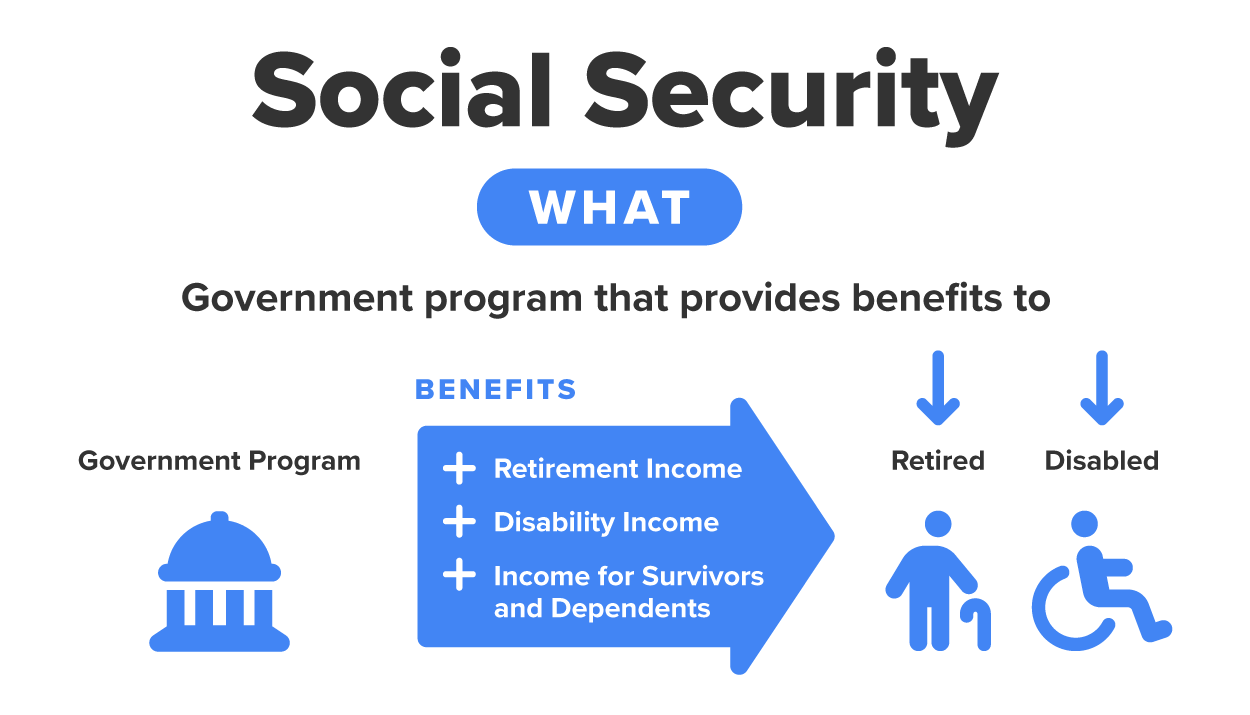

Social Security is like a giant financial safety net created by the U.S. government to provide support for people when they retire, become disabled, or lose a family member who was a worker. Think of it as a system where workers contribute a little from their paychecks while they’re working, and, in return, they receive financial support later in life when they need it.

did you know

This system was created in 1935 during the Great Depression, a time when millions of Americans had lost their jobs and savings. Before Social Security, many older adults had no reliable income once they could no longer work. The government stepped in with a plan to make sure that workers who spent their lives contributing to the economy wouldn’t be left without financial support in their later years. Over time, Social Security expanded to include people with disabilities and the families of workers who passed away, ensuring that those facing financial hardships weren’t left struggling alone.

President Franklin D. Roosevelt signing the Social Security Act on August 14, 1935Source: Library of Congress

But why should you care about Social Security right now? Because it’s a system that directly affects you—even if you don’t realize it yet. If you have a part-time job, you’re already contributing to Social Security, and, someday, you’ll benefit from it. Whether you work at a fast-food restaurant or a bookstore or have a side gig, a portion of your paycheck goes into this system. Plus, understanding Social Security now will help you make smart financial choices in the future, like planning for retirement (yes, even though it feels light-years away!).

The Social Security Process

Social Security is funded through taxes taken out of workers’ paychecks. When you look at your paycheck stub, you might see a deduction labeled FICA (Federal Insurance Contributions Act), which is how the government collects money to keep Social Security running.

Here’s a simple breakdown of how the system works:

1. Workers Pay Into Social Security

a. Every time you earn a paycheck, 6.2% of your earnings is taken out and sent to the Social Security system.

b. Your employer also matches this by paying another 6.2% on your behalf.

c. If you are self-employed, you pay both portions yourself—which means a total of 12.4% of your income goes to Social Security.

2. The Money Goes to Current Recipients

a. Social Security works like a giant piggy bank, but instead of saving your money for just you, your contributions help fund benefits for today’s retirees, disabled individuals, and survivors of deceased workers.

b. In other words, when your grandparents receive Social Security checks each month, part of that money comes from what today’s workers are contributing.

3. Your Earnings Are Recorded for the Future

a. Even though your paycheck deductions are helping today’s recipients, the Social Security Administration (SSA) keeps track of how much you’ve paid into the system over your lifetime.

b. When it’s your turn to retire (usually around age 67 for full benefits), the government calculates how much you should receive based on how much you contributed during your working years.

EXAMPLE

Let’s say you work at a local coffee shop and earn $500 per month:

Your paycheck deduction: $31 (6.2% of $500) goes to Social Security.

Your employer’s contribution: Your employer also adds another $31 to the system on your behalf.

Total going into Social Security: $62 per month goes from just your job alone.

Now imagine millions of workers across the country making similar contributions every month. That’s how Social Security remains funded and provides financial support to people who need it.

While most people think of Social Security as something only retired people receive, it actually provides benefits in other situations, too:

Disability benefits (SSDI): If someone becomes disabled and is unable to work, they may qualify for Social Security disability benefits.

Survivor Benefits: If a worker passes away, their spouse, children, or other dependents may be able to receive financial support.

Early Benefits: While the full retirement age is typically 67, some people start receiving reduced benefits as early as age 62.

Even though retirement may seem a million years away, Social Security is still an important part of your financial future. Here’s why:

1. It’s already affecting your paycheck: Whether you work part-time or full-time or run your own business, Social Security taxes are coming out of your earnings.

2. It will be there when you need it: Even if you never need disability or survivors’ benefits, Social Security is something you’ll rely on when you retire.

3. It’s a piece of your financial puzzle: Social Security is just one piece of the puzzle when it comes to financial security in retirement. You’ll also want to save money on your own through 401(k)s, IRAs, and investments to ensure a comfortable future.

Now that you understand how Social Security is funded and why it matters, you might be wondering, “How do people actually receive Social Security benefits?”

Since Social Security is a system where today’s workers fund benefits for current recipients, you may not see the money you’re contributing for decades. But when it’s time to collect benefits—whether due to retirement, disability, or other circumstances—Social Security follows specific rules to determine who qualifies, how much they receive, and when they can start collecting.

Let’s dive into how Social Security benefits work and explore what it takes to qualify, how benefits are calculated, and what different types of benefits exist.

terms to know

Great Depression

A severe economic crisis from 1929 to the late 1930s, marked by high unemployment, bank failures, and widespread poverty. It led to the creation of Social Security in 1935.

Federal Insurance Contributions Act (FICA)

A U.S. payroll tax that funds Social Security and Medicare, deducted from employees’ wages and matched by employers.

Social Security Administration (SSA)

The government agency that manages Social Security benefits, including retirement, disability, and survivor payments.

Disability Benefits (SSDI)

Monthly payments for people who can’t work due to a serious long-term disability, based on their past work history and earnings.

Survivor Benefits

Financial support for spouses, children, or other dependents of a worker who has passed away.

Early Benefits

Social Security retirement payments that start before full retirement age (as early as 62) but at a reduced amount compared to waiting until full retirement age.

2. Social Security Benefits

Now that we know how Social Security is funded, let’s talk about how people actually receive benefits. Social Security isn’t just a savings account where you get back exactly what you put in. Instead, it’s a program designed to provide financial support when people reach retirement age, become disabled, or lose a spouse or parent who was a worker.

Social Security benefits work by calculating how much a person has earned over their working years and how much they have paid into the system. The more someone works and earns, the more they may receive in benefits later. However, there are rules about who qualifies, when benefits start, and how much money people can get.

Who Qualifies for Social Security Benefits?

To receive Social Security benefits, a person must have worked and paid into the system for a certain number of years. Social Security keeps track of this through something called work credits.

Work credits: Every year a person works and earns money, they can earn up to four work credits (one per quarter, or every 3 months).

To qualify for retirement benefits, you generally need 40 credits—which is about 10 years of working.

For disability benefits, fewer credits may be required, depending on age.

EXAMPLE

Let’s say Alexia starts working at age 22 and works steadily for 10 years, earning enough each year to get four credits. By age 32, Alexia will have 40 credits and will qualify for Social Security retirement benefits later in life, even if they stop working before retirement age.

Social Security benefits aren’t just for retirees! There are three main types of benefits people can receive:

1. Retirement Benefits (The Most Common)

Most people think of Social Security as the money they’ll receive when they retire. A person can start collecting as early as age 62, but the amount they receive depends on when they start:

Early retirement (age 62–66): People can start receiving benefits at 62, but they get a reduced amount (about 70%–75% of full benefits).

Full retirement age (67 for most people today): If someone waits until their full retirement age, they get 100% of their calculated benefit.

Delaying retirement (up to age 70): If someone waits past full retirement age to collect benefits, they earn extra money—about an 8% increase for every year they delay, up to age 70.

EXAMPLE

Mia decides to retire early at 62. If she is supposed to receive $1,500 per month at 67, she’ll only get about $1,050 per month instead.

Jake waits until 70 to retire. His original benefit was $1,500 at 67, but because he waited, he’ll now get about $1,860 per month.

try it

Maria is 61 years old and thinking about when to take Social Security. Her full retirement age (FRA) is 67, and she qualifies for a $2,000 monthly benefit if she waits until then. However, she could start collecting early benefits at 62, but it would reduce her payments by 30% for life.

Question 1: How much will Maria receive per month if she takes Social Security at 62 instead of waiting until 67?

Answer to Question 1:

Maria’s full benefit at 67 will be $2,000 per month.

If she takes benefits at 62, her monthly benefit will be reduced by 30%:

So, if Maria takes Social Security at 62, she will receive $1,400 per month instead of $2,000.

Question 2: What are the pros and cons of taking it early versus waiting?

Answer to Question 2:

Taking benefits early (at 62):

Maria will get the money sooner.

This will help if she needs income right away.

She gets a permanently lower benefit ($1,400 vs. $2,000).

If she lives a long time, she might lose out on more money overall.

Waiting until 67 for full benefits:

She will get her full benefit of $2,000 per month.

If she lives a long time, she’ll collect more money over her lifetime.

She will have to wait five more years before receiving any payments.

hint

The longer you wait (up to age 70), the more money you receive each month.

2. Disability Benefits (SSDI: Social Security Disability Insurance)

If someone becomes disabled and can’t work for a year or longer, they may qualify for Social Security disability benefits. The amount they receive is based on their past earnings.

EXAMPLE

Sarah is a 35-year-old construction worker who suffers a severe injury and can’t work anymore. She has worked for 12 years and has enough work credits. She applies for SSDI benefits and, once approved, starts receiving a monthly payment to help cover expenses.

Key takeaway: SSDI is like a safety net if someone can no longer work due to a serious disability.

3. Survivor Benefits (For Spouses, Children, or Other Dependents)

When a person who was paying into Social Security passes away, their spouse, children, or sometimes even elderly parents may qualify for benefits to help financially.

EXAMPLE

Mark, a father of two, worked for 20 years but passes away unexpectedly at 45. His children (under age 18) and his spouse may qualify for monthly survivor benefits to help support them financially.

Lisa, who was married to Mark for 15 years, can receive widow’s benefits when she reaches retirement age.

Key takeaway: Survivor benefits help families who have lost a loved one who was a worker contributing to Social Security.

learn more

If you’ve ever heard someone say, “Social Security is running out of money”, you might wonder, “Is that true?” Will Social Security still exist when today’s young workers retire? Let’s break down what’s really happening.

The Reality: Social Security Isn’t Going Away, But It May Change

Here’s the key fact: Social Security is not “running out of money,” but it is facing financial challenges.

Right now, more money is being paid out in benefits than is being collected in taxes.

This is happening because baby boomers (a large generation) are retiring in huge numbers, but fewer younger workers are paying into the system.

If nothing changes, the Social Security Trust Fund (which holds extra money to cover benefits) is expected to be depleted by the mid-2030s.

BUT—even if the trust fund runs out, Social Security will still collect payroll taxes from workers and employers. This means it won’t disappear—but benefits could be reduced if no changes are made.

What Could Happen to Fix Social Security?

The government has options to keep Social Security strong for future generations. These are some possible solutions:

Raising the payroll tax rate: Right now, workers and employers each pay 6.2% of wages into Social Security. A small increase (like 7% each) could help stabilize the system.

Raising the full retirement age: Currently, full benefits start at 67 for most people. Some experts suggest increasing it to 68 or 70, since people are living longer.

Changing benefit formulas: Social Security could adjust how benefits are calculated so that higher-income workers receive slightly smaller benefits, making the system more sustainable.

Lifting the payroll tax cap: Right now, only income up to $176,100 (as of 2025; this number adjusts every year) is taxed for Social Security. If that cap is removed or raised, higher earners would contribute more.

Investing Social Security funds: Some policymakers suggest allowing a portion of Social Security money to be invested in stocks or other assets to help grow funds over time.

While Social Security isn’t “going broke,” it does need adjustments to remain strong. The government is likely to make changes over the next decade to ensure that future generations can count on Social Security.

So, will Social Security be there when you retire? Yes! But to have a comfortable retirement, you’ll also want to build your own savings through investments, retirement accounts, and smart financial planning.

The amount someone receives in Social Security benefits depends on the following:

How much they earned over their lifetime: Higher lifetime earnings = higher benefits.

When they start collecting benefits: Early retirement means smaller checks; delaying benefits increases them.

What type of benefit they qualify for: Disability and survivor benefits vary based on different factors.

EXAMPLE

Emma worked as a teacher for 35 years and had an average salary of $60,000 per year. She will receive around $2,000 per month in retirement benefits.

Ryan only worked part-time for 15 years, earning about $25,000 per year. His benefit may be closer to $1,000 per month.

hint

The more you earn over your lifetime, the higher your Social Security benefit will be.

big idea

Even though Social Security benefits may feel far away, it’s important to understand how they work now so you can make smart financial decisions in the future.

Every time you work and pay Social Security taxes, you’re building your eligibility for benefits later in life.

The more you earn and the longer you work, the higher your benefits will be.

Social Security isn’t just for retirees—it helps disabled workers and families who have lost loved ones.

Understanding Social Security now helps you plan for the future—whether that’s making sure you’re saving enough for retirement, knowing your options in case of an emergency, or helping family members who may already be receiving benefits.

terms to know

Work Credits

Units earned by working and paying Social Security taxes; you need 40 credits (about 10 years of work) to qualify for retirement benefits.

Full Retirement Age

The age when you can collect full Social Security retirement benefits, currently 67 for most people born after 1960.

summary

In this lesson, you learned how Social Security works, including who has access to Social Security benefits.

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.

Terms to Know

Disability Benefits (SSDI)

Monthly payments for people who can’t work due to a serious long-term disability, based on their past work history and earnings.

Early Benefits

Social Security retirement payments that start before full retirement age (as early as 62) but at a reduced amount compared to waiting until full retirement age.

Federal Insurance Contributions Act (FICA)

A U.S. payroll tax that funds Social Security and Medicare, deducted from employees’ wages and matched by employers.

Full Retirement Age

The age when you can collect full Social Security retirement benefits, currently 67 for most people born after 1960.

Great Depression

A severe economic crisis from 1929 to the late 1930s, marked by high unemployment, bank failures, and widespread poverty. It led to the creation of Social Security in 1935.

Social Security Administration (SSA)

The government agency that manages Social Security benefits, including retirement, disability, and survivor payments.

Survivor Benefits

Financial support for spouses, children, or other dependents of a worker who has passed away.

Work Credits

Units earned by working and paying Social Security taxes; you need 40 credits (about 10 years of work) to qualify for retirement benefits.