Here we are at the second exception to depreciating an asset, AKA, the tax plot twist number two! Special (bonus) depreciation allowance.

The special depreciation allowance (also called simply “special depreciation” or “bonus depreciation”) is a deduction available in the first year certain qualifying property is placed into service for use in a trade or business. The deduction is based on a percentage (usually either 50% or 100%) of the cost of the asset.

For 2022, the special depreciation allowance is 100% of the cost of qualifying property placed into service during the tax year.

The allowance is calculated on a depreciable basis. If the taxpayer applies the Section 179 deduction, this will reduce the depreciable basis available for bonus depreciation. After figuring the special depreciation allowance for qualified property, the remaining cost can be depreciated under the regular MACRS depreciation deduction.

EXAMPLE

On July 1, 2022, Jan purchased and placed in service a computer for her bookkeeping business in the amount of $3,000. Jan did not elect to claim a Section 179 deduction. Jan may deduct up to 100% of the cost as a special depreciation allowance for 2022. If Jan decides to deduct 100% of the cost as a special depreciation allowance for 2022, she will have no remaining cost to figure a regular MACRS depreciation deduction for the property for 2022 and later years.Special depreciation has been the subject of significant legislation in the past few decades. The percentage has changed from 50% to 100% over the years.

Qualified property must be placed into service before January 1, 2027, and generally includes the following:

A few things to keep in mind regarding qualifying property for bonus depreciation:

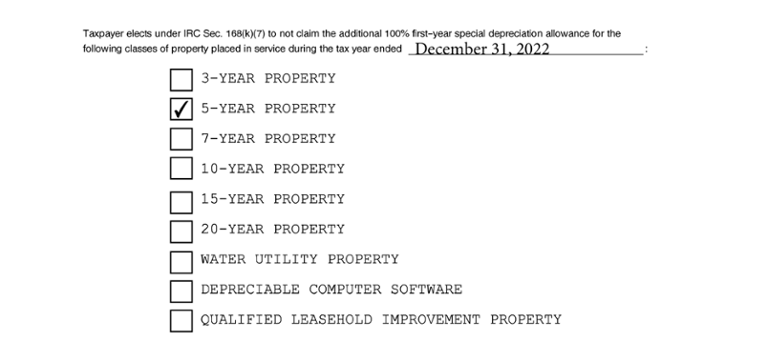

Claiming special depreciation is optional, but in the years when special depreciation is allowed, it is the default position for taxpayers who placed qualifying property into service. Taxpayers who do not wish to claim the allowance must attach a statement to the tax return to affirmatively opt out. The decision to opt out of special depreciation applies to all property in an asset class placed in service in that year.

A taxpayer opts out by attaching a statement to their tax return indicating the class of property for which they would like to opt out.

EXAMPLE

Morgan has four properties she is going to depreciate in 2022. Two of them are 5-year class property, and the other two are 7-year class property. Morgan decides to opt out of using special depreciation for her 5-year class of property. She will have to elect to do so on her tax return. She must opt out of bonus depreciation for all of her 5-year property and cannot opt out on only one of those assets. She could, however, opt out of bonus depreciation for all of her 5-year class property and not opt out for her 7-year class property.