In operations management, and really, in any part of a business there is risk involved. Successful businesspeople understand these risks and take steps to manage them. In this lesson, you will receive an overview of risk management and the process for managing risks. Specifically, this lesson covers the following:

1. Risk Management

Effective risk management is essential for maintaining operational stability and safeguarding production against a wide range of potential disruptions. Risk management includes Identifying, Assessing, and Controlling (IAC) vulnerabilities, threats, and events—both expected and unexpected—that impact production.

-

Risk management involves identifying, assessing, and managing an organization’s production process to ensure the smooth and consistent delivery of earnings, operations, and a positive public reputation.

These risks originate from various sources, including but not limited to:

- Financial uncertainty

- Legal liabilities

- Technology vulnerabilities

- Accidents

- Natural disasters

Understanding the different types of risk is essential for effective decision making and strategic planning as each type presents unique challenges and implications for organizations.

There are basically two types of risk:

-

Speculative risk:

This is a type of risk that can create a loss or a gain, based on the situation. You may not always be sure about the magnitude of that loss or gain, such as when designing a new product or investing in a stock. There is risk involved with both of those actions, and the outcome could go either way. You can have a gain or a loss, but you won’t always be sure of what the magnitude—the amount of gain or loss—is going to be.

-

Pure risk:

This is a type of risk that creates only a loss or a no-loss situation. You either survive and do well, or you have a complete loss. Think of a hurricane hitting a house or destroying a building. This is a risk that is completely beyond the risk taker’s control; it exists outside of their ability to speculate on it or control it in any way.

Within these types of risks, companies also consider other risks that fall into the speculative risk category:

- Strategic

- Compliance or legal

- Reputational

- Environmental

- Political and economic

|

- Cybersecurity and technology

- Health and safety

- Project

- Human

|

These risks can affect the stability and success of an organization. Strategic risk occurs when poor decisions are made or the organization fails to adapt to changing environments, while operational risk stems from internal failures such as system breakdowns or human error. Another critical category is compliance or legal risk, which involves penalties or losses resulting from not following laws and regulations. Reputational risk threatens a company’s image and customer trust, often arising from scandals or poor service. Environmental risk includes threats from natural disasters, climate change, or environmental regulations, and political and economic risk emerges from instability, policy changes, or economic downturns.

As technology becomes increasingly central to operations, cybersecurity and technology risk—including hacking, data breaches, and IT system failures—has grown significantly. Health and safety risk relates to potential harm to employees or customers due to unsafe practices, while project risk concerns uncertainties in meeting goals for time, cost, scope, or quality. Finally, human risk involves issues such as employee behavior, turnover, morale, and inadequate training. Understanding and managing these risks is essential for organizational resilience and long-term success.

Now, we can take a look at how companies manage these risks.

-

- Risk Management

- The classifying and evaluating of potential hazards for an organization and developing a systematic response (or nonresponse) to avert or lower the damage.

- Speculative Risk

- A type of risk that can create a loss or a gain, based on the situation.

- Pure Risk

- A type of risk that creates only a loss or a no-loss situation.

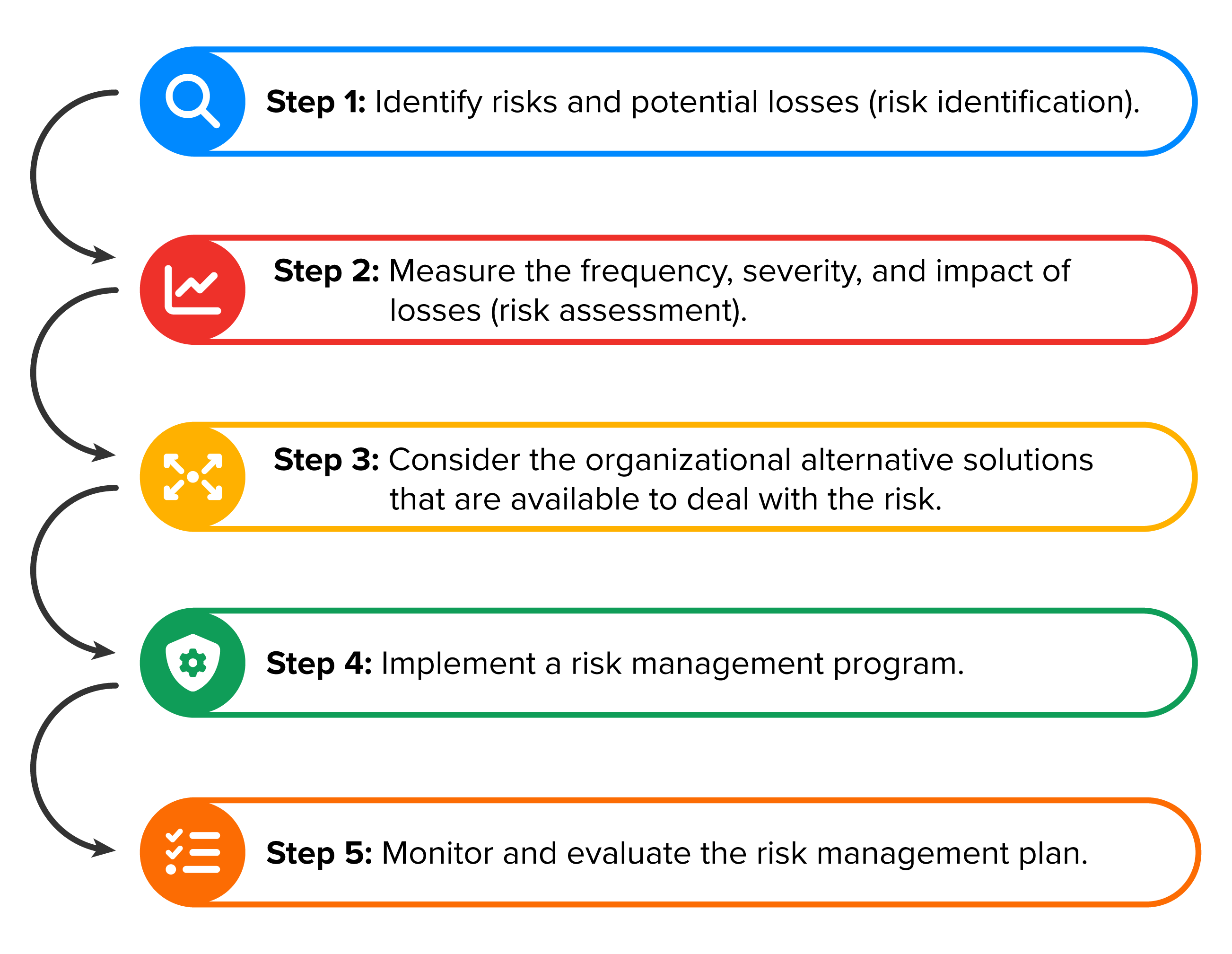

2. Five Steps in Risk Management

The five steps of risk management are as follows:

-

Risk Management

Here are some tools and techniques used in risk management:

- SWOT analysis (strengths, weaknesses, opportunities, and threats)

- PESTLE analysis (political, economic, social, technological, legal, and environmental)

- Monte Carlo simulation

- Scenario planning

- Business and economic impact analysis

Click through the slideshow to see how these tools and techniques are used at each step:

Step 1: Risk Identification:

This involves recognizing threat patterns, both internal and external.

Practical tools and methods used in this step include, but are not limited to, SWOT analysis, brainstorming, and auditing.

Step 1: Risk Identification:

Questions to ask yourself:

- What can go wrong?

- Are your suppliers being paid on time?

- Are your employees happy at their jobs?

- Are the key business activities secure?

All of these things are important for any business, small or large, to look at and analyze.

Step 2: Risk Assessment:

This step involves assessing the likelihood and the potential impact of each risk.

Common tools and techniques include, but are not limited to, risk matrices (probability vs. severity), failure mode and effect analysis (FMEA), and quantitative models like Monte Carlo simulations.

Step 2: Risk Assessment:

Questions to ask yourself:

- What is the likelihood of the risk occurring, and if it does occur, what is its impact?

- Do you pay your suppliers late all the time?

- What would be the potential impact of this on your business?

It is very important to analyze this because it can impact your business for years to come. This step typically involves a risk prioritization process when an organization encounters multiple risks simultaneously. It employs a matrix to assess the urgency and severity of each threat, helping to allocate resources to the most critical risks.

Step 3: Consider Alternative Solutions:

What are the choices you can make as an organization to deal with these types of risks? There are basically five different choices that you can use:

1. Risk avoidance: This refers to avoiding or stopping risky practices altogether.

-

Example: You might decide not to enter an industry you don’t fully understand or avoid entering a volatile foreign market.

2.

Risk control/mitigation/reduction: This refers to attempting to minimize the frequency of risky practices. It involves not taking as many risks going forward as you did earlier and choosing appropriate strategies.

- Example: Having a fire extinguisher on every floor in a building and training people to use it can reduce the damage from a potential fire.

Step 3: Consider Alternative Solutions:

3. Risk retention/acceptance: This refers to when you cannot avoid risks. You need to make sure that the costs of those risks are assumed.

-

Example: If people aren’t paying their credit card bills on time or at all, you look at that risk and make sure you’re accounting for it.

4.

Risk transfer: This refers to transferring large risks to another firm.

-

Example: Having insurance would involve transferring risks to someone else. If you suffer a loss, then the insurance company will pay for that loss.

5.

Risk sharing: This refers to distributing a risk among several parties to minimize each one’s exposure.

- Example: You can engage in a joint venture, a co-investment deal, or a research and development project involving multiple stakeholders.

Step 4: Implement a Risk Management Program:

Questions to ask yourself:

- What are the resources needed?

- What do you need to do to get the necessary approval?

After you’ve identified the risks, measured how severe they are, and considered the choices that you can take as an organization to deal with them, you need to have a good, solid risk management plan in place. This is the organization’s plan to mitigate and deal with potential risks both internal to the organization and risks that happen outside the organization that you may or may not have control over.

Step 5: Monitor & Evaluate the Risk Management Plan:

Questions to ask yourself:

- Is your plan working?

- Does the organization need to make changes or updates?

Make sure that the risk management plan is doing everything that you want and need it to do. This is absolutely essential to ensure that new risks are being considered and that the organization is reassessing the risks that you already know about in light of the new risks.

Tasha, the owner of Glow & Grace Salon, skillfully navigates a variety of risks to keep her business thriving and her clients glowing:

IN CONTEXT: Risks at Glow & Grace Salon

To manage financial risk, she tracks cash flow closely, offers prepaid packages for hair and skincare services, and keeps a cushion in her business account for slow months. When facing market risk, like changes in beauty trends or economic downturns, Tasha stays nimble—introducing new services like brow lamination or scalp treatments to keep clients interested and revenue steady. She mitigates credit risk by requiring deposits for high-ticket services like bridal packages and charging cancellation fees to protect against last-minute no-shows. To minimize liquidity risk, she balances her retail inventory smartly, avoiding overstocking products that might expire or go out of style.

To manage financial risk, she tracks cash flow closely, offers prepaid packages for hair and skincare services, and keeps a cushion in her business account for slow months. When facing market risk, like changes in beauty trends or economic downturns, Tasha stays nimble—introducing new services like brow lamination or scalp treatments to keep clients interested and revenue steady. She mitigates credit risk by requiring deposits for high-ticket services like bridal packages and charging cancellation fees to protect against last-minute no-shows. To minimize liquidity risk, she balances her retail inventory smartly, avoiding overstocking products that might expire or go out of style.

In terms of operational risk, Tasha invests in reliable scheduling software, trains her staff on customer service and hygiene protocols, and performs routine equipment checks to avoid broken equipment mid-appointment. She tackles strategic risk by reviewing client feedback, watching competitors, and experimenting with loyalty programs and pop-up events to keep her brand fresh. For compliance and legal risk, Tasha ensures her team is properly licensed, follows all state health codes, and keeps up with insurance coverage for both liability and workers’ compensation.

Reputation is everything in the beauty industry, so to avoid reputational risk, Tasha encourages honest reviews, responds promptly to client concerns, and maintains a classy and welcoming salon vibe that clients love to post on social media. With environmental risk, she focuses on sustainability—partnering with eco-conscious brands and implementing recycling programs for product packaging. Political and economic risks are on her radar too; she adapts pricing when inflation hits and looks for local grants or business support programs when times get tight.

Reputation is everything in the beauty industry, so to avoid reputational risk, Tasha encourages honest reviews, responds promptly to client concerns, and maintains a classy and welcoming salon vibe that clients love to post on social media. With environmental risk, she focuses on sustainability—partnering with eco-conscious brands and implementing recycling programs for product packaging. Political and economic risks are on her radar too; she adapts pricing when inflation hits and looks for local grants or business support programs when times get tight.

As for cybersecurity and technology risk, Tasha secures her digital booking and payment systems with encryption and makes sure client information stays protected. She takes health and safety risk seriously and ensures that her staff follows all sanitation procedures. When managing project risk, such as launching a new service or remodeling a space, she plans carefully, sets a budget, and allows wiggle room for delays or supplier issues. Finally, Tasha manages human risk by fostering a positive work environment, offering professional development, and resolving staff conflicts quickly to keep her team motivated and professional. With her hands-on approach and eye for both detail and big-picture strategy, Tasha is aware of potential risks and tries to mitigate them before they happen but has a plan in place in case they do.

In this lesson, you learned that risk management is the process of identifying, evaluating, and responding to potential hazards that could negatively impact a business. Every company, regardless of size, must consider risk as part of daily operations and long-term strategy. Risks fall into two main categories: speculative risk, which involves the chance of either loss or gain (such as investing in new products), and pure risk, which involves the potential for only loss or no loss (such as damage from natural disasters). Beyond these, companies face specific risks including strategic risk from poor decisions, operational risk from internal failures, compliance and legal risk from regulatory issues, reputational risk from public perception damage, and environmental, political, and economic risks due to external forces. Cybersecurity, health and safety, project-related, and human risks are also key concerns as businesses rely more on technology and people to maintain success.

You also learned that to manage these risks, companies typically follow five steps in risk management. First, they identify potential risks that could affect operations. Second, they analyze how often the risks might occur and how severe the impact could be. Third, they determine how to respond, whether by avoiding, controlling, accepting, or transferring risks. Fourth, they implement a risk management program, which includes creating action plans and allocating necessary resources. Finally, they continually monitor and evaluate the plan to make sure it’s working and adjust it as new risks emerge. This structured approach helps businesses prepare for uncertainty, protect their resources, and increase the likelihood of long-term success.