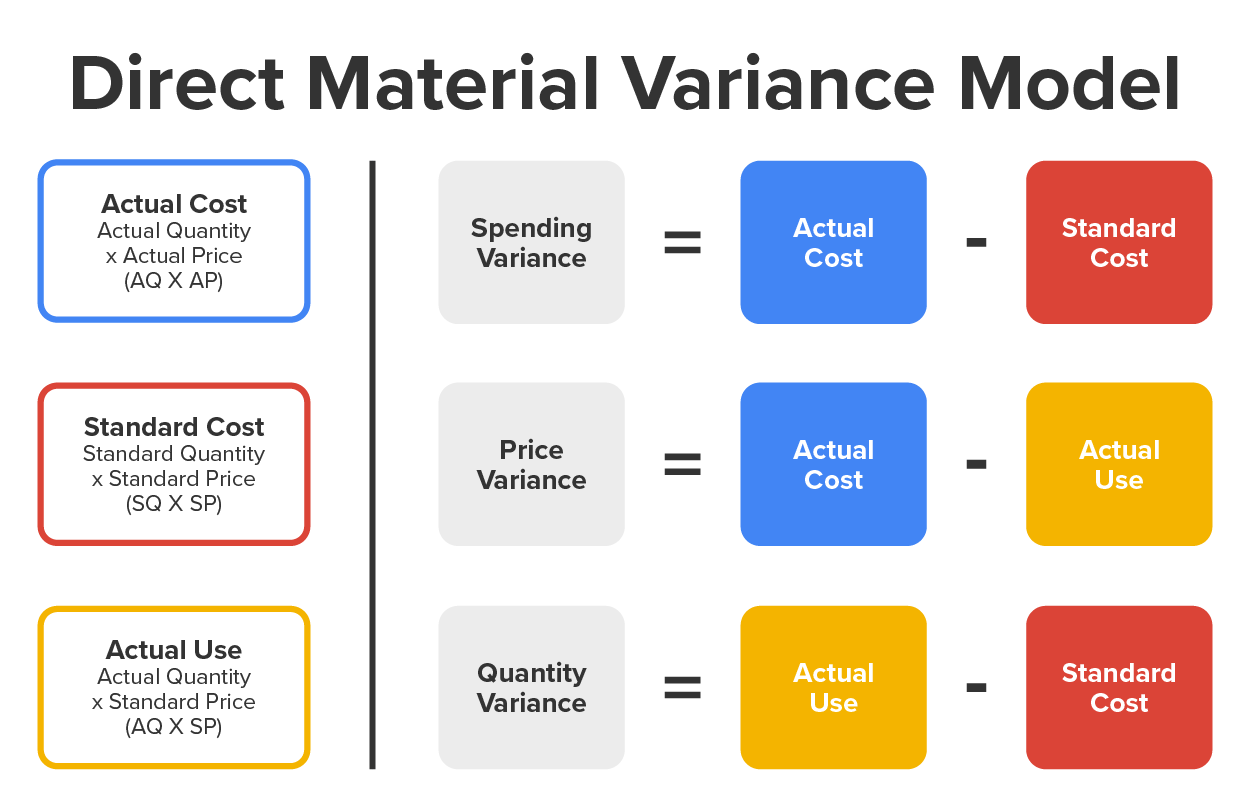

2. Direct Materials Variance

The standards that are used to determine the measurement of a company’s performance concerning direct materials are the standard quantity per unit and the standard price per unit. The standard quantity per unit is the amount of direct materials that the production department should use to produce one finished product. The standard price per unit is the cost of each unit of direct materials that should be paid per the standard. Once a company has established its standard quantity per unit and standard price per unit, the standard direct material cost per unit can be calculated by multiplying the two.

The direct material quantity and price variances are classified as either favorable or unfavorable. In general, if the actual prices paid or quantities used are lower than the standard, then the variance is considered favorable; if they are greater than the standard, then the variance is considered unfavorable. Thus, if the actual price paid for materials is less than the standard price, the price variance is considered favorable; if the actual price paid for materials is greater than the standard price, the price variance is considered unfavorable. Likewise, if the actual quantity of materials used is less than the standard quantity of materials used, the quantity variance is considered favorable; if the actual quantity of materials used is greater than the standard quantity of materials used, the quantity variance is considered unfavorable.

-

Remember that accountants often use parentheses in place of a negative sign to indicate a negative difference. A variance of 5 would be considered unfavorable, and a variance of (5) would be considered favorable.

-

- Standard direct material cost per unit formula

- Standard quantity per unit x standard cost price per unit = Standard direct material cost per unit

-

EXAMPLE

MoTown Racing Tires, Inc., produces tires for automotive racing applications. Each tire produced requires 10 lb of rubber, and each pound of rubber costs $5.00. Multiplying the standard quantity per unit (10 lb) by the standard cost price per unit ($5.00 per pound) results in a standard direct material cost per unit of $50.00 of direct materials for each tire.

Once a company has established its standards, the next step is to compute the direct material variances from the budget for the period that has just passed. We compute both a price variance and a quantity variance. The price variance is the difference between the amount that was actually paid for direct materials and the standard amount that should have been paid, while the quantity variance is the difference between how much material was actually used to produce the actual production level and the amount that should have been used by the standard.

Once we solve the price and quantity variances, we then calculate the spending variance, which is a comparison of the actual quantity used at the actual price paid versus the standard quantity that should be used at the standard price. The spending variance can also be calculated by combining the price and quantity variances.

To simplify these calculations, we use the following direct materials variance model:

-

EXAMPLE

Using the direct materials variance model, we compute the price variance, quantity variance, and spending variance for MoTown Racing Tires. MoTown has the following direct materials standards:

- Standard quantity per unit: 10 lb of rubber per tire

Standard price per unit: $5.00 per pound of rubber

During the month of February, 4,000 tires were produced using a total of 42,000 lb of rubber at a total cost of $205,800. The total cost of $205,800 divided by 42,000 lb equals $4.90 per pound. The standard quantity of rubber to be used to produce 4,000 tires is 4,000 tires multipled by 10 lb of rubber per tire, which equals 40,000 lb.

Price variance = Actual cost − actual use

Price variance = $205,800 − $210,000 = ($4,200)

The price variance is favorable.

Spending variance = Actual cost − standard cost

Spending variance = $205,800 − $200,000 = $5,800

The spending variance is unfavorable.

Quantity variance = Actual use − standard cost

Quantity variance = $210,000 − $200,000 = $10,000

The quantity variance is unfavorable.

-

When determining variances, convert to total costs.

Step 1 : Multiply the actual total units of production by the appropriate standard cost per unit to get the standard cost amount.

- Actual Total Units Produced x Standard Cost Per Unit = Standard Cost

Step 2: Then compare standard cost to the actual total cost to determine if the costs predicted (standard costs) were more or less than actual costs.

- If actual costs < standard costs, there is a favorable variance.

- If actual costs > standard costs, there is an unfavorable variance.

-

Sensory Slime, Inc., has the following direct materials standards:

- Standard quantity per unit: 4 oz of polymer per unit

Standard price per unit: $0.05 per ounce of polymer

During the month of January, 25,000 units of slime were produced using a total of 98,000 oz of polymer at a total cost of $5,880: $5,880 / 98,000 lb = $0.06 per ounce. The standard quantity of polymer to be used to produce 25,000 units of slime is 100,000 oz: 25,000 units x 4 oz of polymer per unit = 100,000 oz.

-

- Standard Quantity per Unit

- The amount of direct materials that the production department should use to produce one finished product.

- Standard Price per Unit

- The cost of each unit of direct materials that should be paid per the standard.

- Standard Direct Material Cost per Unit

- The standard cost of materials to produce a single finished unit.

- Price Variance

- The difference in the amount that was actually paid for direct materials and the standard amount that should have been paid.

- Quantity Variance

- The difference between how much material was actually used to achieve the actual production level and the amount that should have been used by the standard.

- Spending Variance

- A comparison of the actual quantity used at the actual price paid versus the standard quantity that should be used at the standard price.

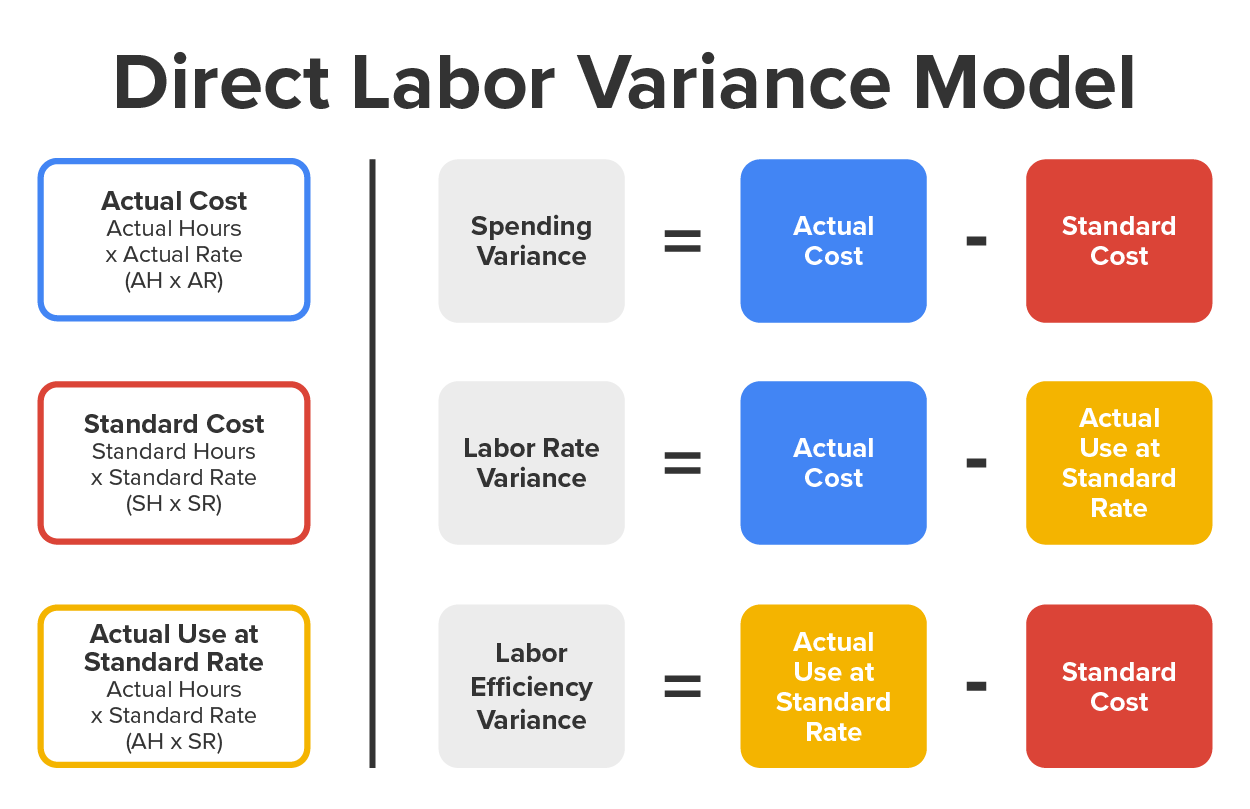

3. Direct Labor Variances

In addition to measuring materials variances, a company will also want to measure how far the actual direct labor costs deviate from the budgeted figures. Similar to direct materials, we calculate three variances for direct labor. The direct labor rate variance measures the difference in labor cost when the actual number of direct labor hours is applied to both the actual labor rate and the standard labor rate. The standard labor rate is the hourly rate that should be paid for direct labor that includes employment taxes and benefits.

The second variance is the labor efficiency variance, which measures the difference in labor hours actually used in production as compared to the number of hours that should have been used based on the standard direct labor hours per unit. Standard direct labor hours per unit is the number of direct labor hours that should be committed to producing a single unit.

Finally, we calculate the spending variance, which is a comparison of the actual labor hours used at the actual rate paid versus the standard labor hours that should be used at the standard rate. The spending variance can also be calculated by combining the rate and efficiency variances.

To simplify these calculations, we use the direct labor variance model:

-

EXAMPLE

MoTown Racing Tires, Inc., has the following direct labor standards:

- Standard direct labor hours per unit: 0.5 direct labor hours per tire

Standard labor rate per hour: $20.00 per hour

During the month of February, 4,000 tires were produced using a total of 1,900 direct labor hours at a total cost of $40,850. Total cost of $40,850 divided by 1,900 hours equals $21.50 per hour. The standard number of direct labor hours to be used to produce 4,000 tires is 4,000 tires times 0.5 hours per tire, which equals 2,000 hours.

Labor rate variance = Actual cost − actual use at standard rate

Labor rate variance = $40,850 − $38,000 = $2,850

The labor rate variance is unfavorable.

Spending variance = Actual cost − standard cost

Spending variance = $40,850 − $40,000 = $850

The spending variance is unfavorable.

Labor efficiency variance = Actual use at standard rate − standard cost

Labor efficiency variance = $38,000 − $40,000 = ($2,000)

The labor efficiency variance is favorable.

-

Sensory Slime, Inc., has the following direct labor standards:

- Standard direct labor hours per unit: 0.1 direct labor hours per unit

Standard labor rate per hour: $12.00 per hour

During the month of January, 25,000 units of slime were produced using a total of 2,400 direct labor hours at a total cost of $32,400: $32,400 / 2,400 lb = $13.50 per hour. The standard number of direct labor hours needed to produce 25,000 units of slime is 2,500 hours: 25,000 units x 0.1 direct labor hours per unit = 2,500 hours.

-

- Direct Labor Rate Variance

- A measurement of the difference in labor cost when the actual number of direct labor hours is applied to both the actual labor rate and the standard labor rate.

- Standard Labor Rate

- The hourly rate that should be paid for direct labor that includes employment taxes and benefits.

- Labor Efficiency Variance

- A measurement of the difference in labor hours actually used in production as compared to the number of hours that should have been used based on the standard direct labor hours per unit.

- Standard Direct Labor Hours per Unit

- The number of direct labor hours that should be committed to producing a single unit.

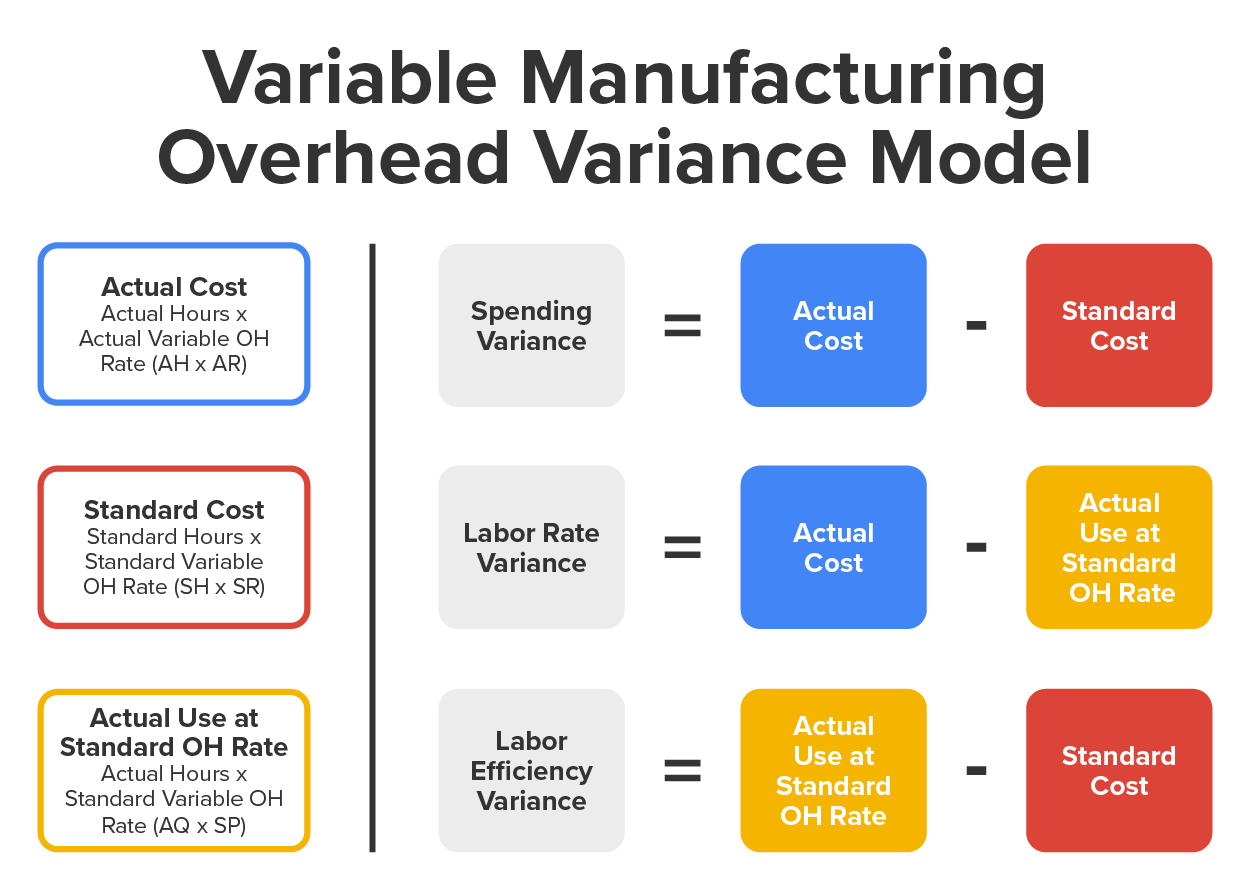

4. Variable Manufacturing Overhead Variances

Variable manufacturing overhead variances are very similar to direct labor variances, particularly when the allocation base is direct labor hours, which is what we will use for all of our examples. We once again calculate three variances for variable manufacturing overhead. The variable overhead rate variance measures the difference in variable overhead cost when the actual number of direct labor hours is applied to both the actual variable overhead rate and the standard rate. The standard variable overhead rate is the variable overhead cost per unit that was used to calculate the company’s predetermined overhead rate.

The variable overhead efficiency variance measures the difference in labor hours actually used in production as compared to the number of hours that should have been used based on the standard direct labor hours per unit. Standard direct labor hours per unit refer to the number of direct labor hours that should be committed to producing a single unit.

We then calculate the spending variance, which is a comparison of the actual labor hours used at the actual variable overhead rate paid versus the standard labor hours that should be used at the standard rate. The spending variance can also be calculated by combining the rate and efficiency variances.

To make these computations easy, we use the following variable manufacturing overhead variance model:

-

EXAMPLE

MoTown Racing Tires, Inc., has the following variable manufacturing overhead standards:

- Standard direct labor hours per unit: 0.5 direct labor hours per tire

Standard variable overhead rate per hour: $4.00 per direct labor hour

During the month of February, 4,000 tires were produced using a total of 1,900 direct labor hours at a total variable overhead cost of $7,315.A total variable overhead cost of $7,315 divided by 1,900 hours equals $3.85 per direct labor hour. The standard number of direct labor hours to be used to produce 4,000 tires is 4,000 tires multiplied by 0.5 hours per tire, which equals 2,000 hours.

Labor rate variance = Actual cost − actual use at standard overhead rate

Labor rate variance = $7,315 − $7,600 = ($285)

The labor rate variance is favorable.

Spending variance = Actual cost − standard cost

Spending variance = $7,315 − $8000 = ($685)

The spending variance is favorable.

Labor efficiency variance = Actual use at standard overhead rate − standard cost

Labor efficiency variance = $7,600 − $8,000 = ($400)

The labor efficiency variance is favorable.

-

Sensory Slime, Inc., has the following variable manufacturing overhead standards:

- Standard direct labor hours per unit: 0.1 direct labor hours per unit

Standard variable overhead rate per hour: $2.50 per hour

During the month of January, 25,000 units of slime were produced using a total of 2,400 direct labor hours at a total cost of $6,600: $6,600 / 2,400 lb = $2.75 per hour. The standard number of direct labor hours needed to produce 25,000 units of slime is 2,500 hours: 25,000 units x 0.1 direct labor hours per unit = 2,500 hours.

-

- Variable Overhead Rate Variance

- The difference in variable overhead cost when the actual number of direct labor hours is applied to both the actual variable overhead rate and the standard rate.

- Standard Variable Overhead Rate

- The variable overhead cost per unit that was used to calculate the company’s predetermined overhead rate.

- Variable Overhead Efficiency Variance

- The difference in labor hours actually used in production as compared to the number of hours that should have been used based on the standard direct labor hours per unit.

In this lesson, we discussed the use of standard costing and variances in order to improve efficiency and develop corrective action plans when necessary. The goals that a company sets are called standards, therefore, a standard cost is a predetermined measure of what a cost should be under certain standards. Manufacturing companies determine the standard cost of each unit of product by establishing the standard cost of direct materials, direct labor, and variable manufacturing overhead that is needed to produce each unit.

We also discussed the direct materials variance, which are the standards that are used to determine the measurement of a company’s performance concerning direct materials. The direct materials variance includes the standard quantity per unit and the standard rice per unit. The standard quantity per unit is the amount of direct materials that the production department should use to produce one finished product. The standard price per unit is the cost for each unit of direct materials that should be paid per the standard. Multiplying the standard quantity per unit and the standard price per unit together will provide the standard direct material cost per unit. The variances are classified as either favorable or unfavorable. A variance is favorable if the actual amount is less than the standard and it is unfavorable if the actual amount is higher than the standard.

The direct labor variances allow management to measure how far the actual direct labor costs divert from the budgeted figures. The variances that are calculated include the direct labor rate variance, the labor efficiency variance, and the spending variance. The direct labor rate variance measures the difference in labor cost when the actual number of direct labor-hours are applied to both the actual labor rate and the standard labor rate. The labor efficiency variance measures the difference in labor hours actually used in production as compared to the number of hours that should have been used based on the standard direct labor-hours per unit. Finally, the spending variance consists of a comparison of the actual labor-hours used at the actual rate paid versus the standard labor-hours that should be used at the standard rate.

Additionally, we learned about the variable manufacturing overhead variance which consists of the variable overhead rate variance, the variable overhead efficiency variance, and the spending variance. The variable overhead rate variance measures the difference in variable overhead cost when the actual number of direct labor-hours are applied to both the actual variable overhead rate and the standard rate. The variable overhead efficiency variance measures the difference in labor hours that are actually used in production in comparison to the number of hours that should have been used based on the standard direct labor-hours per unit. The spending variance compares the actual labor-hours used at the actual variable overhead rate paid versus the standard labor-hours that should be used at the standard rate.