In another section, we learned that for tax purposes, the Tax Code requires the cost of an asset be depreciated (deducted) over a period of time if the asset is used for business or is income-producing property. You may recall we mentioned, “unless an exception applies.” Well, here we are at the first exception, AKA, the tax plot twist number one!

Section 179 of the United States Internal Revenue Code allows a taxpayer to elect to deduct the cost of certain types of property as an expense, rather than being “capitalized” and depreciated. Let’s revisit our taxpayer, Sherry.

EXAMPLE

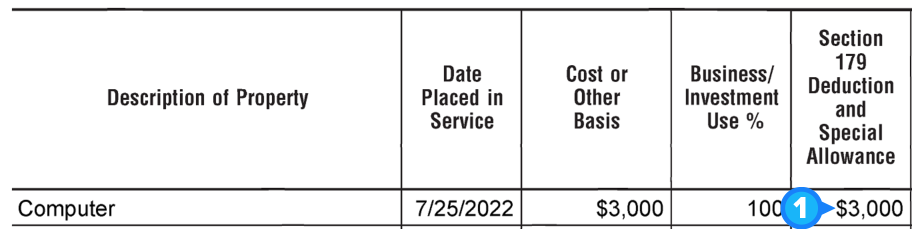

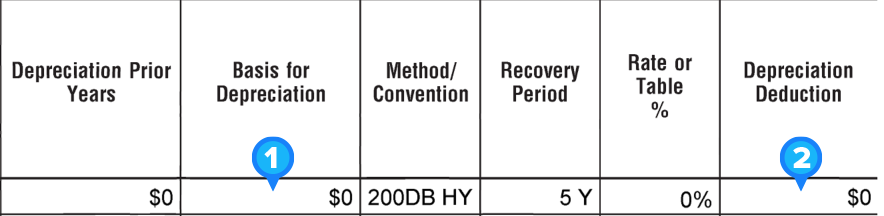

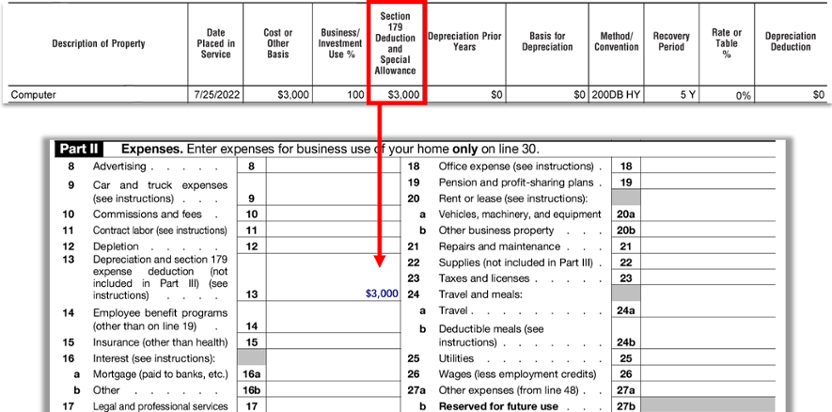

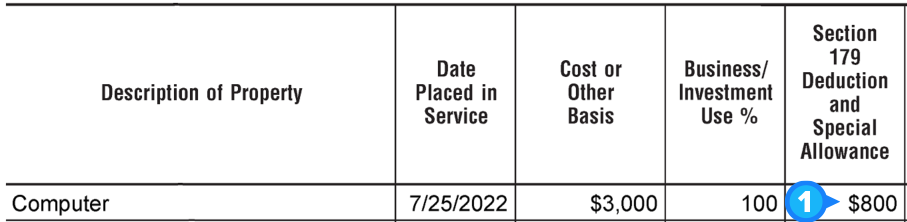

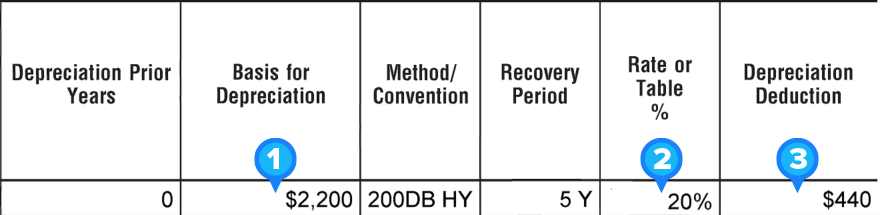

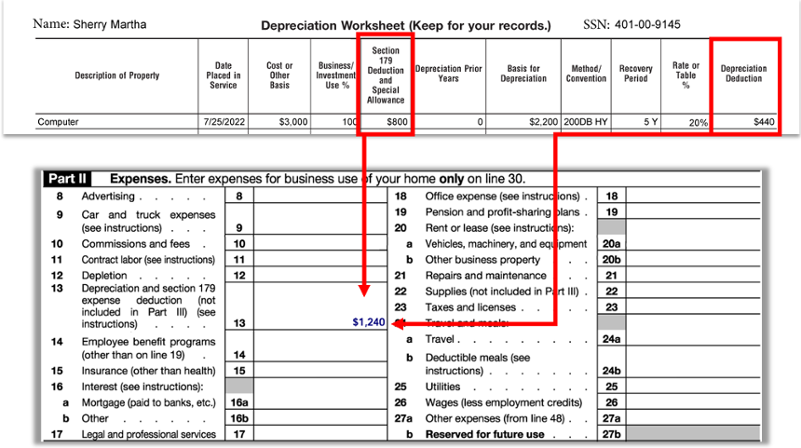

Sherry has a lucrative catering business. During 2022, she purchased a new computer for $3,000. She uses the computer exclusively for business. Per the Tax Code, Sherry will need to depreciate (deduct) the cost over a span of five years unless she elects to deduct the property using the Section 179 deduction.

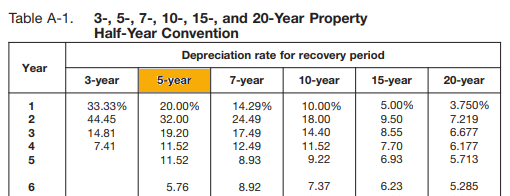

| Tax Year | Percent of $2,200 | Deduction |

|---|---|---|

| 2023 | 32% | $704 |

| 2024 | 19.20% | $422 |

| 2025 | 11.52% | $253 |

| 2026 | 11.52% | $253 |

| 2027 | 5.76% | $127 |

We are so glad you asked! For 2022, a taxpayer generally may elect to immediately deduct up to a total of $1,080,000 of the cost of certain property in the year the property is placed into service instead of recovering that amount through depreciation.

Eligible property includes new or used property purchased by the taxpayer for use in their trade or business. There are restrictions as to what property is eligible. For our purposes in this introductory tax course, the first two are the ones seen most often. The last four are a bit more complex and more research would be needed. Publication 946 would be a good start:

EXAMPLE

On May 19, 2022, Jim purchased a machine for use in his business for $100,000. He may, if he wishes, claim the §179 deduction for the whole cost in the year of purchase, or he may depreciate it and claim the expense over its useful life.The Section 179 deduction must be claimed in the year the asset is purchased. If an asset is first used by the taxpayer for any purpose for which depreciation is not allowed (such as for personal use), the §179 deduction will never be available to that taxpayer for that asset.

EXAMPLE

Rosalyn purchased a computer entirely for personal use in 2019. In 2022, she started using it for business purposes. She may not claim a §179 deduction for the computer, but she may begin depreciating it.Continue reading for our tax plot twist number two!