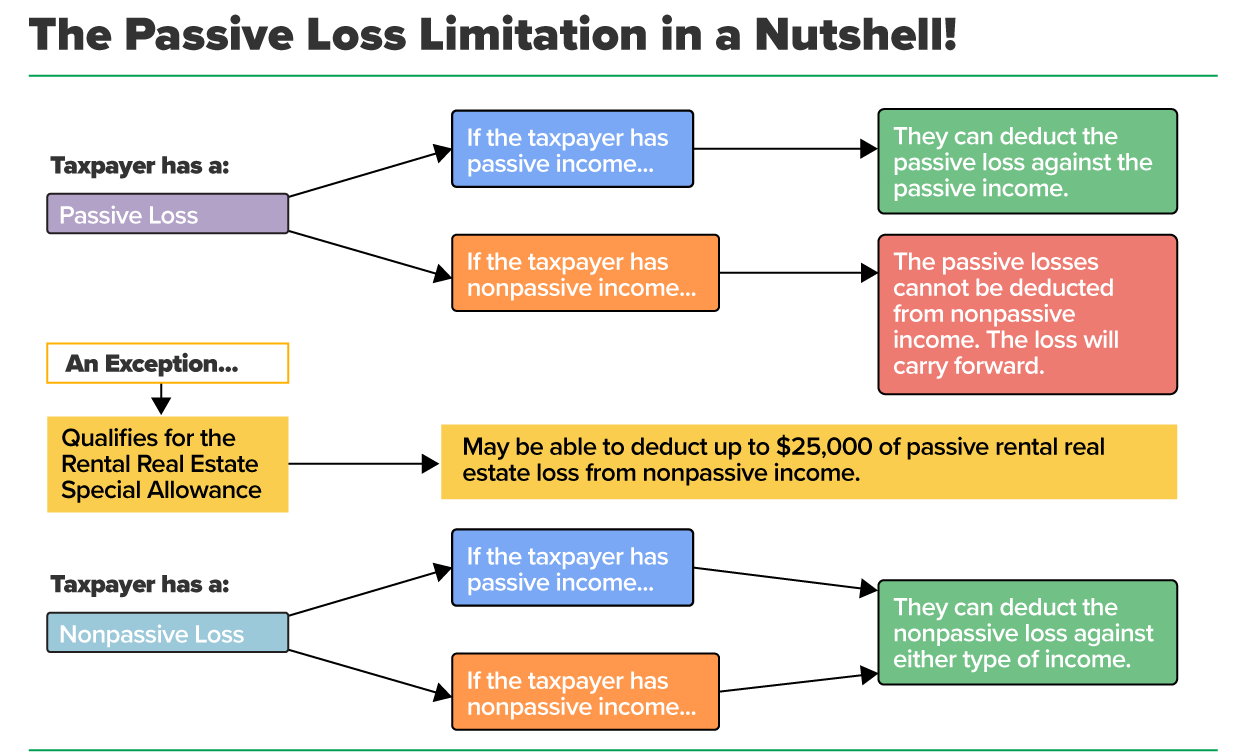

As established earlier in the chapter, rental real estate is generally a passive activity. Passive losses are limited to the amount of passive income or are carried forward until there is passive income or a disposition of the property.

The most common passive loss situations involve rental activities similar to those of Albert Hawking in Exercise 14.2. As you will recall, Albert had inherited his parents’ home and had converted it to rental property. There are times rental activities will generate a passive loss, especially in the early years of renting the property, and the passive loss limitation will apply.

However, there is one exception to the passive loss limitation for taxpayers who meet certain qualifications. These taxpayers:

A taxpayer actively participates in their rental real estate activity when they or their spouse, if married, own at least 10% of the property and make management decisions in a significant and bona fide sense. Management decisions include:

Active participation isn’t the same as material participation. Active participation is a less stringent standard than material participation. Active participation only relates to the rental real estate special allowance, and material participation relates to participation in a trade or business.

EXAMPLE

Benjamin Coffin III is the only owner of a rental house. He approved the tenant before they moved in. He also met with the tenant and their attorney to sign the lease agreement. He makes himself available to the tenant when any repairs or maintenance need to be made to the property, and he processes the rent payment each month.For all filing statuses except married filing separately, as long as the taxpayer actively participates and meets the modified AGI requirements, the taxpayer can deduct up to $25,000 of their rental real estate passive losses against nonpassive income.

However, if the taxpayer is filing married filing separately and did not live with their spouse at all during the year, actively participates, and meets the modified AGI requirements, they can deduct up to $12,500 of their rental real estate passive losses against nonpassive income.

Lastly, if the taxpayer is filing married filing separately and lived with their spouse at any time during the year, they do not qualify to use the rental real estate special allowance.

For taxpayers with modified adjusted gross income (MAGI) above $100,000, there is a limit on the $25,000 annual rental loss deduction against other income.

The maximum special allowance of $25,000 ($12,500 for married individuals filing separate returns and living apart at all times during the year) is reduced by 50% of the amount of the taxpayer’s modified adjusted gross income that is more than $100,000 ($50,000 if the taxpayer is married filing separately). If the modified adjusted gross income is $150,000 or more ($75,000 or more married filing separately), the taxpayer cannot use the special allowance.

Modified AGI, for purposes of active-participation passive loss limitations, consists of the taxpayer’s adjusted gross income without taking into account:

EXAMPLE

Roger Davis owns a rental house in which he actively participates in the rental activity. On Schedule E, his loss for the rental property is $1,300. Roger is filing single, and his modified AGI is $96,000. Roger will be allowed to deduct the full $1,300 loss from his other income because he qualifies to use the rental real estate special allowance.Form 8582, Passive Activity Loss Limitations, is used to compute the necessary limitations. You will not be required to complete Form 8582 in this course. However, it is a very important form for audit purposes.

The following steps are used in determining the phaseout amount that is applied to the passive loss:

EXAMPLE

Maureen Johnson owns a rental house in which she actively participates in the rental activity. Her loss on Schedule E for the rental property is $12,500. Maureen is filing single, and her modified AGI is $145,000.