Table of Contents |

Retirement benefits are an important part of an employee's overall compensation package and are offered voluntarily by an organization. These benefits provide financial security for individuals once they leave the workforce. The primary purpose of retirement benefits is to ensure that employees have a stable income during their retirement years, allowing them to maintain their standard of living without the need to work.

One of the main reasons retirement benefits are important is that they offer peace of mind. Knowing that there is a plan in place for the future can reduce stress and anxiety about financial stability in later years. This assurance can lead to increased job satisfaction and loyalty, as employees feel valued and supported by their employer.

Retirement benefits also play a significant role in attracting and retaining talent. In a competitive job market, offering a comprehensive retirement plan can make a company more appealing to potential employees. It shows that the organization is invested in the long-term well-being of its workforce. This can be a deciding factor for individuals when choosing between job offers.

Another important aspect of retirement benefits is that they encourage long-term financial planning. By participating in a retirement plan, employees are more likely to develop good saving habits and become more financially literate. This can have positive effects on their overall financial well-being, both during their working years and into retirement.

Retirement benefits come in various forms, primarily divided into two categories: defined benefit plans and defined contribution plans.

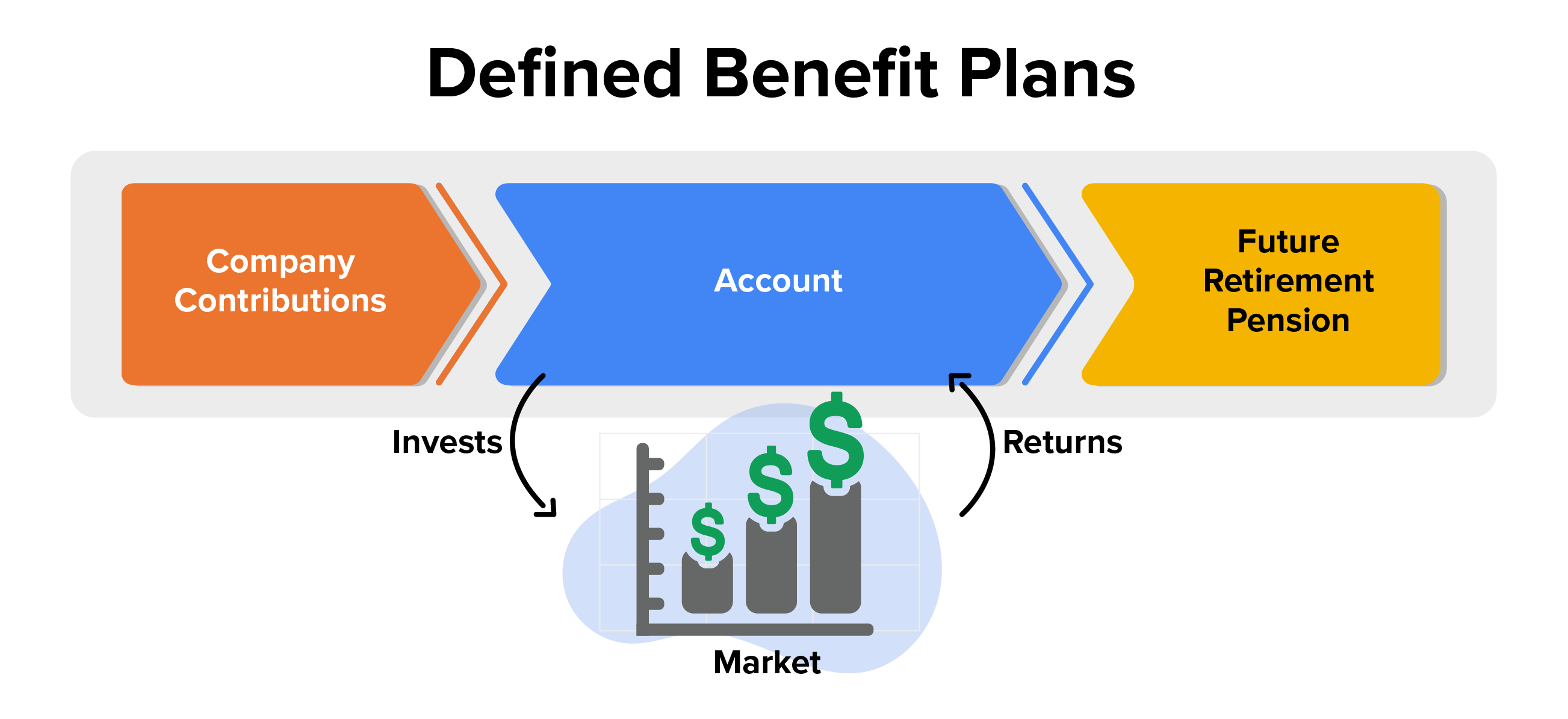

Defined benefit plans promise a specific payout upon retirement, which is usually based on factors like salary history and years of service. The employer is responsible for managing the plan's investments and ensuring there are enough funds to pay the promised benefits. This type of plan provides employees with a predictable income in retirement, as the amount they receive is pre-determined.

On the other hand, defined contribution plans do not promise a specific amount at retirement. Instead, employees and sometimes employers contribute a set amount to the employee's individual account. The final benefit depends on the contributions made and the performance of the investments chosen. This means the retirement income can vary based on how well the investments perform over time.

Defined benefit plans are a type of retirement plan where the employer guarantees a specific payout upon retirement. This payout is usually based on factors such as the employee's salary history and the number of years they have worked for the company. The employer is responsible for managing the plan's investments and ensuring there are enough funds to pay the promised benefits.

These plans work by calculating the retirement benefit using a formula that often includes the employee's final salary and years of service.

EXAMPLE

A plan might promise to pay 1.5% of the employee's average salary over their last five years of employment for each year of service. If an employee worked for 30 years and had an average salary of $50,000, their annual retirement benefit would be $22,500.Defined benefit plans are more common in public sector jobs, such as government positions, and in some large private sector companies. They are less common in smaller companies due to the financial and administrative burden of managing the plan.

There are several pros and cons to defined benefit plans. One of the main advantages is the predictability of the retirement income, which can provide peace of mind for employees. They do not have to worry about investment decisions or market fluctuations affecting their retirement income. Additionally, these plans often provide benefits for life, which can be a significant advantage.

However, there are also downsides. For employers, defined benefit plans can be expensive to maintain, especially if the investments do not perform well. This financial risk is entirely on the employer. For employees, these plans can be less flexible than defined contribution plans, as they typically do not allow for individual investment choices. And though they typically pay out during the life of the employee, if the employee passes first, they may not continue to pay to the surviving spouse.

Examples of defined benefit plans include traditional pensions and some public sector retirement systems. These plans have been a staple of retirement planning for many years, though their prevalence has decreased in favor of defined contribution plans.

IN CONTEXT

Defined Benefits Plan Scenario

Emma has been working for a local municipality for 25 years. Her employer offers a defined benefit plan as part of the retirement package. According to the plan, Emma will receive 2% of her average salary over her last five years of employment for each year she has worked at the company. Emma's average salary during her final five years is $60,000.

Using the plan's formula, Emma's annual retirement benefit is calculated as follows: 2% of $60,000 equals $1,200. Since she has worked for 25 years, her annual benefit will be $1,200 multiplied by 25, which equals $30,000. This means Emma will receive $30,000 each year after she retires.

Emma appreciates the predictability of her retirement income, knowing she will have a steady amount each year. This allows her to plan her finances confidently. However, she also understands that the organization bears the responsibility of ensuring there are enough funds to pay her and other retirees.

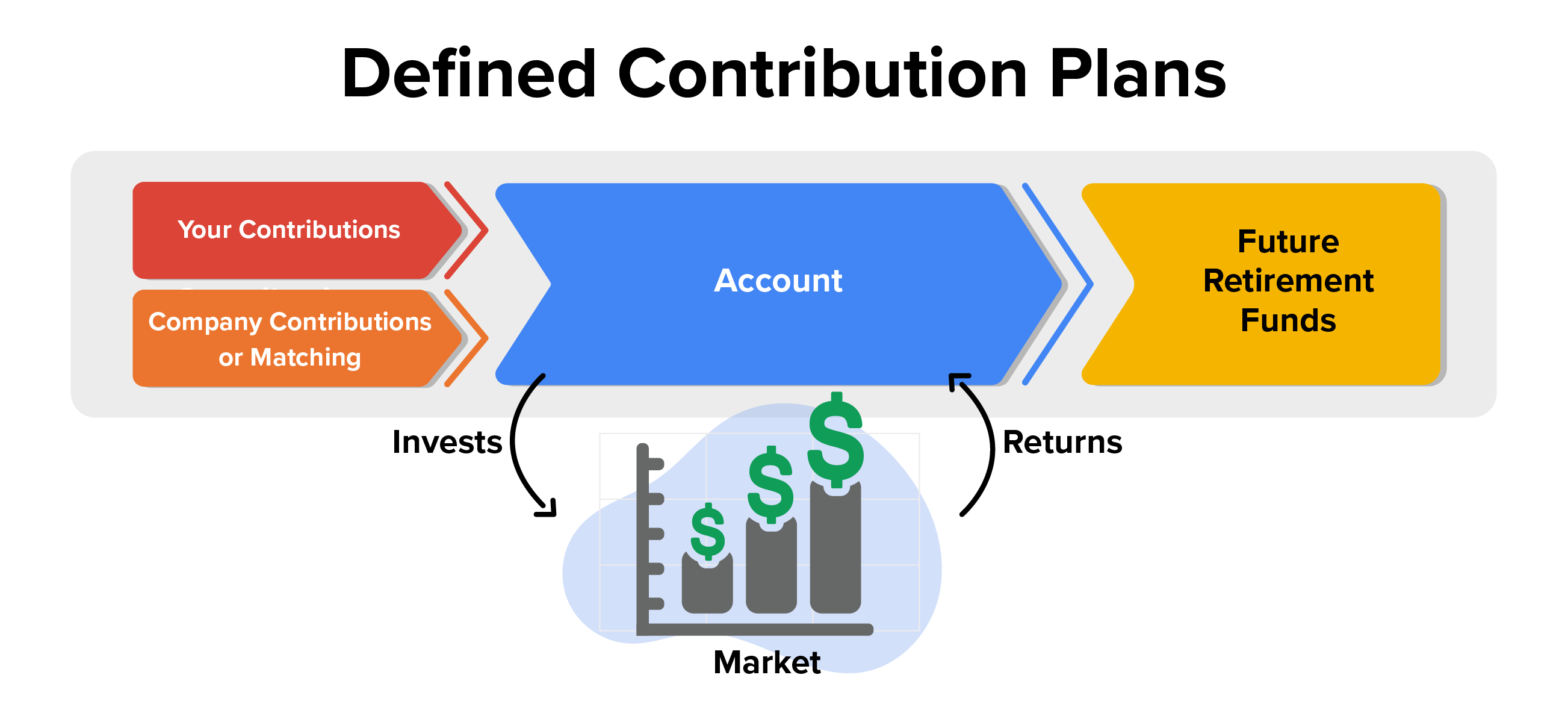

Defined contribution plans are a type of retirement plan where the amount contributed to the employee's account is specified, but the final benefit amount depends on the investment performance. In these plans, both employees and employers can make contributions to the employee's individual account. The contributions are often a percentage of the employee's salary.

The key feature of defined contribution plans is that the retirement benefit is not predetermined. Instead, the amount available at retirement depends on the total contributions made and how well the investments perform over time. Employees typically have some control over how their contributions are invested, choosing from a range of options provided by the plan.

These plans are common in both private and public sectors, especially among employers who prefer to shift the investment risk from the company to the employee. Defined contribution plans are popular because they offer flexibility and potential for growth, allowing employees to tailor their retirement savings to their individual needs and risk tolerance.

There are several pros and cons to defined contribution plans. One advantage is the potential for higher returns, as employees can invest in a variety of assets. Additionally, these plans are portable, meaning employees can take their savings with them if they change jobs. However, the downside is that the retirement income is not guaranteed and depends on market performance, which can be unpredictable.

Examples of defined contribution plans include 401(k) plans, Individual Retirement Accounts (IRAs), and similar retirement savings accounts. These plans have become a staple of modern retirement planning, offering a flexible and customizable approach to saving for the future.

Defined contribution plans offer several features that make them attractive for both employees and employers. One of the main benefits is the tax advantage. Contributions to traditional defined contribution plans, like a 401(k), are made with pre-tax dollars, which reduces the employee's taxable income for the year. The investments grow tax-deferred, meaning taxes are only paid upon withdrawal, typically during retirement when the individual may be in a lower tax bracket.

Employers often enhance these plans by offering matching contributions. A common matching formula might be 50% of the employee's contributions up to 6% of their salary. However, it's important to note that employers are not required to match contributions. When they do, it serves as an incentive for employees to save more for retirement.

Vesting periods are another key aspect of defined contribution plans. Vesting refers to the amount of time an employee must work for the company before gaining full ownership of the employer's contributions. There are different vesting schedules, including cliff vesting, where employees become fully vested after a specific period, and graded vesting, where employees gradually gain ownership over time.

Pros and Cons of Different Vesting Schedules:

IN CONTEXT

Defined Contribution Plan Scenario

Tucker works for a marketing firm that offers a 401(k) plan. He decides to contribute 6% of his salary to his 401(k) account. His employer matches 50% of his contributions, up to 6% of his salary. This means for every dollar Tucker contributes, his employer adds 50 cents—up to the 6% limit.

Tucker earns $50,000 a year, so he contributes $3,000 annually to his 401(k). His employer adds another $1,500, making the total annual contribution $4,500. Tucker chooses to invest his 401(k) funds in a mix of stocks and bonds, aiming for growth over time.

Tucker's plan has a graded vesting schedule, meaning he gradually gains ownership of the employer's contributions over five years. After two years, he is 40% vested, and after five years, he is fully vested. Tucker also has the option to choose between a traditional 401(k) and a Roth 401(k). He opts for the traditional 401(k) to take advantage of the immediate tax benefits.

- Tucker’s contribution is $50,000 x 6% = $3,000

- The employer’s contribution is $50,000 x 6% x 50% = $1,500

- Total contributions are $3,000 + $1,500 = $4,500

By regularly contributing to his 401(k) and taking advantage of the employer match, Tucker is building a retirement fund that will grow through both his contributions and investment returns.

Planning for retirement can seem overwhelming, but there are many resources and tools available to help. One valuable resource is a financial advisor. These professionals can provide personalized advice based on your financial situation and retirement goals. They can help you create a comprehensive retirement plan, choose the right investment options, and adjust your strategy as needed.

Online calculators are another useful tool. These calculators can estimate how much you need to save for retirement based on factors like your current savings, expected retirement age, and desired retirement income. They can help you understand if you're on track or if you need to make changes to your savings plan.

HR departments can also play a key role in retirement planning. Many companies bring in experts to train employees on retirement planning. These sessions can cover topics like understanding your retirement plan options, maximizing employer contributions, and making informed investment choices. HR can also provide resources and support to help you navigate your retirement benefits.

Additionally, conducting annual reviews of your retirement plan can help you stay on track to reach your goals. These reviews allow you to assess your progress, make necessary adjustments, and ensure that your retirement strategy remains aligned with your financial objectives. Another important aspect is setting up payroll deductions for retirement savings and increasing these contributions as your income grows. This approach helps you consistently save more over time and take advantage of market growth, ultimately boosting your retirement savings.

Source: This Tutorial has been adapted from "Human Resources Management" by Lumen Learning. Access for free at courses.lumenlearning.com/wm-humanresourcesmgmt/. License: CC BY: Attribution.