Every taxpayer must sign their own return. A joint return must be signed by both the taxpayer and the spouse. The date of signing, occupations, daytime telephone number, and email should be entered in the appropriate spaces.

If a spouse died before the end of the year and the surviving spouse files a joint return, the If a spouse died before the end of the year and the surviving spouse files a joint return, the executor or administrator must sign the return for the deceased spouse. If no one has been appointed executor or administrator, the surviving spouse can sign the joint return and enter “Filing as surviving spouse” in the signature area.

Paid tax return preparers must sign every return they are paid to prepare. The date the return was prepared should also be entered. The preparer must enter their preparer tax identification number (PTIN) in the space provided. A PTIN is required annually for anyone who prepares or assists in preparing federal tax returns for compensation.

In addition, the tax preparer must be sure their employer’s company name, address, ZIP code, phone number, and employer identification number are entered in the signature section.

A self-employed preparer should enter their own name, PTIN, address, ZIP code, and phone number where they can be reached all year. They should also check the Self-employed box.

The IRS may provide an Identity Protection Personal Identification Number (IP PIN) to taxpayers who are victims of identity theft. The Identity Protection PIN is a six-digit number that is attached to the taxpayer’s tax return account. It prevents anyone from filing a return only using the social security number, date of birth, and address. The PIN must be provided at the time the tax return is filed. If it is not provided, the return will not be processed by the IRS.

An Identity Protection PIN is only valid for one calendar year and a new PIN must be obtained for each new tax year.

Starting in 2021, taxpayers may request an Identity Protection PIN even if not victims of identity theft. More information can be obtained from the IRS website.

The majority of tax returns are filed electronically. Therefore, no paperwork is physically sent to the IRS. The taxpayer and paid tax preparer will still need to sign the tax return. This is accomplished using a personal identification number (PIN). This is different from the Identity Protection PIN discussed above. The PIN is a combination of any random five digits selected by the taxpayer(s) and a combination of five digits selected by the paid tax preparer. If the PIN is used, nothing has to be physically signed and mailed to the IRS. Another way to think of the PIN is that entering those five digits is in fact the taxpayer digitally “signing” the return. When the paid tax preparer enters their own PIN, the act of entering those numbers on the keyboard is in fact them digitally signing the return as the paid preparer.

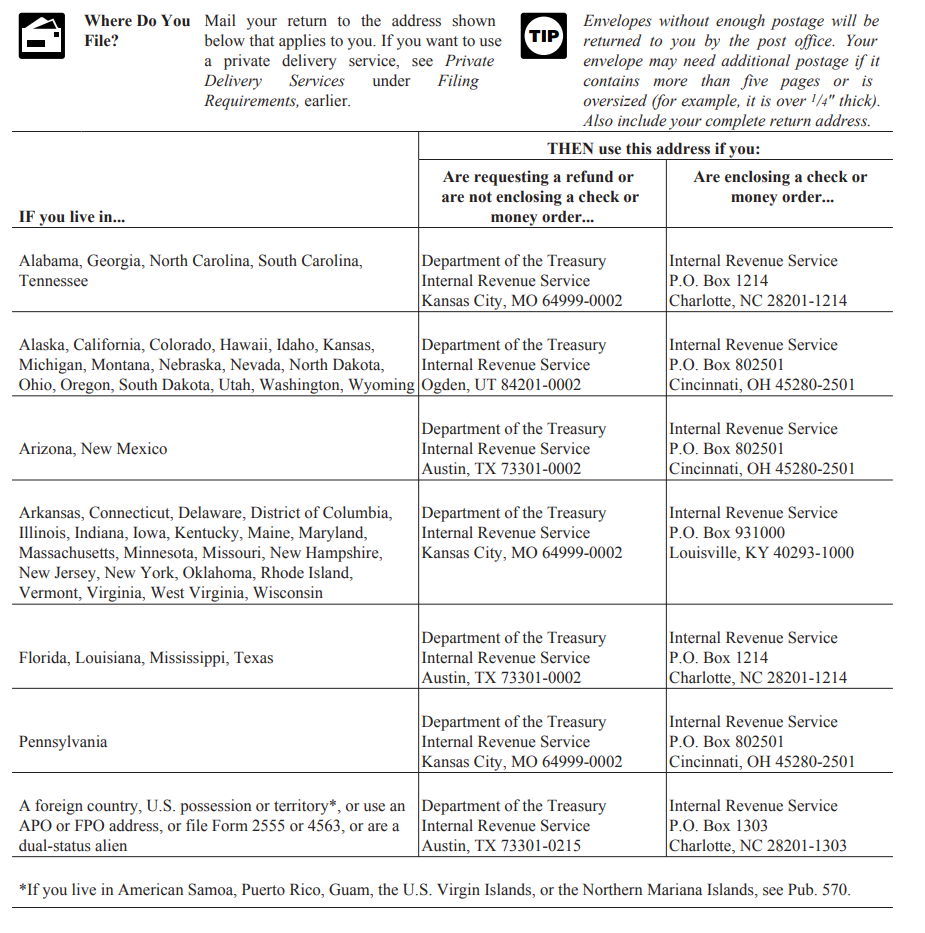

If the taxpayer does not electronically file their return, the other option is to physically mail in their tax return. The Form 1040 would need signatures in all the appropriate areas of the form before mailing.

Depending on where the taxpayer lives and whether they are receiving a refund or enclosing a payment, the IRS provides specific addresses for the return to be mailed.

These addresses have been known to change year over year, so it is important to look up the address each year in the Form 1040 instructions.

After filing a tax return, the taxpayer ends up with either a refund or a balance due. Certain elections can be made directly on Form 1040, or with attached forms, to direct the IRS on how to proceed with the tax refund or balance due.

There are a few options on how a tax refund can be processed.

The refund can be:

There are a few payment options offered by the IRS.

Payments can be made:

There are also additional options if the taxpayer cannot pay the entire balance due.

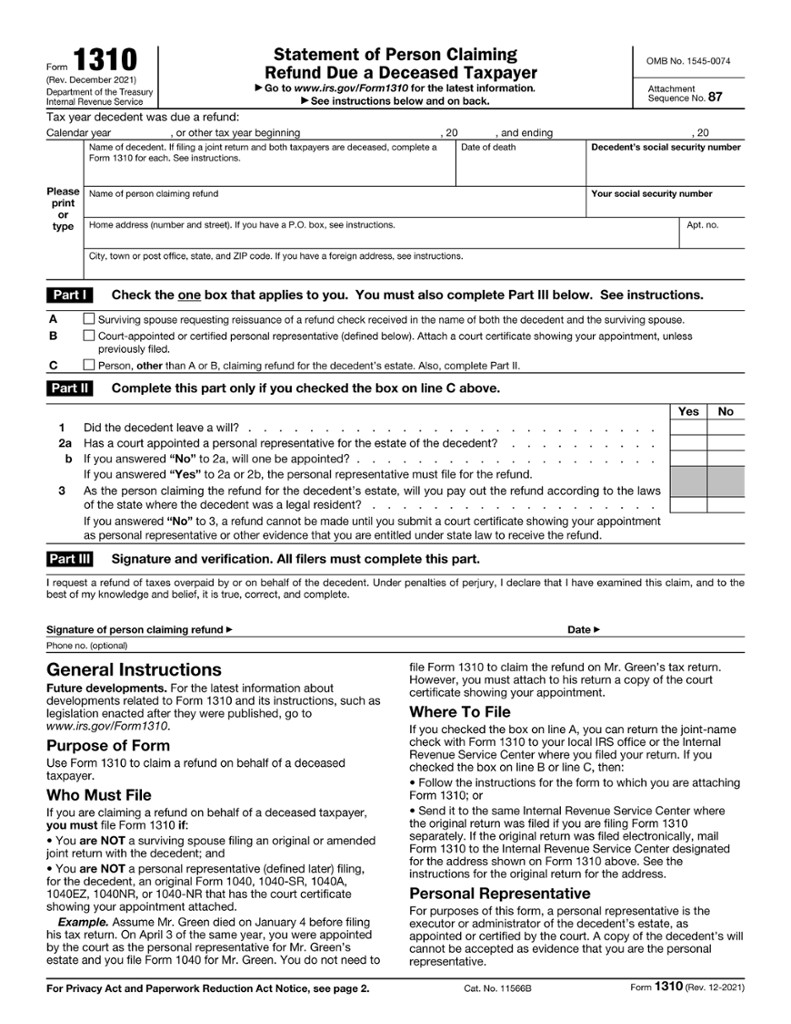

Form 1310, Statement of Person Claiming Refund Due a Deceased Taxpayer, is used to claim a refund on behalf of a deceased taxpayer.

An individual claiming a refund on behalf of a deceased taxpayer must file Form 1310 if:

EXAMPLE

Norma’s father died on June 5th. Norma is his sole survivor. Norma’s father did not have a will and the court did not appoint a personal representative for his estate. Norma’s father is entitled to a $400 refund. To get the refund, Norma must complete and attach Form 1310 to her father’s final return. She should check the box on Form 1310, line C; answer all the questions in Part II; and sign her name in Part III. Norma must also keep a copy of the death certificate or other proof of death for her records.For purposes of Form 1310, a personal representative is the executor or administrator of the decedent’s estate, as appointed or certified by the court. A copy of the decedent’s will cannot be accepted as evidence that an individual is the personal representative.

EXAMPLE

Assume Mr. Brown died on January 10 before filing his tax return. On April 8 of the same year, Sam Smith was appointed by the court as the personal representative for Mr. Brown’s estate and Sam files Form 1040 for Mr. Brown. Sam does not need to file Form 1310 to claim the refund on Mr. Brown’s tax return.