Table of Contents |

As in job order costing, a process costing system has production costs that include direct materials, direct labor, and overhead. Another similarity between the two systems is that they both use source documents, including materials requisitions and time tickets, to track direct materials and direct labor. Some companies might combine labor and overhead into conversion costs when they use process costing; however, when they record the labor and overhead in the general ledger, they will record them in their individual ledger accounts rather than combining them.

EXAMPLE

In this section, we will use the example of Beckie’s Beverages, a bottling company. Bottling companies like Beckie’s Beverages buy ingredients like syrup and carbonated water from distributors, which they mix (in the mixing department) and bottle (in the bottling department) into cans and bottles for commercial distribution.Accounting for direct materials in process costing is similar to accounting for direct materials when job order costing is used.

EXAMPLE

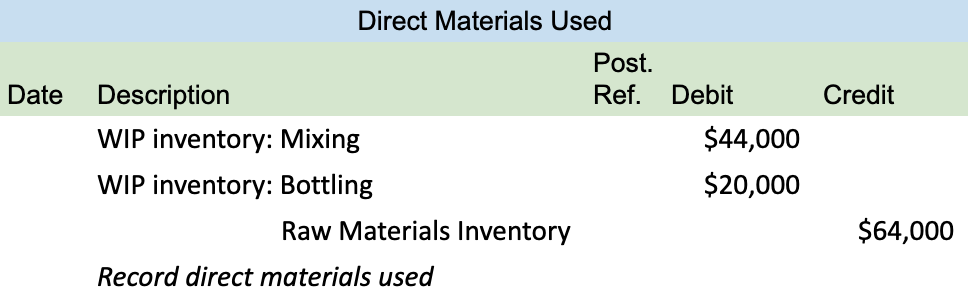

For Beckie’s Beverages, the raw materials may consist of syrup or concentrate, carbonated water, cans, and tops for the cans.The company receives the raw materials and, subsequently, records a debit to the raw materials inventory and a credit to the accounts payable to show that it acquired materials on credit. One thing to note is that the dates on the journal entries are omitted because they are summary entries, which are often used to reflect two or more transactions.

EXAMPLE

A bottling company might have a mixing department that is responsible for mixing the syrup or concentrate with the carbonated water, and it might also have a bottling department where the soda is bottled to be sold. Both of the departments will have a work-in-process (WIP) inventory that will be identified in the journal entry that is required to assign the costs of direct materials. The entry to record the use of raw materials in the production departments consists of a debit to WIP: Mixing and a debit to WIP: Bottling, with a credit to the raw materials inventory. This entry shows us the movement of raw materials into the two production departments.

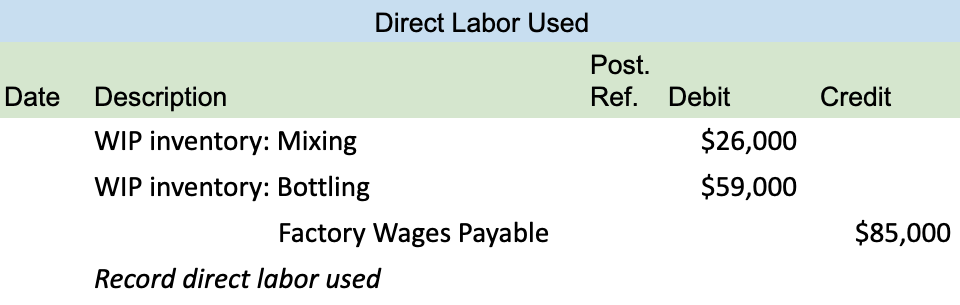

Just as with job order costing, the labor for process costing is tracked by time reports that record the employees’ hours worked, their hourly wage, and the total labor cost. For process costing, time reports are kept for each individual department, rather than for each individual job as they would be in job order costing. With process costing, the direct labor of a production department includes all labor used exclusively by that department.

EXAMPLE

Beckie’s Beverages’ production department has a full-time manager and a full-time maintenance worker. Their salaries are direct labor costs rather than overhead.

Overhead costs in the process costing system consist of indirect materials, indirect labor, and any other indirect costs that are necessary to complete the production process. As we learned previously, indirect materials are materials that are not clearly linked with a specific production process or department. These costs cannot be directly linked to the mixing or bottling departments; however, they support the overall production activity. The journal entry that is used to record the direct materials is a debit to the overhead and a credit to the raw materials inventory.

EXAMPLE

Indirect labor costs for Beckie’s Beverages may include clerical or maintenance workers that help production in both the mixing and bottling departments. These employees are responsible for labor such as ordering materials, repairing equipment, processing payroll, or cleaning the factory. The journal entry to record the indirect labor will consist of a debit to the overhead and a credit to the wages payable.Additional overhead costs outside of indirect material and indirect labor for a company that uses process costing could include prepaid insurance, utilities payable, and depreciation. When we record the overhead costs, we debit factory overhead and credit prepaid insurance, utilities payable, and depreciation.

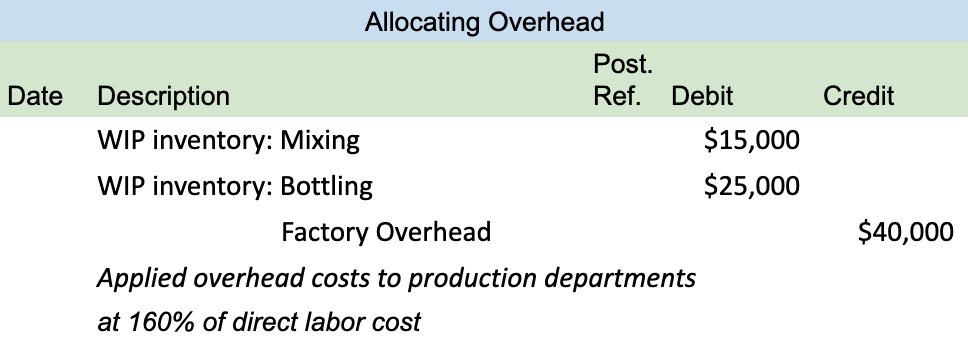

Similar to job order costing, we allocate overhead to WIP using the predetermined overhead allocation rate to estimate the overhead at the beginning of a period and allocate the overhead throughout the period. Managers are able to obtain up-to-date estimates of the costs of their processes during the period. This is important for process costing since goods are transferred across departments before the production process is complete.

Since overhead costs benefit all processes or departments within process costing, most process operation companies use a single overhead account to accumulate actual and applied overhead costs. Manufacturers that use process costing must allocate overhead to processes; therefore, it is required for them to have good allocation bases.

With process costing, we are tracking cost by the process; therefore, different processes might have different cost drivers, resulting in different allocation bases when allocating the overhead.

EXAMPLE

A mixing department might use machine-hours as their allocation base since machines provide the bulk of the work. The assembly department on the other hand might use labor hours as their allocation base since labor is primarily used in the production process.

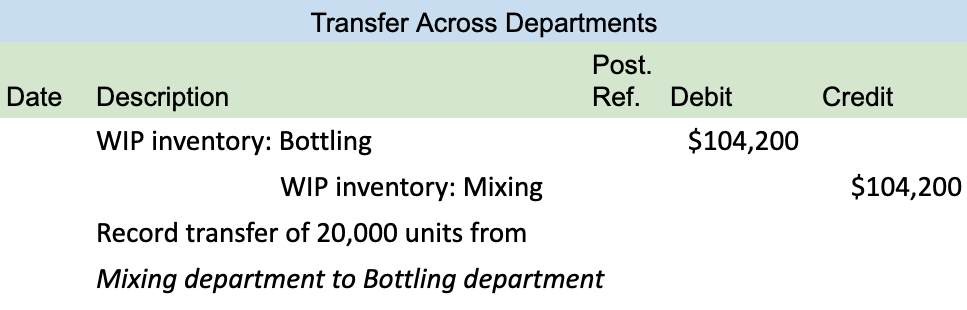

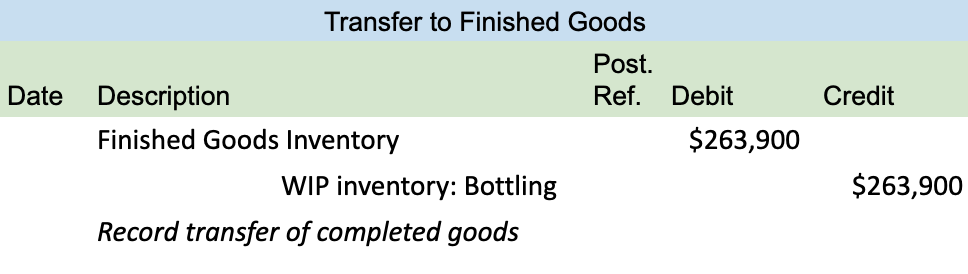

When multiple departments are used in the production process, the WIP inventory is transferred between the departments until the product is completed and transferred to the finished goods inventory.

EXAMPLE

The bottling company will start with the mixing department and transfer the WIP inventory to the bottling department. The inventory in the mixing department is partially completed; therefore, it is transferred to the next department to continue with the production process. Units and costs are transferred out of the mixing department and transferred into the bottling department.

With job order costing, managers use the schedule of the cost of goods manufactured along with job cost sheets to gather the cost information related to direct materials, direct labor, and overhead. Process costing, on the other hand, will use the production cost report to identify the direct materials, direct labor, and overhead. The production cost report shows both the flow of units and the flow of costs through a production process. It also shows how accountants divide these costs between the cost of units completed and transferred out and the cost of units still in the department’s ending inventory. This report makes the equivalent unit and unit cost computations easier. The equivalent units of production (EUP) are the number of units that could have been started and completed given the costs incurred during the period. Companies that use process costing will usually end each period with both the WIP inventory and the finished goods inventory.

EXAMPLE

Beckie’s Beverages ends each period with both completed cans of soda and partially completed cans of soda in their inventory since some of the inventory is still in the mixing stage of production. This is when managers calculate the EUP, allowing them to measure the production activity.When preparing the production cost report, the EUP for direct materials and conversion costs are calculated. Calculating the EUP for direct materials is often not the same with respect to direct labor and overhead. With direct materials, the raw materials might enter the production process at the beginning of the process, whereas direct labor and overhead might be used continuously throughout the process. We account for these timing differences by using EUP, allowing managers to effectively track costs.

As we learned in a previous lesson, the total of direct labor and factory overhead is classified as the conversion cost or the cost of converting direct materials into finished products. Companies with process operations will compute the cost per equivalent unit, consisting of a combination of direct labor and overhead per equivalent unit of production. Managers combine direct labor and overhead since they typically enter the production process at the same time.

The preparation of the production cost report includes the following four steps:

In the next lesson, we will walk through each of the steps that are used to create the production cost report and later discuss how this is used to make managerial decisions.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.