Table of Contents |

Just as you are responsible for your own personal budget and have to understand what you are earning as well as what money you are spending, businesses have the same type of responsibilities. When a business is small, the owner often bears the full burden for all areas of cash flows and is responsible for costs, profit, revenues, and investments. As a business grows and more employees are added, these responsibilities are shifted to key employees who are accountable for them.

Responsibility accounting is a system of control where ownership of a specific business objective is given to an employee. That employee then becomes responsible for that particular piece of the business, and accountability for the success (or failure) of those business objectives falls on them.

More specifically, responsibility accounting refers to an accounting system that collects, summarizes, and reports accounting data relating to the responsibilities of individual managers. A responsibility accounting system provides information to evaluate each manager on the revenue and expense items over which that manager has primary control or authority to influence.

Under the umbrella of responsibility accounting, businesses typically have four responsibility centers: cost, profit, revenue, and investment. A responsibility center is a unit within an organization that is headed by a manager who is responsible for its activities. Responsibility center managers help accomplish the goals of the organization and must work in conjunction with one another to ensure business success.

In order for a business to set up responsibility centers, assign those centers to employees, and assess the performance of each center, the business needs to have the following in place:

Each responsibility center manager is held accountable for that particular center and should report their activities to someone who manages the overall system. An organizational chart helps in determining these responsibilities. To identify the items over which each manager has control, the lines of authority should follow a specified path.

EXAMPLE

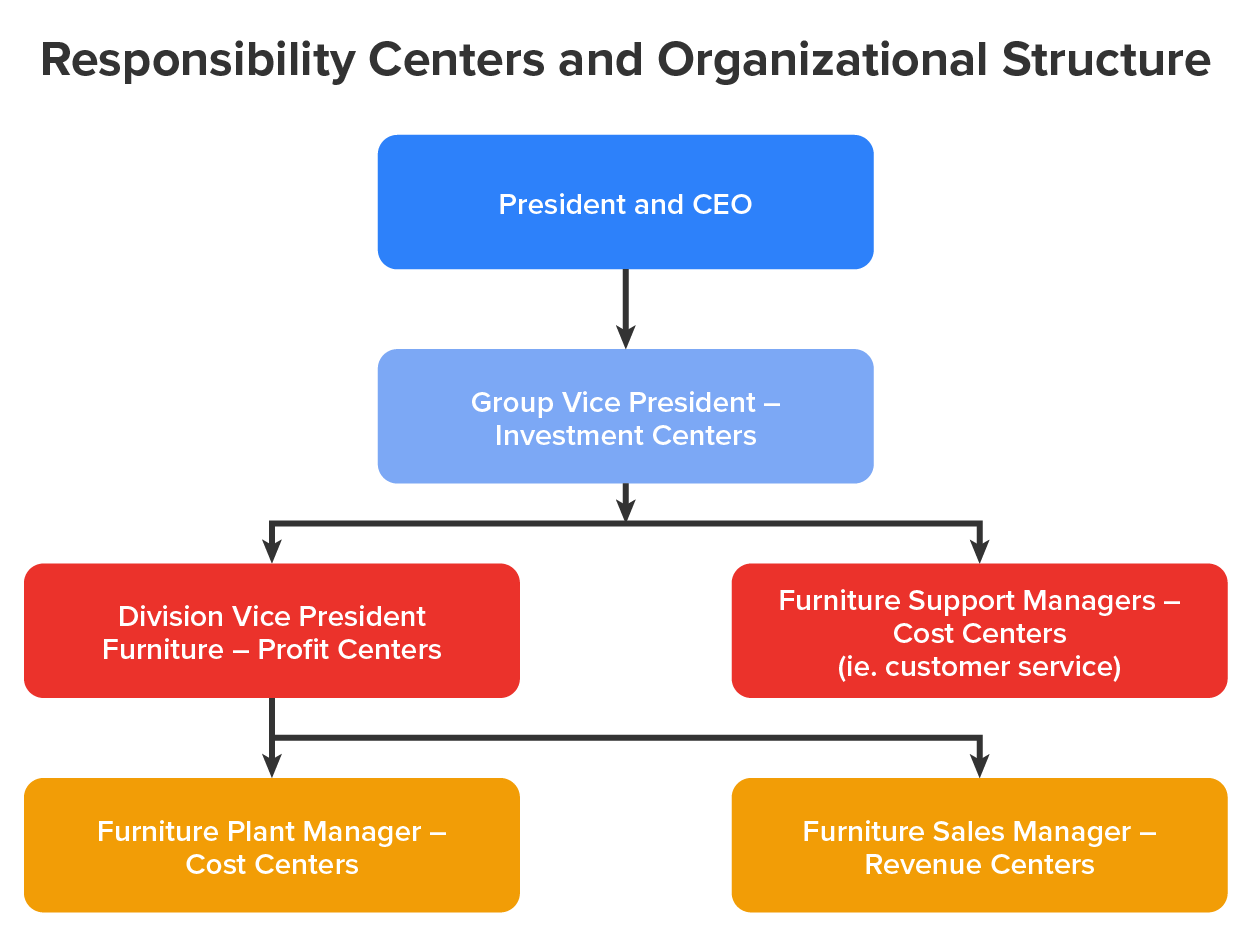

As an example, consider a growing furniture business. This furniture business needs salespeople to help generate revenue (revenue centers). The furniture they sell needs to be manufactured in order to sell it. This is where the responsibility center of the plant provides value in the supply chain. Both the plant manager and the sales manager report directly to the furniture division vice president. This division vice president’s responsibility is considered to be a profit center since he is overseeing both revenues and costs. The group vice president is responsible for an investment center as she is in charge of the investments that provide resources to the responsibility center leaders. Finally, the president oversees all of the responsibility centers and is given appropriate aggregate accounting information from the group vice presidents. This information is used to make decisions about company direction and funding.

Responsibility center managers must understand what is to be considered optimal performance. If these standards of measurement (goals) are not clearly defined, it is difficult for the center manager and their supervisors to determine if they are performing well.

EXAMPLE

Following our furniture business example, the division vice president needs to understand how the cost and revenue centers incur costs and generate revenue. One of the charges of the group vice president is to clearly define the metrics of what successful operations are, so the cost and revenue centers know their goals and can plan on how best to achieve them.A manager is only as good as the information they have. If center managers base their decisions on bad or faulty information, then the success of their center is at risk. Businesses need to strive to collect and use only useful and accurate information to get the best results.

EXAMPLE

All information must be accurate in order for managers to make relevant decisions. If the furniture sales manager predicts higher than usual sales, this would prompt the division vice president to inform the furniture plant manager to produce more furniture. If the sales manager made a mistake, this would cause the company to have a large inventory of furniture. This inventory has costs that are incurred with it, which hurts the company’s bottom line.As a center manager is doing their work, they will frequently produce reports that inform the responsibility managers of the progress of their center. Responsibility managers should then provide periodic feedback about the center's performance and how their work is affecting other areas of the business. This feedback should come from the center manager’s supervisor and should be clear, timely, and concise.

EXAMPLE

For our furniture store, the division vice president should receive reports from the furniture plant manager and the furniture sales managers, as updates on progress. The division vice president then would provide feedback either to let these managers know they are meeting or to help these managers work toward achieving the standards of measurement as defined in 1b.Controllable factors are those factors that can be regulated by a particular center manager’s actions and decisions. Responsibility center managers should and will be accountable for these controllable factors. Uncontrollable factors are those factors that are beyond the sphere of influence of a center manager. Responsibility center managers should understand and work with uncontrollable factors, but should not be held responsible for all risks associated with them.

EXAMPLE

As a center manager, it is important to know which factors you can control and which are beyond your influence. Since uncontrollable factors are not within the center managers’ purview, they should not be held responsible for them by their vice president. Conversely, vice presidents need to keep these uncontrollable factors in mind when setting center goals.| Controllable Factors | Uncontrollable Factors |

|---|---|

| Material costs | Factory rent |

| Labor costs | Most overhead costs |

| Cost of marketing and advertising | Fixed costs |

| Training costs | Cost of licenses |

Just as a student writes a report that showcases their knowledge on a particular topic, responsibility center managers report on the status of their centers to their managers and other interested stakeholders within the business. Responsibility reports are accounting reports prepared by responsibility center owners, for various levels of management in a company’s organizational chart, that contain items that are controllable by the responsibility center manager. These responsibility reports can be brief or extremely detailed, depending on what upper management wants and needs to know.

EXAMPLE

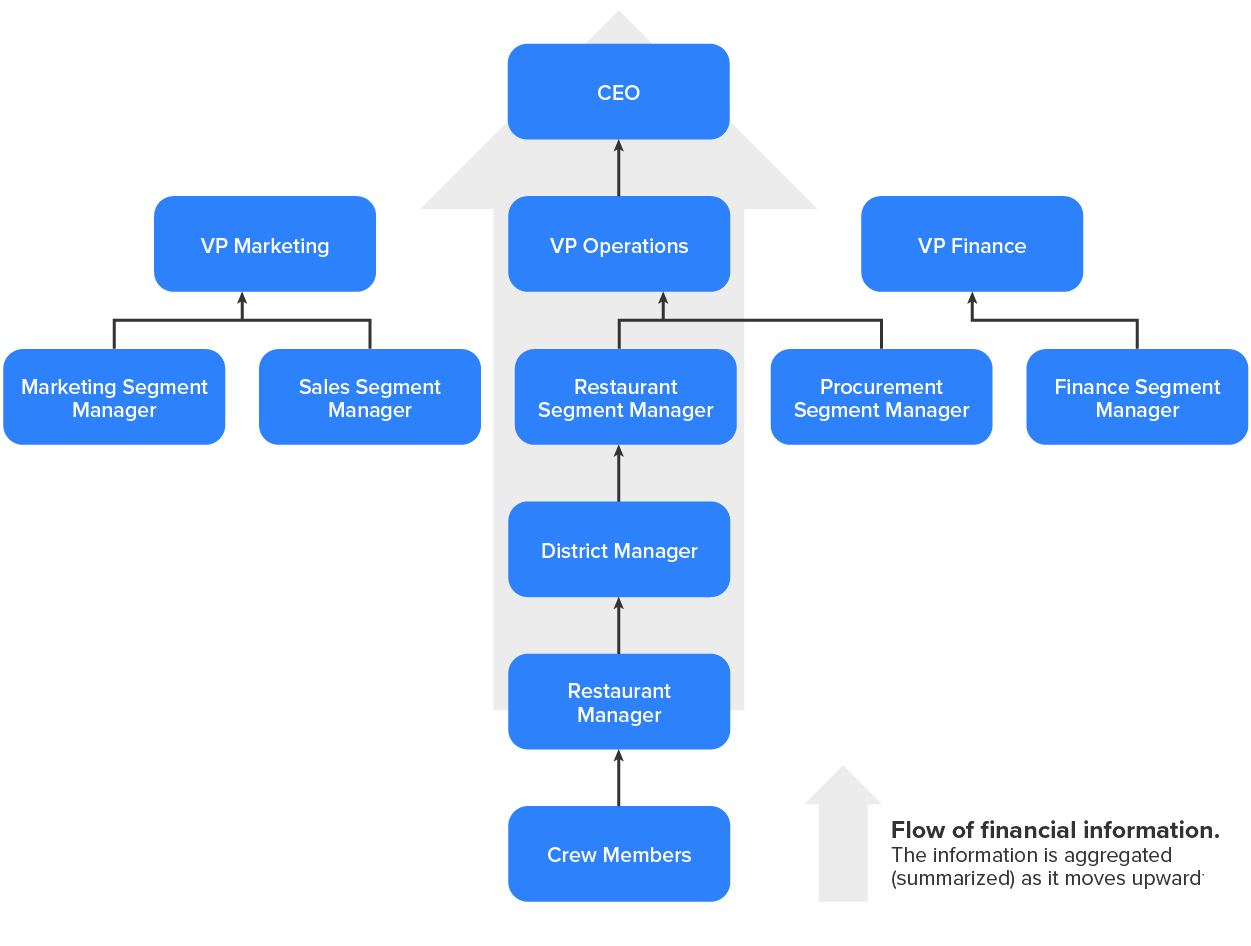

Rebekah is a regional manager of a restaurant chain. In order to understand the current operations of each of the franchises in her region, she needs detailed reports from each franchise manager. The reports include actual and budgeted dollar amounts of all revenue and expense items under that franchise manager's control. Rebekah then gives feedback to each of the restaurant managers on the state of their operations and the financial well-being of the franchise.An executive summary is a summary of aggregated data that allows senior management to make effective decisions. Aggregated data is high-level data that is summarized from separate individual reports. The figure below shows the movement of accounting data and the aggregation of the data as it moves up the organizational chart.

Responsibility reports enable managers, in different levels of the organization, to identify and address problems. This type of management style is called management by exception. Management by exception is the principle that upper-level management does not need to examine operating details at lower levels unless there appears to be a problem. As businesses become increasingly complex, responsibility center managers have found it necessary to filter and condense accounting data so that these data may be analyzed quickly. Most executives do not have time to study detailed accounting reports and search for problem areas. Reporting only aggregate totals highlights any areas needing attention and makes the most efficient use of the executive's time.

IN CONTEXT

In 2021, amid the COVID pandemic, one of the industries that was hit hardest was the restaurant industry. Many restaurants were forced to shut their doors, while others remained open but allowed fewer people to dine due to social distancing requirements. Food prices were rising stemming from supply chain issues, so restaurants had to make difficult decisions.

One restaurant chain that had a particularly difficult decision to make was Wingstop. Among all of the other COVID worries, Wingstop also had to deal with a chicken wing shortage that was plaguing the industry. Chicken wings were difficult to get, and even if you could buy them, they were expensive. Seeing these rising costs and lack of availability in responsibility center reports, executives had to think of something. The answer was chicken thighs.

Chicken thighs were readily available, were much less expensive than wings and could be prepared in the same way. Using management by exception principles, management at Wingstop identified and provided a solution to this problem. This tactic helped Wingstop survive the pandemic through creative thinking. Accounting data helped executives identify the issue, manage through this exception, and navigate a chicken wing restaurant through a chicken wing shortage.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.