In this lesson, you will learn why financial goals matter and how to make your goals SMART. You’ll also learn how to track progress toward your goals. Specifically, this lesson will cover the following:

1. Why Financial Goals Matter

Have you ever felt like your money just disappears every month, leaving you wondering where it all went? Or maybe you have big dreams, like buying a house or taking a dream vacation, but you don’t know how to make them a reality. This is where financial goals come in. Think of them as your personal GPS, guiding you step by step toward the life you want.

-

Financial goals aren’t just for the wealthy or the financially savvy—they’re for everyone. Whether you’re earning minimum wage or six figures, having goals helps you give your money a purpose.

Imagine you’re planning a road trip. Would you just get in the car and start driving, hoping you’ll end up somewhere amazing? Probably not. You’d pick a destination, map out the route, and plan your stops along the way. Setting financial goals works the same way. Without them, your money has no direction, and you might find yourself spinning your wheels without getting anywhere.

Why set financial goals?

- Clarity: Goals help you figure out what you want your money to do for you.

- Motivation: They give you something exciting to work toward.

- Accountability: Goals make it easier to evaluate whether your spending aligns with what matters most.

-

EXAMPLE

You’re earning $3,000 a month, but it feels like your paycheck evaporates before you can do anything meaningful with it. With goals, you can say, “I’m putting $500 into savings, $200 toward debt, and $300 for fun,” and suddenly, you’re in the driver’s seat.

Now that we know why goals matter, let’s figure out what you really want your money to do for you.

-

- Financial Goals

- Specific targets you set for managing and saving your money.

1a. Identifying Your Goals

Close your eyes for a moment and imagine your ideal life. What does it look like? Are you debt-free? Do you own a cozy home? Are you traveling the world? Understanding what you truly want is the first step in setting meaningful financial goals.

-

Ask yourself these questions:

- What would financial success look like to me?

- If money weren’t an issue, how would I live my life?

- What’s one thing I wish I could afford right now?

Your answers to these questions can help you uncover the financial goals that really matter. Maybe you want the peace of mind that comes with an emergency fund, or perhaps you dream of starting your own business. Whatever it is, write it down. Seeing your goals on paper makes them feel real.

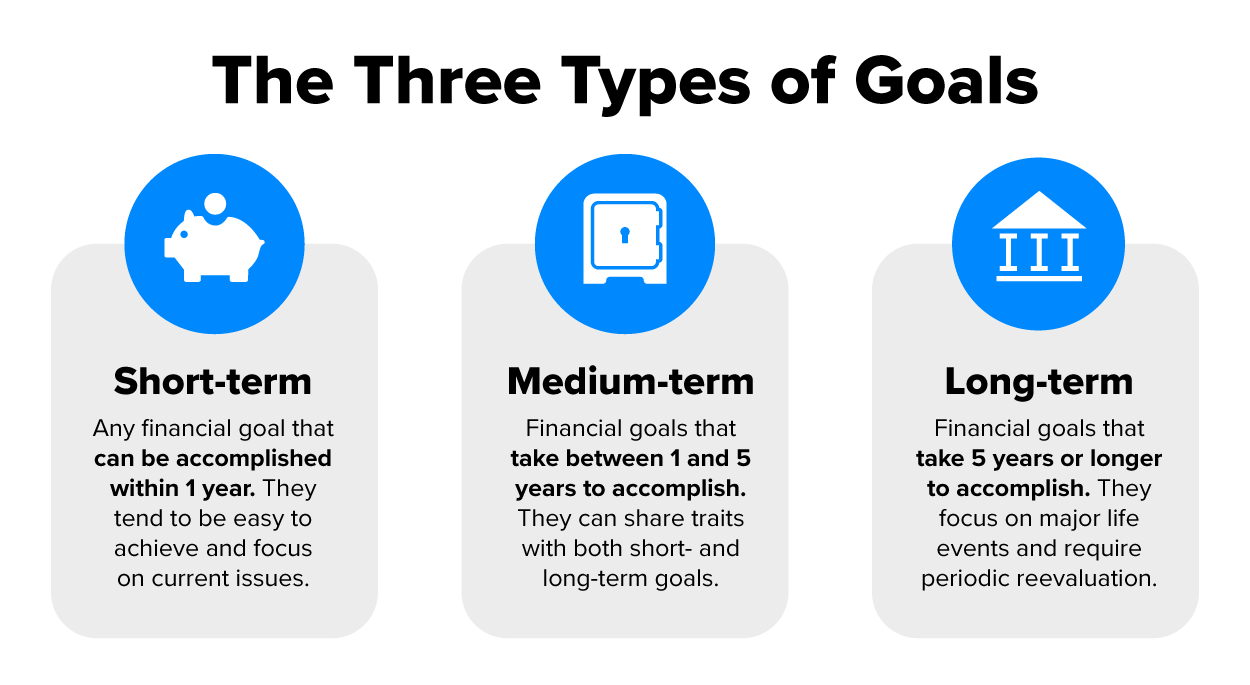

The first place to start is by categorizing your goals. Financial goals typically fall into the following categories:

-

Short-term goals (0–1 year): Emergency funds, paying off small debts, or saving for a vacation

-

Medium-term goals (1–5 years): Saving for a down payment on a house, paying off larger debts, or starting a business

-

Long-term goals (5+ years): Retirement, funding your kids’ education, or achieving financial independence

-

EXAMPLE

- Short-term: Save $1,000 for an emergency fund in 6 months

- Medium-term: Pay off $10,000 in credit card debt in 3 years

- Long-term: Save $500,000 for retirement by the age of 65

Now that you’ve identified your goals, let’s make them SMART.

-

- Short-Term Goals

- Financial objectives you aim to achieve within a year.

- Medium-Term Goals

- Goals you plan to accomplish in 1–5 years.

- Long-Term Goals

- Big financial plans that take 5+ years to achieve.

1b. SMART Goals

Ever set a vague goal like, “I want to save more money,” and then forgot all about it? That’s because vague goals don’t give you a clear path to follow. The SMART Goals framework helps you turn fuzzy ideas into crystal-clear plans that you can actually achieve.

Goals should be SMART:

- Specific: What exactly do you want to achieve?

- Measurable: How will you track progress?

- Achievable: Is this goal realistic?

- Relevant: Does it align with your values and priorities?

- Time-bound: What’s the deadline?

Let’s break down each component:

- Be as detailed as possible. Instead of saying, “I want to save money,” specify how much, for what purpose, and where the money will go. For example, “I want to save $5,000 for a down payment on a car.” Specific goals give you clarity and a clear target to aim for.

- Numbers are your best friend here. Ask yourself, “How will I know when I’ve achieved this goal?” For example, saving $250 a month toward your $5,000 car fund makes the goal measurable and allows you to track your progress easily.

- This is where reality comes into play. If you’re earning $2,000 a month and trying to save $1,500 of this, you might be setting yourself up for failure. Break your goal into something that fits within your financial limits. Even if progress feels slow, you’re still moving forward.

- Your goals should align with your bigger life priorities. Saving for a car might not make sense if your primary focus is paying off high-interest debt. Relevance ensures your goals fit your current situation and future aspirations.

- Deadlines create urgency and help you stay focused. Instead of saying, “I’ll save for a car,” set a specific time frame like, “I’ll save $5,000 in 24 months by saving $208 each month.”

-

EXAMPLE

Instead of saying, “I want to save money,” use SMART criteria:

- Specific: Save $3,000 for a vacation.

- Measurable: Track savings each month.

- Achievable: Save $250 per month.

- Relevant: Taking a vacation is a priority.

- Time-bound: Reach the goal in 12 months.

SMART goals break big dreams into clear, manageable steps. They eliminate guesswork, helping you stay focused and motivated as you work toward your goals.

Great—now that your goals are SMART, let’s break them into smaller, doable steps.

-

- SMART Goals

- Clear and structured objectives that are specific, measurable, achievable, relevant, and time-bound.

1c. Breaking Down Big Goals Into Actionable Steps

Big goals can feel like staring up at a massive mountain. But what if you broke that climb into small, manageable steps? Suddenly, the mountain doesn’t seem so intimidating. Let’s break this process down further with relatable examples.

Start with the end in mind: Think about the ultimate goal and then work backward. This makes it easier to see the steps you’ll need to take along the way. For instance, if you’re saving $1,000 for an emergency fund, focus on the first $100 rather than the whole amount.

-

EXAMPLE

Saving $1,000 for an emergency fund over 6 months:

- Set a Monthly Target: Break the total goal into smaller chunks. $1,000 ÷ 6 months = $167/month. Doesn’t $167 sound more doable than $1,000 all at once?

- Cut Expenses Strategically: Look at your spending habits. Could you pack lunch 3 days a week instead of eating out? Could you cancel a subscription you rarely use? Even small changes, like brewing your own coffee, can add up.

- Automate Savings: Set up an automatic transfer of $167 to a separate savings account each month. Out of sight, out of mind.

- Celebrate Progress: Every time you save $100, give yourself a small, affordable reward like a coffee or movie night. Small wins keep you motivated.

When you focus on small, manageable steps, big goals feel less overwhelming. Each completed step gives you a sense of accomplishment, which builds momentum to keep going.

Now that you’ve broken down your goals into actionable steps, it’s time to discuss how you track progress toward your goals.

2. Tracking Progress Toward Your Goals

Have you ever started a project with tons of excitement, only to lose steam halfway through? Staying motivated can be tough, but it’s not impossible. The key is tracking your progress in ways that keep you engaged and inspired.

1. Celebrate Small Wins

Progress doesn’t have to mean completing the entire goal—every step forward counts. Paid off one credit card? Celebrate by doing something you enjoy, like having a low-cost night out or buying a small treat. Saved your first $500 for an emergency fund? Share your success with a friend or family member who will cheer you on. Recognizing and celebrating these milestones keeps the momentum going.

2. Revisit and Adjust Goals

Life changes, and so should your goals. Maybe an unexpected expense means you need to slow down on saving for a vacation, or perhaps a raise at work allows you to save more aggressively. Check in with your goals every 3–6 months to ensure they’re still realistic and aligned with your priorities.

3. Find Accountability

It’s easier to stay on track when someone else is cheering you on. Share your goals with a trusted friend, family member, or even an online community so they can be an accountability partner. You can do the following:

- Create a friendly competition, like who can save the most in a month.

- Check in weekly to discuss progress and challenges.

- Celebrate each other’s wins—big or small.

4. Gamify the Process

Turn tracking your progress into a game. For example:

- Reward yourself for every $100 saved or debt payment made.

- Set a challenge to save an extra $20 each week by cutting back on nonessentials, and see how long you can keep the streak alive.

- Use visual trackers that feel fun and interactive.

Progress breeds motivation. The more you see your hard work paying off, the more you’ll want to stick with it. Tracking gives you tangible proof that your efforts are making a difference, even when the end goal feels far away.

Setting financial goals might feel daunting at first, but it’s one of the most empowering steps you can take toward building the life you want. Start small, be consistent, and celebrate your progress.

-

- Accountability Partner

- Someone who helps you stay focused and committed to your goals by providing support.

In this lesson, you now understand why financial goals matter. You have a process for identifying what your goals are, how to make them SMART Goals, and taking steps to break down big goals into actionable steps. Lastly, you have a plan for tracking progress toward your goals.