Table of Contents |

The operating activities section of the statement of cash flows focuses on inflows and outflows of cash resulting from the normal day-to-day operations of the business. This includes such things as cash received from selling products and services, paying employees and vendors, and paying for operational costs like rent, utilities, and insurance. Paying interest to creditors and taxes is also addressed within the operating activities section.

Both the U.S. Generally Accepted Accounting Principles (GAAP) and the International Financial Reporting Standards (IFRS) permit companies to use either the direct or indirect method to calculate the net cash flows from operating activities. However, the majority of accountants choose the indirect method over the direct method. Ultimately, both methods have the same purpose but take separate approaches.

The indirect method adjusts net income (rather than adjusting individual items in the income statement) for changes in current assets and current liabilities, as well as items that were included in net income but did not affect cash. The most common example of an operating expense that does not affect cash is depreciation expense, which is a measurement of how much an asset has lost value over a time period.

If a company chooses to use the direct method for external reporting, they are required to provide an additional report that uses the indirect method, but companies that use the indirect method are not required to supplement their reporting using the direct method.

IN CONTEXT

Excerpt from the Financial Accounting Standards Board (FASB), Statement of Financial Accounting Standards No. 95

- This Statement requires that a statement of cash flows reports the reporting currency equivalent of foreign currency cash flows, using the current exchange rate at the time of the cash flows. The effect of exchange rate changes on cash held in foreign currencies is reported as a separate item in the reconciliation of beginning and ending balances of cash and cash equivalents.

- This Statement requires that information about investing and financing activities not resulting in cash receipts or payments in the period be provided separately.

- This Statement is effective for annual financial statements for fiscal years ending after July 15, 1988. Restatement of financial statements for earlier years provided for comparative purposes is encouraged but not required.

We will utilize a three step process to adjust the net income provided on the income statement to the net cash provided by the operating activities.

Let’s look at each of these steps in more detail.

Depreciation and amortization are noncash expenses. Since the indirect method requires us to adjust net income for all of the changes to noncash accounts on the balance sheet, depreciation and amortization expenses must be added back since these are the amounts that would have increased the accumulated depreciation or amortization accounts on the balance sheet.

Noncurrent assets are assets that a company holds long term with the expectation that they will generate income; this includes fixed assets like property and equipment as well as intangible assets like copyrights and patents. The proceeds from the sale of noncurrent assets are included as a cash inflow in the investing activity section. Proceeds are cash received from the sale of a noncurrent asset. However, gains or losses must be adjusted from net income. Gains are the result of when proceeds received from the sale of an asset exceed the book value, and losses are the result of the proceeds of an asset’s sale being less than the book value.

There are a few different rules for indicating the balance of current assets and liabilities, depending on their increase or decrease:

| If account balance has increased | If account balance has decreased | |

| Current Assets: | ||

| Inventory |

|

|

| Accounts receivable |

|

|

| Prepaid expenses |

|

|

| Current Liabilities: | ||

| Accounts payable |

|

|

| Accrued expenses payable |

|

|

| Income taxes payable |

|

|

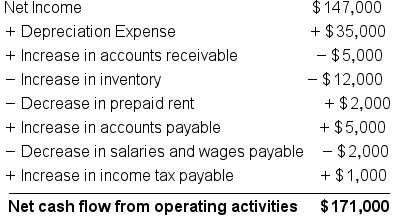

We will use Allentown Hydraulics Inc. as our example for preparing the operating activities section of the statement of cash flows. Allentown Hydraulics Inc. is a midsized producer of hydraulic parts used in many industries and has customers all over the world. We will notice that the net cash flows from operating activities end up being the same for both the direct and indirect methods. However, the path taken to the end result is quite different.

EXAMPLE

The most recent income statement for 2022 and a comparative balance sheet for 2022 and 2021 are used to demonstrate the process for preparing the operating activities section of the statement of cash flows using the indirect method.

We will now walk through the steps with the information from these statements.

Step One: Add noncash expenses back to the net income.

Net income is increased by the amount of depreciation expense listed on the income statement.

EXAMPLE

Depreciation is the only noncash expense for Allentown. We add the noncash expense of depreciation back to the net income:

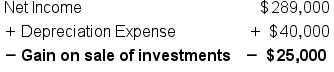

Step Two: Adjust for any gains and losses from the sale of noncurrent assets.

EXAMPLE

In the other income section of Allentown’s income statement, we can see that there is a gain in the sale of investments reported. We adjust by subtracting the gain on the sale of investments.

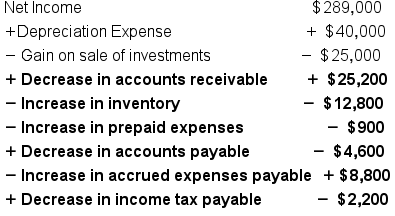

Step Three: Adjust for any changes to all other noncash current assets and liability accounts.

EXAMPLE

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.