Table of Contents |

Periodically contributing to a savings or investment account is a great way to increase your wealth, prepare for unexpected emergencies, or plan for the future.

One way in which to save money is to use an annuity, which is a sequence of periodic deposits or payments.

EXAMPLE

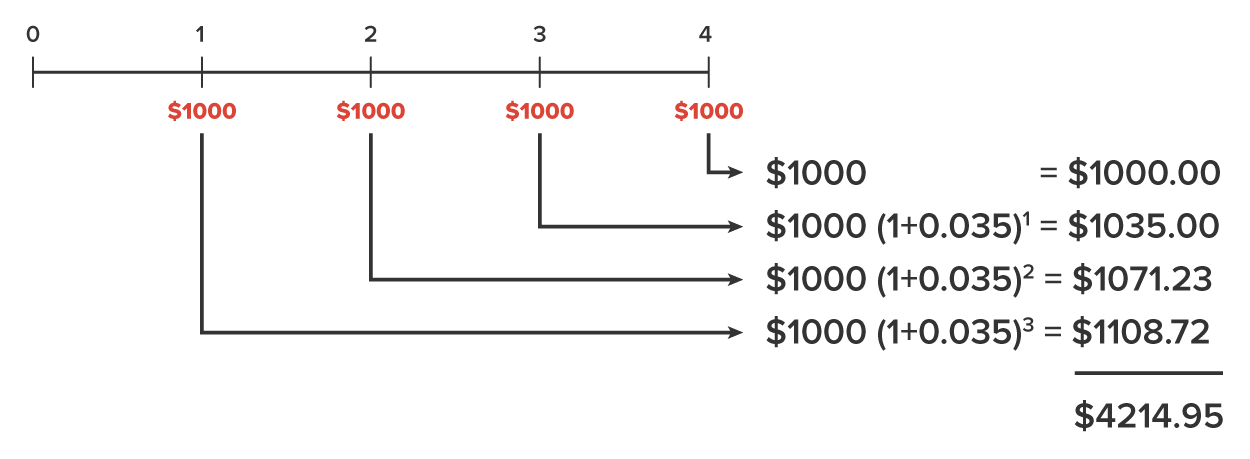

An investment consists of $1,200 deposits at the end of each year. This account gains 3.5% interest each year, applied at the end of the year. Our goal is to compute the amount available in the account immediately after the fourth deposit is made.

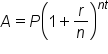

is used to find the amount in an account after t years when P dollars has been invested into an account that pays an annual interest rate of r, compounded n times per year.

When interest is compounded once per year,

is used to find the amount in an account after t years when P dollars has been invested into an account that pays an annual interest rate of r, compounded n times per year.

When interest is compounded once per year,  . This simplifies the formula to

. This simplifies the formula to  .

.

.

. .

.Initiative: Skill in Action |

While the process to find the amount available is fairly straightforward, it is also tedious for situations with more deposits. For example, what if you were making 20 yearly deposits? That would mean calculating 20 values, then adding them together. For this situation, we can use a formula.

Let’s look back at the previous example to get some ideas:

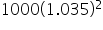

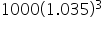

The values of each deposit at the end of 4 years were 1000, 1000(1.035),  , and

, and  . Notice that the only thing that changes between two consecutive terms is the exponent on the 1.035, which means that to get from one term to the next, we multiply by 1.035. A sequence that is formed by doing this is called a geometric sequence, and the constant number that is multiplied to each term to get the next term is called the common ratio.

. Notice that the only thing that changes between two consecutive terms is the exponent on the 1.035, which means that to get from one term to the next, we multiply by 1.035. A sequence that is formed by doing this is called a geometric sequence, and the constant number that is multiplied to each term to get the next term is called the common ratio.

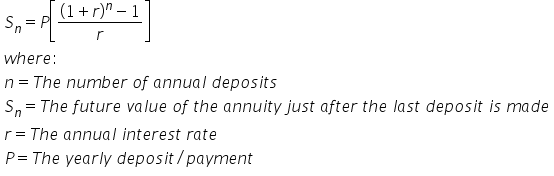

There are special rules we can use to find the sum of the terms of a geometric sequence, and in turn, a formula for the value of a series of deposits immediately after the last deposit is made.

EXAMPLE

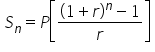

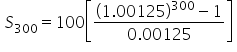

If you make annual deposits of $10,000 into a retirement account at the end of each year for the next 30 years, how much will be in the account right after the last deposit is made? Assume an annual interest rate of 2.5%.

|

The future value formula for an annuity. |

|

Substitute

|

|

Compute the quantity in brackets. |

|

Simplify. |

|

|

The future value formula for an annuity. |

|

Substitute

|

|

Compute the quantity in brackets. |

|

Simplify. |

Not all investments are made up of yearly deposits. One example is a retirement account in which deposits are made monthly. The formula can be adapted to annuities in which deposits are made more than once per year, as long as the interest rate, r, and number of payments, n, are adjusted as well.

EXAMPLE

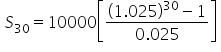

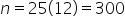

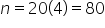

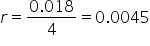

Suppose an annuity consists of monthly deposits for 30 years, where the annual interest rate is 1.2%, compounded monthly. Then, there are deposits, meaning

deposits, meaning  .

. .

.

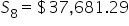

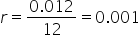

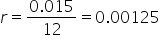

EXAMPLE

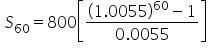

After opening a Roth IRA, you decide that you can afford to deposit $100 into your account at the end of each month for the next 25 years. If the annual interest rate stays steady at 1.5%, compounded monthly, how much will be available in this account after the last deposit is made? .

. .

.|

|

The future value formula for an annuity. |

|

Substitute

|

|

Evaluate the quantity in brackets. |

|

Evaluate completely. |

.

. .

.|

|

The future value formula for an annuity. |

|

Substitute

|

|

Evaluate the quantity in brackets. |

|

Evaluate completely. |

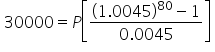

There are situations where you have an investment goal in the future and want to know the payment connected to that goal. The same formula is used; we’ll just need to solve that formula for P.

EXAMPLE

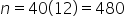

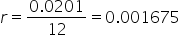

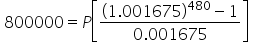

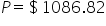

Suppose that in 40 years, you will want a lump sum of $800,000 available to you for retirement. What monthly payment is required to meet this goal, assuming an annual interest rate of 2.01%, compounded monthly? .

. .

.|

|

The future value formula for an annuity. |

|

Substitute

|

|

Evaluate the quantity in brackets. |

|

Divide by 736.0946444 to solve for P. |

.

. .

.|

|

The future value formula for an annuity. |

|

Substitute

|

|

Evaluate the quantity in brackets. |

|

Divide both sides by 96.038301396 to solve for P. |

Source: THIS TUTORIAL WAS AUTHORED BY SOPHIA LEARNING. PLEASE SEE OUR TERMS OF USE.