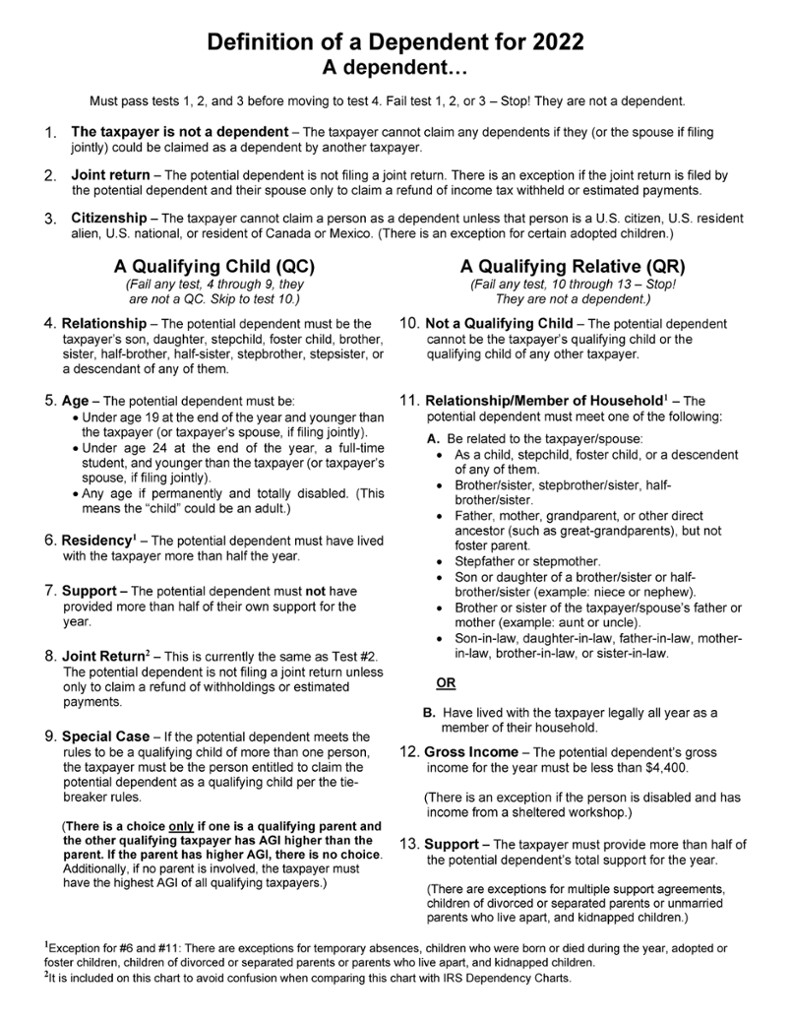

1. Qualifying Child

In the previous section, we learned the first three tests on the Definition of a Dependent illustration must be met. If any of these first tests are failed, there is no need to continue as the person is not a dependent. If all three tests are passed, then the additional dependent tests must be considered.

As mentioned earlier, a dependent is either a qualifying child (QC) or a qualifying relative (QR).

All the requirements for claiming dependency are summarized below.

2. What is a Qualifying Child?

For an individual to be a qualifying child (QC) of a taxpayer, an individual must meet five tests:

For an individual to be a qualifying child (QC) of a taxpayer, an individual must meet five tests:

- Relationship (test #4)

- Age (test #5)

- Residency (test #6)

- Support (test #7)

- Joint return (test #8)

Qualifying Child: Five Requirements

- Only certain relationships are accepted.

- Specific age requirements must be met.

- Residency requirements must be met.

- Potential dependents cannot provide more than 50% of their own support.

- Is the potential dependent filing a joint return?

2a. (4) Relationship Test

In order to satisfy the relationship test, an individual must be related to the taxpayer in one of the following ways:

- Son or daughter

- Brother or sister

- Adopted child

- Eligible foster child

- A descendant of any of these (this includes all grandchildren, nieces, and nephews)

Stepsons, stepdaughters, stepbrothers, and stepsisters all satisfy the relationship test. Half brothers, half sisters, and their descendants also meet this requirement.

Adopted children satisfy the test, even if the adoption is not yet final, provided the child has been lawfully placed for adoption with the taxpayer.

A foster child must be placed with the taxpayer by an authorized placement agency or by judgment, decree, or other order of any court of competent jurisdiction.

If the potential dependent does not pass this test, the remaining tests under qualifying child can be skipped, and the first question under qualifying relative can be considered.

Relationships for the qualifying child relationship test established by marriage are not ended by death or divorce.

-

EXAMPLE

Tim #1 Tim (23) and his brother, Dave (21), lived together all through the tax year. Tim is a full-time student and is not disabled. Dave and Tim are brothers, so the relationship test is passed. (You will see Tim again under the age test.)

-

EXAMPLE

Adam Tony (28) and Adam (27) are cousins and lived in the same home throughout the entire tax year. Adam only earned $2,500. Tony earned $25,000. Since Tony and Adam are cousins, the relationship test for a

qualified child is not passed. Adam is not a

qualifying child. The next requirement to consider is #10 under

qualifying relative.

-

EXAMPLE

Dakota #1 Dakota (10), a child actress, has a significant income and pays over half of her own support. She lives with her parents when she is not working. When she is working, she has a guardian travel with her.

Because Dakota is the daughter of her parents, she passes the relationship requirement for a

qualifying child. (You will see Dakota again under the age test.)

2b. (5) Age Test

To meet this requirement, the child must meet one of the following tests:

- Be under age 19 at the end of the year and younger than the taxpayer (or the taxpayer’s spouse, if filing jointly).

- A full-time student under age 24 at the end of the year and younger than the taxpayer (or the taxpayer’s spouse, if filing jointly). A full-time student is defined as being full-time according to the institution for any part of five calendar months during the year.

-

Permanently and totally disabled at any time during the year, regardless of age. The potential dependent does not have to be younger than the taxpayer or spouse when permanently and totally disabled.

-

For an individual who is not permanently and totally disabled to be a

qualifying child of a taxpayer or taxpayer’s spouse (if filing jointly), the individual must be younger than either the taxpayer or the taxpayer’s spouse but doesn’t have to be younger than both.

-

EXAMPLE

Tim #2 Tim (23) and his brother, Dave (21), lived together all through the tax year. Tim is a full-time student and is not disabled. Dave may not claim Tim as a

qualifying child since Dave is younger than Tim, failing the age test.

-

EXAMPLE

Paul Mike’s 23-year-old brother, Paul, who is a full-time student and unmarried, lived with Mike and Mike’s spouse all year. Paul is not disabled. Mike is 21, and his spouse is 24 years old. Because Mike’s brother, Paul, is younger than Mike’s spouse, and Mike and his spouse are filing a joint return, Paul meets the age test to be Mike’s

qualifying child.

-

EXAMPLE

Dakota #2 Dakota (10), a child actress, has a significant income and pays over half of her own support. She lives with her parents when she is not working. When she is working, she has a guardian travel with her.

Because Dakota is under the age of 19, she passes the age requirement for a

qualifying child.

If the potential dependent does not pass this test, the remaining tests under qualifying child can be skipped, and the first question under qualifying relative can be considered.

-

- Permanent and Total Disability

- A disability that prevents an individual from engaging in any substantial, gainful activity because of a medically determined physical or mental impairment expected to result in death, or that has lasted, or is expected to last, for a continuous period of not less than 12 months.

2c. (6) Residency Test

The residency test is satisfied if the individual lived with the taxpayer for more than six months of the year. An individual who was born or died during the year is considered to have met this test, regardless of how long they lived with the taxpayer, provided they lived with the taxpayer for half of the time they were alive during the tax year.

There are exceptions for children who were kidnapped or temporarily absent from the home.

Adoption/Foster Child Exception

An adopted child satisfies this test provided the child is adopted in 2022 and has been lawfully placed in the home for adoption. The taxpayer can consider the child to have lived with them for more than half of the year if the taxpayer’s main home was the child’s main home for more than half the time since the child was adopted or placed with them during the year 2022.

EXAMPLE

Lena (6) was legally placed in Ati’s (30) home on April 11, 2022. Lena lived with Ati from that time forward. Lena’s adoption was finalized on July 18, 2022.

Lena is considered to have lived with Ati for more than half of the year since her main home was with Ati from when she was legally placed with Ati on April 11 through the end of the year.

A foster child satisfies this test provided the child has been lawfully placed in the home. The taxpayer can consider the child to have lived with them for more than half of the year if the taxpayer’s main home was the child’s main home for more than half the time since the child was legally placed with them during the year 2022.

Temporary absences by the taxpayer or the child for special circumstances, such as school, vacation, business, medical care, military service, or detention in a juvenile facility, count as time the child lived with the taxpayer. Attending college is an example of a temporary absence. There are also exceptions for children of divorced, separated, or unmarried parents.

If the potential dependent does not pass this test, the remaining tests under qualifying child can be skipped, and the first question under qualifying relative can be considered.

-

EXAMPLE

Dakota #3 Dakota (10), a child actress, has a significant income and pays over half of her own support. She lives with her parents when she is not working. When she is working, she has a guardian travel with her. Due to her age, she is not away from home for more than two weeks at a time.

Because Dakota’s absences from the home are considered temporary absences, she passes the residency requirement for a

qualifying child.

2d. (7) Support Test

A potential dependent cannot have provided more than one-half of their own support during the tax year.

Payments received for the support of a foster child from a child placement agency are considered support provided by the agency. Similarly, payments received for the support of a foster child from a state or county are considered support provided by the state or county. A potential dependent’s own funds are not considered support unless they are actually spent for support. Thus, if money is put in savings and not used for support, it does not count.

-

EXAMPLE

Dakota #4 Dakota (10), a child actress, has a significant income and pays over half of her own support. She lives with her parents when she is not working. When she is working, she has a guardian travel with her. Due to her age, she is not away from home for more than two weeks at a time.

Dakota cannot be claimed as a

qualifying child because she fails the support test.

If Dakota had saved all of her income and not spent it on her support, she would have passed the support requirement for a

qualifying child.

-

The taxpayer does not have to provide over one-half of the potential dependent’s support to satisfy the support test for a

qualifying child. Rather, the

qualifying child cannot provide more than one-half of their own support. This test differs from the support test for a

qualifying relative, as you will see when discussing the

qualifying relative requirements.

If the potential dependent does not pass this test, the remaining tests under qualifying child can be skipped, and the first question under qualifying relative can be considered.

2e. (8) Joint Return Test

To meet this test, the child cannot file a joint return for the year, unless they file a joint return only to claim a refund of income tax withheld or estimated taxes paid.

-

This is the same as the #2 requirement, Joint Return. At one point the two separate requirements (#2 and #8) were slightly different but have since been made the same. The IRS still provides them as separate tests in their publications. To avoid any confusion, the

Definition of a Dependent chart also provides them in the same format.

For those who are curious, the difference was in the tax law as it was originally written; the first joint return test (#2) did not allow any exceptions. The #8 joint return test did include the exception, effectively only allowing the exception for

qualifying children. However, this difference was made obsolete by the Fostering Connections to Success and Increasing Adoptions Act of 2008 (FCSIAA).

-

- Joint Return

- A return combining the income, credits, and deductions of a married couple, resulting in a joint tax liability.

2f. (9) “Special Case”

Sometimes a child meets the relationship, age, residency, support, and joint return tests to be a qualifying child of more than one person. Although the child meets the conditions to be a qualifying child of each person, only one person can actually treat the child as a qualifying child. Both of the sections, “Tiebreaker Rules” and “Children of Divorced, Separated, or Unmarried Parents,” covered in the next chapter, will help you understand this special case test.