Table of Contents |

You may recall that a cost center is a segment of a business that does not directly contribute to profit, but still costs the organization money to operate. Managers of cost centers are held responsible only for specified cost items that fall under their control. The goal of a cost center is the long-run minimization of costs, thus cost center managers are measured by their ability to adhere to budgeted costs.

In many businesses, there are several different types of cost centers. Cost centers are different for each business. Common examples of cost centers include legal departments, accounting departments, research and development, advertising, marketing, and customer service. Cost centers are necessary for many types of businesses and add value, but do not create revenue and are usually heavily assessed within a business. Sometimes management may want to cut costs and often look to cost centers for those cuts.

Before these cuts can be made, managers need to understand why these centers are so important. Cost centers bring value to a business in various ways:

A revenue center is a responsibility center of a business that is responsible for generating sales. Traditionally these are sales and marketing departments of businesses. A revenue center’s performance is evaluated on the revenues it generates and how that revenue lines up with revenue budgets but is not evaluated on profitability. Because of this, the main focus of a revenue center is to maximize profits through sales, often without consideration of costs or expenses associated with producing that revenue.

As cost centers are not responsible for revenue, revenue centers do not have cost responsibilities. This enables revenue centers to focus on its main goal of generating sales. Beyond having the responsibility of generating sales, revenue centers have other metrics such as sales promotions, customer relationship management, and gained market share. These metrics are what guide managers in decision making for revenue centers.

Revenue centers can be advantageous for companies that want to separate departments that generate revenues from the departments that manage costs. Another advantage of a revenue center is it can develop highly effective sales strategies without having to worry about cost considerations. A disadvantage of a revenue center is if the revenue center is not well-aligned with company objectives, long-term sales could be sacrificed for short-term gains. One reason for this is that salespeople may be paid by commission or some bonus structure, which may incentivize them to push for quick sales without building relationships.

A profit center is a responsibility center having both revenue and expense responsibility, which is ultimately expected to add to a company’s bottom line. In many corporations, profit centers are treated as their own separate standalone business units. Managers often rank profit centers against one another to determine which are most (or least) profitable. This ranking often determines which profit centers receive higher allocations of resources or which profit centers should be eliminated.

Managers of profit centers have autonomy over decisions made on product pricing and control over operating expenses. Profit center managers are measured on the overall profit of their respective center, as measured by revenue growth, gross margin, and net income, and are often given increased profit goals year after year. Because profit center earnings equal controllable revenues minus controllable expenses, the manager must be adept at managing both of these categories. To be a true profit center, the manager must have the authority to control selling price, sales volume, and all reported expense items.

An example of a profit center is different departments in a department store. For example, the shoe department can be considered one profit center, while health and beauty products may be considered another. Whatever the profit center, the profit center manager must be adept at cost minimization and profit maximization in order to be successful.

IN CONTEXT

The International Business Machines Corporation (IBM) has been in business since 1911. Over that time it has morphed from a tabulating machine business to the multinational technology company it is today. As you may imagine, IBM has seen its share of changes in the technology sector.

Recently, IBM has made the decision to cut profitable, but slow growing, segments of its overall business so that it can increase its investments in more profitable segments. As a consequence of conducting business and investment analysis (much like you learned to do in this course), IBM decided that cloud computing and big data analysis are more profitable options and has shifted its investing strategy away from segments with slow growth. The segments that IBM have divested are its semiconductor technology business and its computer and server lines.

Successful companies must make these difficult decisions. It is tough to cut a profitable endeavor, but is often necessary so that scarce investment dollars are put to best use. Other companies such as Ford, General Electric, and Nestle have also used these strategies to help maximize the returns on their investments. Those who research, analyze, and prepare set themselves up for success. Companies that become complacent or do not use managerial accounting tools are at risk of losing in the long run.

Closely related to the profit center concept is an investment center. Where profit centers are only responsible for generating revenues and controlling costs, investment centers have the additional responsibility to utilize assets to increase return on investment. An investment center is then a responsibility center having revenues, expenses, and an appropriate investment base.

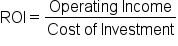

A key advantage of the investment center concept is the ability to measure and compare investment center performance. When a firm evaluates an investment center, it is able to calculate the rate of return it has earned on its investment base, called return on investment or ROI. ROI is an important performance measure used to evaluate the profitability and efficiency of an investment and cannot be calculated for profit centers. We will go into additional detail on calculating ROI for investment centers, as this is not a calculation we have discussed previously.

EXAMPLE

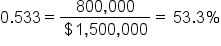

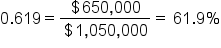

| Coaster Name | Operating Income | Investment Cost |

|---|---|---|

| Fast Times | $800,000 | $1,500,000 |

| Launch Pad | $650,000 | $1,050,000 |

Companies prefer to evaluate segments as investment centers because the ROI criterion facilitates performance comparisons between segments. Segments with more resources should produce more profits than segments with fewer resources, so it is difficult to compare the performance of segments of different sizes on the basis of profits alone. However, when return on investment is a performance measure, performance comparisons take into account the differences in the sizes of the segments. The segment with the highest percentage return on investment is presumably the most effective in using whatever resources it has.

Typical investment centers are large, autonomous segments of large companies. The centers are often separated from one another by location, types of products, functions, and/or necessary management skills. Segments such as these often seem to be separate companies to an outside observer. However, the investment center concept can be applied even in relatively small companies in which the segment managers have control over the revenues, expenses, and assets of their segments.

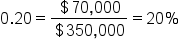

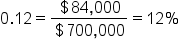

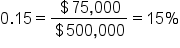

| North Division | South Division | West Division | Total | |

|---|---|---|---|---|

| Income | $70,000 | $84,000 | $75,000 | $229,000 |

| Investment | 350,000 | 700,000 | 500,000 | 1,550,000 |

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.