Table of Contents |

A taxpayer may have other adjustments to income that do not have a designated line to be reported on Form 1040 or any of the schedules. Schedule 1 (Form 1040), line 24, is titled “Other adjustments” and can be considered a “catchall” for those other types of adjustments.

The following list describes common other adjustments on lines 24a through 24z of Schedule 1:

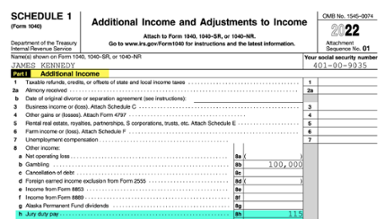

Jury duty pay (line 24a). If a taxpayer receives jury duty pay from the government and their employer pays the taxpayer a salary or for their time at jury duty, the taxpayer often has to repay the amount they received for jury duty. If they have to repay the jury duty pay, they first have to include the amount they received as income on Schedule 1, line 8h, but can then delete the amount they repaid on Schedule 1, line 24a.

|

|

|

Schedule 1, Page 1 Jury duty income |

Schedule 1, Page 2 Jury duty adjustment to income |

Deductible expenses related to income reported on line 8l from the rental of personal property engaged in for profit (line 24b). If the taxpayer has income from renting their personal property, they may deduct expenses related to the income here as an adjustment to income.

Attorney fees and court costs for actions involving certain unlawful discrimination claims (line 24h). The deductible attorney fees and court costs for actions settled or decided involving certain unlawful discrimination claims can be an adjustment to income here.

Other adjustments (line 24z). If there are other adjustments to income for which there are no corresponding lines on the Form 1040, these “write-in” adjustments are entered here.