In this lesson we will examine ways management sets product prices, using differential analysis techniques. One of the most important calculations management does is setting prices of products. There are several ways to set prices, depending on the philosophy of the business. In this lesson we will discuss several of the specific ways management sets pricing. Specifically, we will discuss:

1. Cost-Plus Pricing Method

Cost-plus pricing is a pricing strategy that determines a product’s selling price by adding the product’s unit cost to a markup percentage. Markup is the amount added to the cost of an item to cover overhead and achieve a desired profit. Desired profit is an amount, determined by management, that will earn the company an acceptable return on their investment. Cost-plus is one of the easiest and most common pricing practices. Retail outlets like clothing, department, and grocery stores often use cost-plus pricing to set the prices of their merchandise.

-

There is not one correct pricing methodology. Many factors may play into how prices are set. Businesses must consider factors such as their mission statement, revenue goals, return on investment, marketing objectives, target audience, branding, and specific product attributes. Pricing is a strategic decision, so it must be carefully considered.

Cost-plus pricing is a convenient way for a retail outlet to determine the unit cost of a product since goods are ordered on a per-unit basis. These stores then add a markup percentage to the cost of the goods, which serves as the price. Depending on the type of retail outlet, this can be a low markup percentage or a high one.

A markup percentage depends on the product and the retail outlet. High-end retail outlets like jewelry stores mark up their products anywhere between 250% to 300%. In contrast, dollar stores have an average markup of 15% to 30%, depending on the item.

-

EXAMPLE

Some products have high markups while others do not. For example, movie theater popcorn has an average 1,275% markup and bottled water has a 4,000% markup, when sold separately. Conversely, smartphones and new cars only have a 9% markup.

In theory, stores can mark up their goods as high (or low) as they would like. Practically, their markups must be in line with their competitors, unless they offer some other benefit their competitors do not. Additionally, not all products are marked up at the same percentage. Retail outlets determine which types of products have higher markups and which have lower markups. These are usually determined by competitor pricing, demand, and supply of the product.

-

- Selling Price Formula in Cost-Plus Pricing

- Selling Price = Cost per unit + Markup

-

- Multiply the cost per unit by the markup percentage to determine the amount of markup.

- Add the dollar amount of markup to the cost per unit to determine the selling price.

-

EXAMPLE

Big Box Store purchases 32 oz. bottles of ketchup for $3.00 per bottle. Their markup on condiments is 40%. Using cost-plus pricing, this means that the markup per unit is $3.00 x 40% or $1.20. The sale price of the ketchup bottles therefore are $4.20, or $3.00 cost per unit + $1.20 markup.

-

Bargain Store purchases bags of potato chips from the manufacturer for $1.50. Their markup on potato chips is 30%.

-

- Cost-Plus Pricing

- A pricing strategy that determines a product’s selling price by adding the product’s unit cost to a markup percentage.

- Desired Profit

- An amount, determined by management, that will earn the company an acceptable return on their investment.

- Markup

- The amount added to the cost of an item to cover overhead and achieve a desired profit.

2. Product Cost Method

The product cost method of pricing involves considering all the costs that feed into manufacturing a product, called product costs, and then adding a markup to those product costs to determine the price. Product costs are manufacturing costs which include direct materials, direct labor, and factory overhead. Markup, using the product cost method, is determined by adding administrative expenses, selling expenses, and a desired profit or return on investment.

Using tools such as a contribution margin income statement, management determines the variable and fixed costs they incur during the manufacturing process. That is why it is so important to accurately identify and track costs throughout the manufacturing process. Without accurate accounting, companies may forego profit.

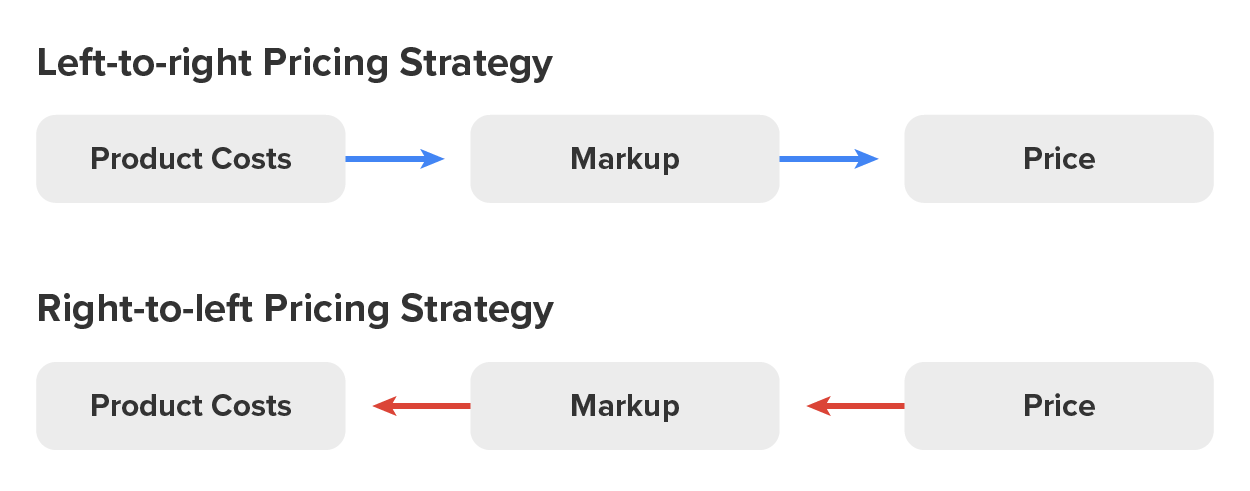

Overall, there are two main philosophies in setting prices. The first philosophy is a left-to-right pricing philosophy which begins by examining all costs involved, and then adding a desired profit to determine the price. Examples of left-to-right pricing strategies are cost-plus and product-cost pricing. The second philosophy, right-to-left pricing, starts with determining a price (based on market conditions), and then subtracting from that price a desired profit to calculate what can be spent to manufacture the product. Whichever philosophy is used, pricing a product is a key business decision and must be done with care and precision. An example of a right-to-left strategy is target costing.

Determining product pricing using the product cost method can be achieved using the following steps:

-

- Determine the total product costs.

- Compute the product cost per unit.

- Calculate the desired profit.

- Determine the markup percentage.

- Calculate the markup per unit.

- Determining the selling price.

As we go through the individual steps, we will now determine the selling price per unit, using the product cost method, for the Seattle Salad Dressing Company, which produces bottles of salad dressing. The cash budget, selling and administrative expense budget, and balance sheet will provide us with the information needed to complete this work.

2a. Determine the total product costs.

The total product cost is determined by using information collected from the cash budget. We sum the direct materials, direct labor, and manufacturing overhead amounts to find total product costs. We will use selling and administrative expenses in a later calculation.

-

- Total Product Cost Formula:

- Total Product Cost = Total Direct Materials + Total Direct Labor + Total Manufacturing Overhead

-

Direct materials, direct labor, manufacturing overhead, and selling and administrative costs can be found in the cash budget.

-

EXAMPLE

For Seattle Salad Dressing Company, the figures found in the cash budget are as follows:

- Direct Materials $280,000

Direct labor $102,000

Manufacturing overhead $ 54,000

Total Product Cost = Total Direct Materials + Total Direct Labor + Total Manufacturing Overhead

Total Product Cost = $280,000 + $102,000 + $54,000

Total Product Cost = $436,000

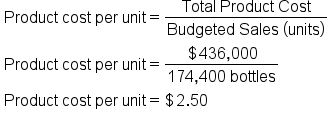

2b. Compute the product cost per unit.

To find the product cost per unit, divide the total product cost by the budgeted units of production. The budgeted units of production can be found in the selling and administrative expense budget.

-

- Product Cost Per Unit Formula:

-

EXAMPLE

For Seattle Salad Dressing Company, the figure found in the selling and administrative expense budget is as follows:

- budgeted sales (units) 174,400 bottles

-

Budgeted sales (units) can be found on the selling and administrative expense budget.

2c. Calculate the desired profit.

Desired profit is the goal a company aims for when selling a product. Often, this amount is based on a return on assets. In order to calculate the desired profit, one needs to know what the acceptable desired return (return on investment) a company is aspiring to. This amount is a percentage set by the company that ensures their investment in the product pays off. To determine the desired profit, we need to know the desired return and the total assets, which come from the budgeted balance sheet.

-

- Desired Profit Formula:

- Desired Profit = Desired Return on Investment Percentage x Total Assets

-

EXAMPLE

For Seattle Salad Dressing Company, the figure found in the budgeted balance sheet is as follows:

- Total Assets $800,000

The company desires a 20% desired return for its products.

Desired Profit = Desired Return x Total Assets

Desired Profit = 20% x $800,000

Desired Profit = $160,000

-

The desired rate of return on investment (ROI) percentage is a figure that management sets to ensure profits are maximized. Total assets are found in the balance sheet.

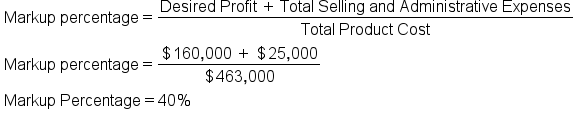

2d. Determine the markup percentage.

Now that we have calculated the desired profit, we can determine the markup percentage we will add to the cost to finalize our selling price. In addition to the desired profit, we will need the total selling and administrative expenses, which come from the cash budget, and the total product cost which we determined in step one of this process.

-

- Markup Percentage Formula:

-

EXAMPLE

For Seattle Salad Dressing Company, the figure found in the cash budget is as follows:

- Total Selling and Administrative Expenses $25,000

We also know:

- Desired Profit $160,000

Total Product Cost $463,000

2e. Calculate the markup per unit.

The amount of markup per unit will be determined by multiplying the product cost per unit, which we calculated in step two, by the markup percentage. This sum will yield the dollar amount of markup we will charge for each of our products.

-

- Markup Per Unit Formula:

- Markup per unit = Markup Percentage x Product Cost per unit

-

EXAMPLE

For Seattle Salad Dressing Company, amounts determined as follow:

- Markup Percentage 40%

Product Cost Per Unit $2.50

Markup per unit = Markup Percentage x Product Cost per unit

Markup per unit = 40% x $2.50

Markup per unit = $1.00

2f. Determine the selling price.

Finally, we can now determine the selling price of our product. The selling price is the sum of the product cost per unit plus the markup per unit.

-

- Selling Price Per Unit Formula:

- Selling Price per unit = Product Cost per unit + Markup per unit

-

EXAMPLE

For Seattle Salad Dressing Company, amounts determined as follows:

- Markup Per Unit $1.00

Product Cost Per Unit $2.50

Selling Price per unit = Product Cost per unit + Markup per unit

Selling Price per unit = $2.50 + $1.00

Selling Price per unit = $3.50

-

The product cost is what we calculated in step two of this process and the markup per unit was calculated in step 5.

-

Now, you will attempt to determine a selling price using the product cost method.

Minnesota Macaroni and Cheese company is attempting to determine what price to charge for boxes of its products. They have collected the following data which will be used to calculate the selling price:

|

|

Amount

|

Statement of Origination

|

|

Direct Materials

|

$ 225,000

|

Cash Budget

|

|

Direct Labor

|

$ 80,000

|

Cash Budget

|

|

Manufacturing Overhead

|

$ 37,000

|

Cash Budget

|

|

Selling and Administrative

|

$ 22,600

|

Cash Budget

|

|

Budgeted Sales (units)

|

180,000

|

Selling and Administrative Budget

|

|

Total Assets

|

$ 400,000

|

Budgeted Balance Sheet

|

|

Desired Return

|

20%

|

Managerial Decision

|

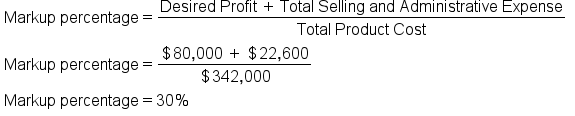

What is the total product cost?Total Product Cost = Total Direct Materials + Total Direct Labor + Total Manufacturing Overhead

Total Product Cost = $225,000+ $80,000 + $37,000

Total Product Cost = $342,000

What is the product cost per unit?Product cost per unit = Total Product Cost ÷ Budgeted Sales (units)

Product cost per unit = $342,000 ÷ 180,000 bottles

Product cost per unit = $1.90

What is the markup per unit?Markup per unit = Markup Percentage x Product Cost per unit

Markup per unit = 30% x $1.90

Markup per unit = $ 0.57

What is the selling price?Selling Price per unit = Product Cost per unit + Markup per unit

Selling Price per unit = $1.90 + $0.57

Selling Price per unit = $2.47

-

- Product Cost Method

- A pricing methodology strategy that adds all product costs that feed into manufacturing a product then adds a markup to determine the price.

- Product Costs

- Manufacturing costs that include direct materials, direct labor and factory overhead.

- Left-to right Pricing

- A pricing strategy where costs that go into a product are first considered, then prices are set after adding markup.

- Right-to-left Pricing

- A pricing strategy where the price of the product is the driving factor, then target profit is subtracted, which leaves the cost the business can incur in making the product.

3. Target Costing Method

Target costing is a methodology of pricing new products, before they are manufactured, by subtracting the desired profit from an expected selling price. The expected selling price is a benchmark price, usually determined by market price or product demand. As mentioned earlier, desired profit is an amount, determined by management, that will earn the company an acceptable return on their investment. In target costing we work backward from the price we wish to charge to determine how much total cost could be invested into a product, in order to sell it for the predetermined price.

-

Local Bicycle is looking to create a new mountain bike that competes with Big Bike Incorporated. How might Local Bicycle develop a competitive pricing strategy?

Often, businesses must charge a lower price to better compete with market prices. In this case, they must find a way to reduce their costs. Some ways to reduce costs are:

- Using different raw materials

- Reducing direct labor costs

- Using lean manufacturing techniques (eliminating waste)

- Simplifying designs

By examining cost structures up front, a business can better predict what its profits will be and work to control its costs more proactively.

-

- Desired Profit Formula:

- Desired Profit (in dollars) = Expected Selling Price x Desired Profit Percentage

-

- Target Costing Formula:

- Target Cost = Expected Selling Price - Desired Profit (in dollars)

-

- Determine the amount of desired profit (in dollars)

- Determine Target Cost

-

EXAMPLE

Local Bicycle LLC. is investigating if it can compete with Big Bike Company in producing and selling a mountain bike. Big Bike’s price for the mountain bike is $200. Local Bike believes it can be competitive with a selling price of $210. The owner of Local Bicycle desires a profit of 25% on the mountain bike, so they use target costing to identify the costs for producing the new mountain bike that would allow for a 25% profit with a selling price of $210.

First, the owner determines the amount of desired profit in dollars by multiplying the expected selling price of $210 by the desired profit percentage of 25%, which yields a desired profit of $52.50. Then they subtract the desired profit from the expected selling price of $210, which yields the target cost of $157.50. This tells the owner that in order to price the bike at $210 and make 25% profit, they will have to ensure that total costs per bike are not above $157.50.

-

Now, you will try to determine the target cost on your own using Felix’s Flip Flop Inc. Felix’s Flip Flop Inc. is a small manufacturer of flip-flops. They are thinking about breaking into the clog market. Felix has done some research and determined the following:

Average Market Price for Clogs: $42.00

Felix’s Desired Profit: 35%

Felix’s Estimated Selling Price: $40.00

-

- Target Costing

- A methodology of pricing products that subtracts a desired profit from an expected selling price to determine how much cost a company can invest in a product and still earn a desired profit.

- Expected Selling Price

- A price set by management for a product it wants to produce; it is usually determined by market price or product demand.

In this lesson, we learned about the application of differential analysis when setting prices for products. There are multiple ways that prices can be set, including the cost plus method, the product cost method, and the target costing method. Overall, there are two main philosophies in setting prices. The first philosophy is a left-to-right pricing philosophy which begins by examining all costs involved, then adding a desired profit to determine the price. The second philosophy, right-to-left pricing, starts with determining a price (based on market conditions), then subtracting from that price a desired profit to calculate what can be spent to manufacture the product. Managers will choose the method that best fits the company’s philosophy.

Cost plus pricing involves calculating the selling price by adding the product’s unit cost to a markup percentage where the markup is the amount added to the cost of an item to pay overhead and achieve a desired profit. The amount of desired profit is determined by management based on what they want the company to earn in order to have an acceptable return on their investment. Cost plus pricing is commonly used to set prices in retail outlets such as clothing, department, and grocery stores.

We also discussed the product cost method for setting prices. The product cost method involves considering the product costs, then adding a markup to the product costs to arrive at the selling price. Product costs consist of manufacturing costs that include direct materials, direct labor, and factory overhead. In order to find the markup when the product cost method is used, we add administrative expenses, selling expenses, and a desired profit or return on investment.

Finally, we learned about the target costing method where the pricing of new products is done before the product is manufactured by subtracting the desired profit from an expected selling price. The expected selling price is a benchmark price, usually determined by market price or product demand. By examining cost structures up front, a business can better predict what its profits will be and work to control its costs more proactively.