If any of the qualifying child requirements are not met, it only means they are not a qualifying child. They may still be a qualifying relative dependent, and those requirements are considered next.

If any of the qualifying child requirements are not met, it only means they are not a qualifying child. They may still be a qualifying relative dependent, and those requirements are considered next.

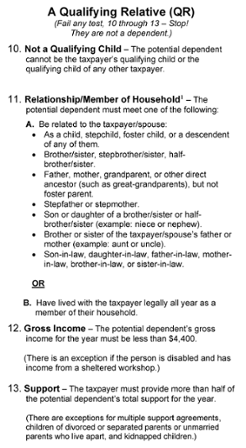

For an individual to be a qualifying relative (QR) of a taxpayer, an individual must satisfy four tests:

To meet this test, the potential dependent must not be the qualifying child of the taxpayer or of any other taxpayer. In other words, a potential dependent who is a qualifying child of one taxpayer cannot be claimed as a qualifying relative by another taxpayer.

EXAMPLE

Remember Melissa, from the previous Qualifying Child Example? Melissa (17) is a qualifying child of her mother, Jill. She did not meet the residency requirement for Rhett, her stepfather. Because Melissa is a qualifying child of Jill, she cannot be a qualifying relative of Rhett. Additionally, because she is Jill’s qualifying child, Melissa cannot be Jill’s qualifying relative.EXAMPLE

Yolanda lives with her daughter, Elizabeth. Elizabeth is the qualifying child of Yolanda. Neither Yolanda nor anyone else can claim Elizabeth as their qualifying relative, since Elizabeth meets the definition of a qualifying child.EXAMPLE

Ron (35) and Sue (35) are married and have two children, Todd (8) and Tracy (6). Neither child has income. Stacy (13), Sue’s child from a previous marriage, came to live with them on July 4, 2022. Prior to moving in with Ron and Sue, Stacy lived with her father, John.EXAMPLE

Aiden #1EXAMPLE

In 2007, Mark and Mindy lived together as an unmarried couple all year. Mindy’s six-year-old daughter, Marissa, from a previous relationship, lived with them all year. Mark was the only member of the household with income.The relationship test for a qualifying relative is broader than the test for a qualifying child. The individual must meet one of two requirements:

If the taxpayer files a joint return, the person can be related to either the taxpayer or their spouse. For example, a spouse’s uncle who receives more than half of his support from the taxpayer may be claimed as the taxpayer’s qualifying relative, due to the relationship, even though the uncle does not live with the married couple. However, if the taxpayer and their spouse file separate returns, the spouse’s uncle can only meet the qualifying relative test if the spouse’s uncle lives with the taxpayer all year under the member of household part of the requirement.

Per Publication 17, a taxpayer does not meet this test if, at any time during the year, the relationship between the taxpayer and the potential dependent violates local law.

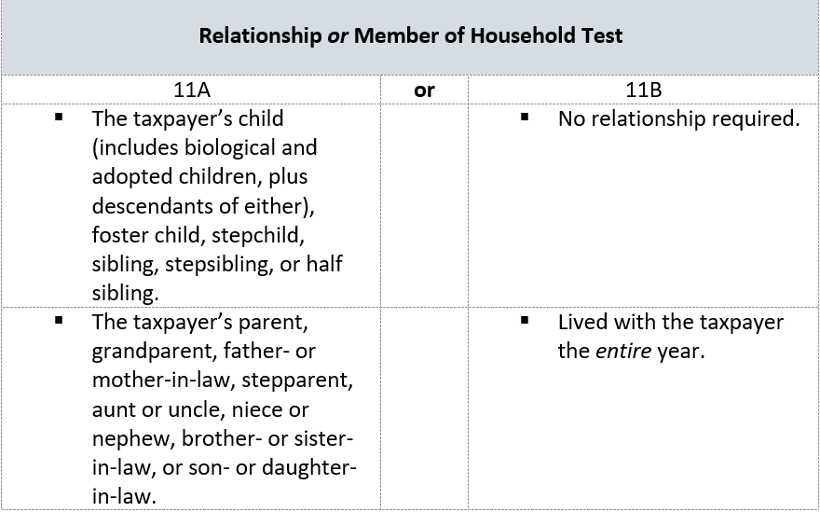

The Relationship or Member of the Household test has caused a lot of confusion among tax preparers. It is important to realize this test is a choice between the two options. The potential dependent either passes by having one of the required relationships, or they pass the member of the household part by living with the taxpayer the entire year.

EXAMPLE

Aiden #2EXAMPLE

Monica is Daniel’s cousin. She lived with Daniel for seven months during the tax year.If the potential dependent has a gross income, it must be less than $4,400 for 2022.

EXAMPLE

Aiden #3EXAMPLE

Tony (28) and Adam (27) are cousins and lived in the same home throughout the tax year. No one else lived in their household. Adam is not disabled. Adam only earned $2,500. Tony earned $25,000. Adam meets the Member of Household portion of the Relationship or Member of Household test for Tony since Adam lived with Tony the entire year. Adam meets the gross income requirement since his gross income is less than $4,400. Assuming that Adam meets the remaining tests, Tony may be able to claim Adam as a qualifying relative dependent.As mentioned earlier, the support test for a qualifying relative is different than for a qualifying child. Remember, the support test for a qualifying child is the child must not provide more than half of their own support. The test for a qualifying relative depends on the taxpayer providing over one-half of the support for the potential dependent to satisfy the test.

Remember, a potential dependent’s own funds are not counted as support unless they actually spent those funds on supporting themselves.

In figuring out a potential dependent’s total support, include tax-exempt income, savings, and borrowed amounts used to support that person. Tax-exempt income includes certain Social Security benefits, welfare benefits, nontaxable life insurance proceeds, Armed Forces family allotments, nontaxable pensions, and tax-exempt interest.

If a potential dependent receives Social Security benefits and uses them toward their own support, the benefits are considered as provided by the potential dependent.

EXAMPLE

Aiden #4EXAMPLE

John lives with Robert, his father. John provides 30% of Robert’s support. John may not claim Robert as a dependent, because John failed the qualifying relative support test by not providing more than 50% of Robert’s support.EXAMPLE

Gerald (69; his birthday is June 5, 1952) is single and lives with his son, Kyle (49), and Kyle’s wife, Kim (48). The fair rental value of their home, which is owned by Kyle and Kim, is $18,000. They pay $1,500 per month in rent, and the utilities cost another $4,500 for the whole year. The food cost for the family is $7,500. Entertainment expenses for Kyle and Kim were $6,000.

We will use the Definition of a Dependent chart to work through this example scenario and determine whether the potential dependent (Aubrey) is a qualifying child, qualifying relative, or not a dependent of Oliver and Hannah.

Aubrey (22) lived with both of her parents, Oliver and Hannah, for five months in 2022. She had moved out to attend college two years ago, but she dropped out of school in 2021 and moved back into her parents’ home in late July 2022. Aubrey is not permanently and totally disabled.

Aubrey worked for part of the year. She had a total gross income of $3,000 from one job and another $1,000 from a second job.

Oliver and Hannah paid all the household expenses, bought the groceries, and paid Aubrey’s outstanding rent of $3,000 from her last apartment. They spent close to $6,000 total (including paying her overdue rent) for Aubrey’s support during the year.

Aubrey spent all of her income on her entertainment and paying off her remaining unpaid bills. Aubrey’s boyfriend paid $1,500 of Aubrey’s credit card bills during the year.

We will determine if Aubrey is a qualifying child, qualifying relative, or not a dependent of her parents.

1. Passed. Oliver and Hannah are not dependents of another taxpayer.

2. Passed. Aubrey is not married and did not file a joint return.

3. Passed. Aubrey is a U.S. citizen.

4. Passed. Aubrey is Oliver and Hannah’s daughter.

5. Failed. Aubrey is under the age of 24, but not a full-time student or permanently and totally disabled.

Aubrey is not Oliver and Hannah’s qualifying child. The next step is to determine if she is their qualifying relative.

10. Passed. Aubrey is not a qualifying child of her parents or of any other taxpayer.

11. Passed. Aubrey passes the relationship requirement for Relationship or Member of Household. She does not have to live with her parents at all during the year to pass this test since she is their daughter.

12. Passed. Aubrey’s gross income is $4,000.

13. Passed. Oliver and Hannah paid over half of Aubrey’s support. They paid 52.18%.

Her total support is $11,500 ($4,000 paid by Aubrey, $6,000 paid by Oliver and Hannah, and $1,500 paid by her boyfriend). Oliver and Hannah paid 52.18%. Aubrey paid 34.78% of her support. Her boyfriend paid 13.04%. [52.18% + 34.78% + 13.04% = 100%]

Because Aubrey satisfies all of the qualifying relative requirements, she is a qualifying relative dependent of Oliver and Hannah.