Using the direct method to compute the cash provided by operating activities requires us to rebuild the income statement. We start with sales and then make adjustments as we work our way down the income statement. Sales are adjusted for the changes in accounts receivable and expenses are adjusted to reflect the cash that was actually paid. The income statement is essentially converted to a cash basis, which records revenue and expenses when cash is exchanged, not when revenue is earned. The income statement is typically presented on an accrual basis, which recognizes revenue and expenses when they are generated, not when the cash is exchanged. Companies using the accrual basis of accounting record revenue when they have met their obligations by providing a good or service, not when cash is collected. Subsequently, expenses are recorded in the same period as related revenues are recognized as opposed to when the bill is actually paid.

The direct method uses a top-down approach in regard to the income statement to calculate the cash provided by operating activities.

To make this calculation easier, we use the following process.

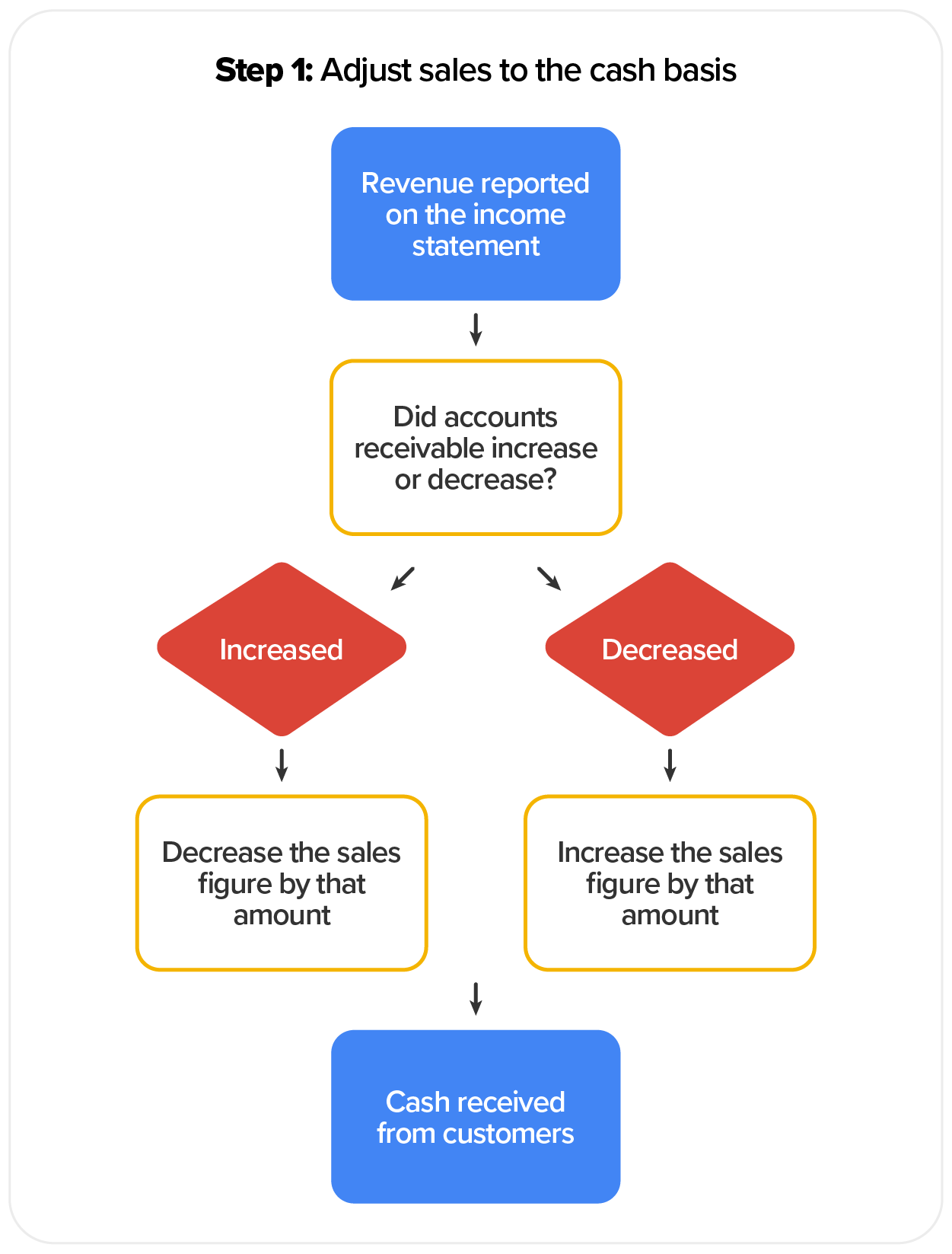

Begin with the revenue that was reported on the income statement. Total revenue will be adjusted for the increase or decrease of accounts receivable during the period. The change in accounts receivable balances will be found on the balance sheet.

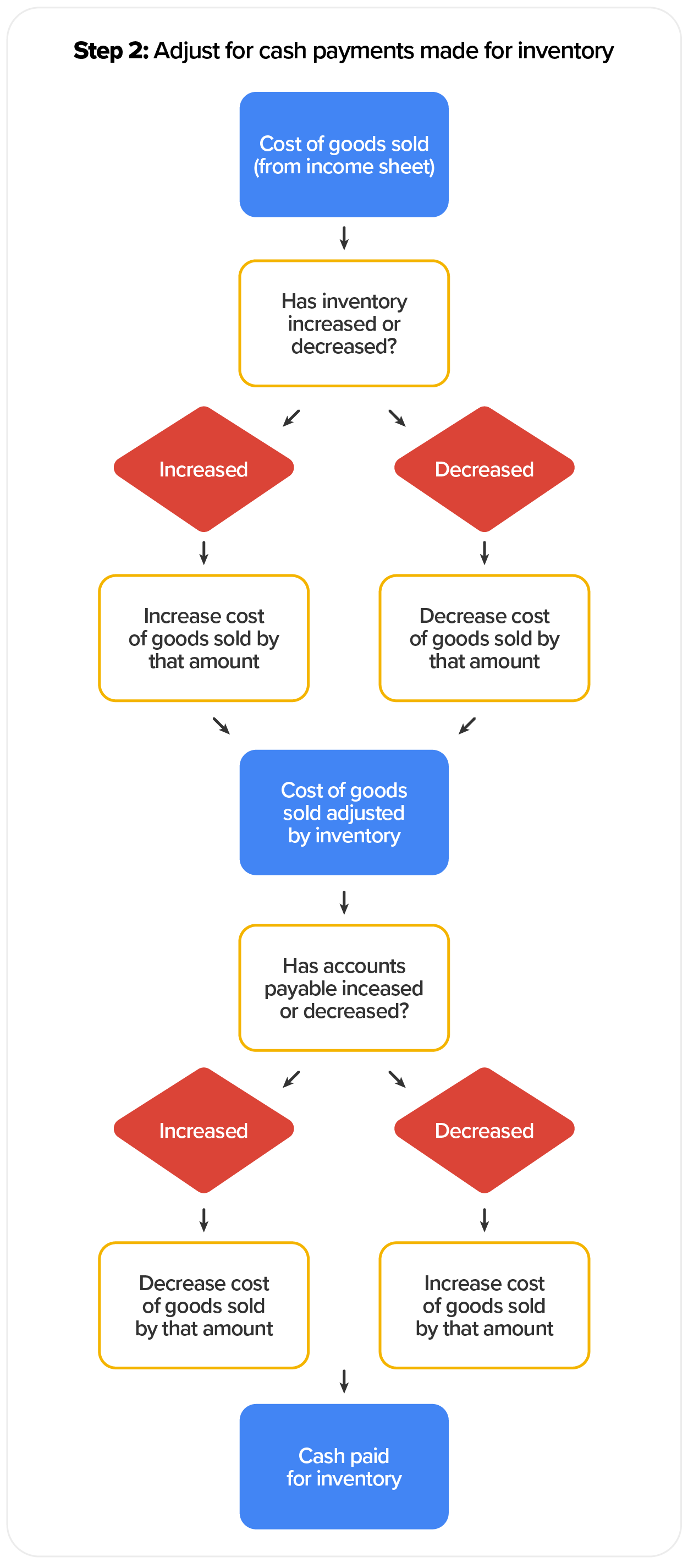

Begin with the cost of goods sold figure that was reported on the income statement. The cost of goods sold will be adjusted for the increase or decrease in inventory and accounts payable during the period. The change in inventory and accounts payable balances will be found on the balance sheet.

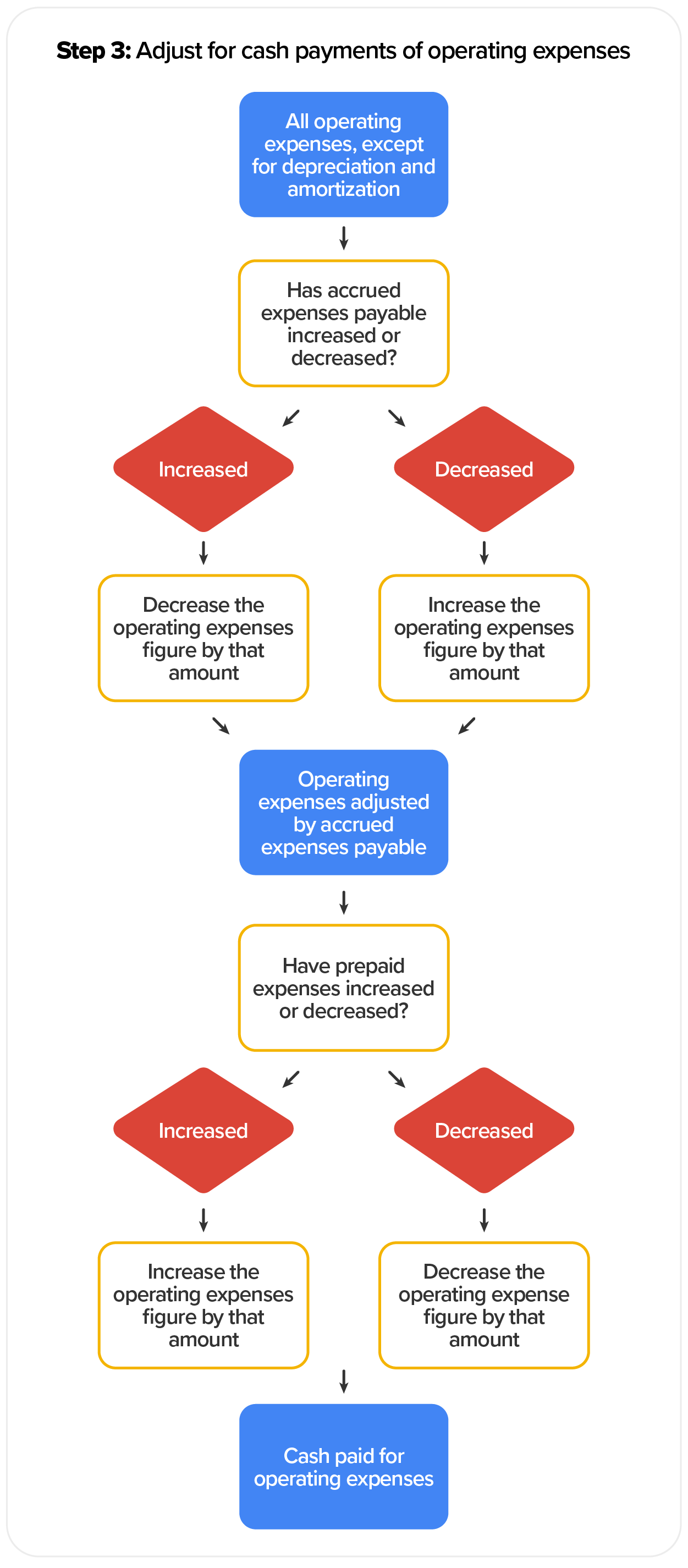

Begin with all operating expenses, except depreciation and amortization expenses which were reported on the income statement. Depreciation and amortization expenses are not adjusted for or reported on the statement of cash flows because they do not involve a cash outflow. The operating expenses will be adjusted for the increase or decrease in accrued expenses payable and the increase or decrease in prepaid expenses during the period. The change in accrued expenses payable and prepaid expense balances will be found on the balance sheet.

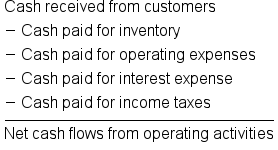

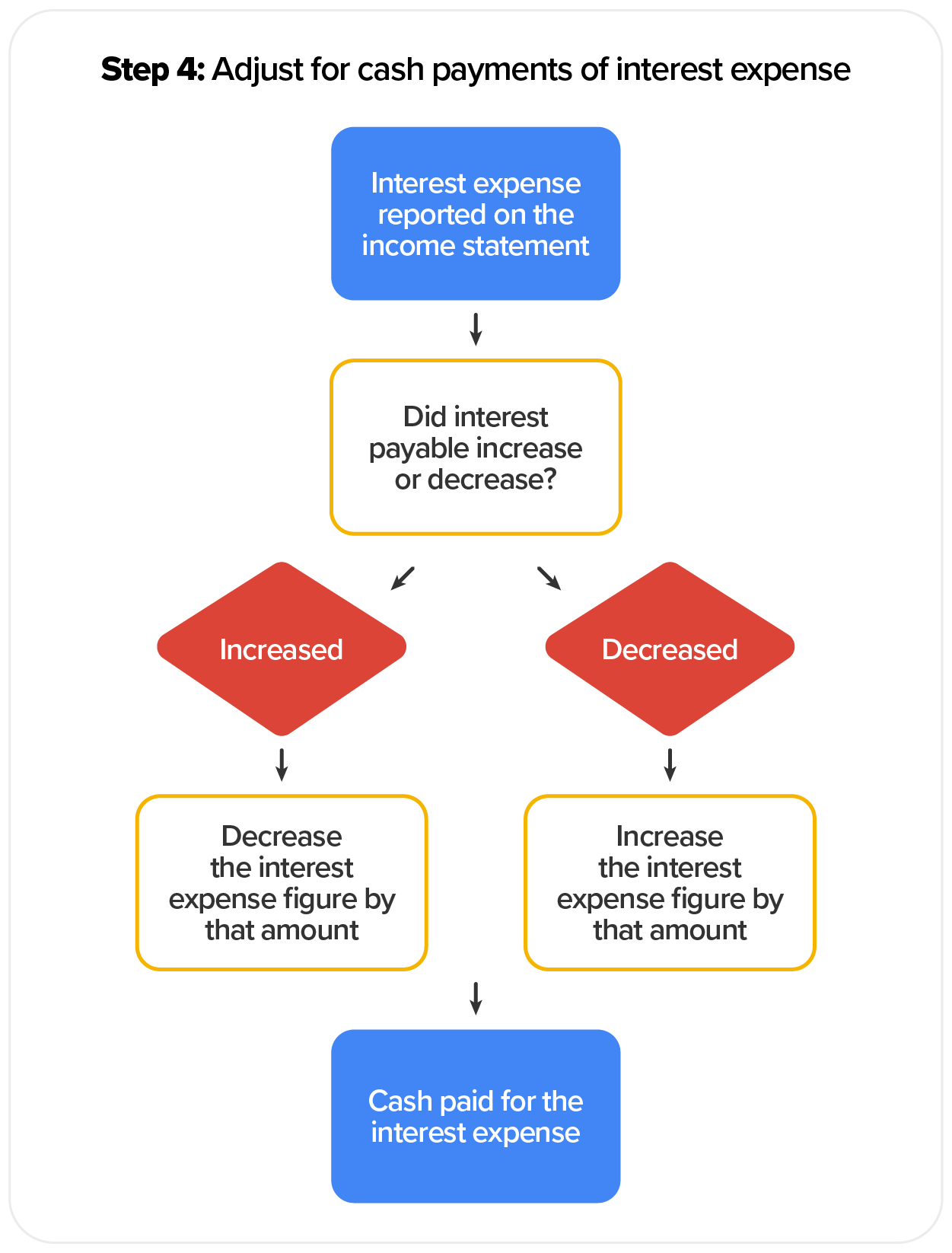

Begin with the interest expense that was reported on the income statement. The interest expense will be adjusted for the increase or decrease in interest payable during the period. The change in interest payable balances will be found on the balance sheet.

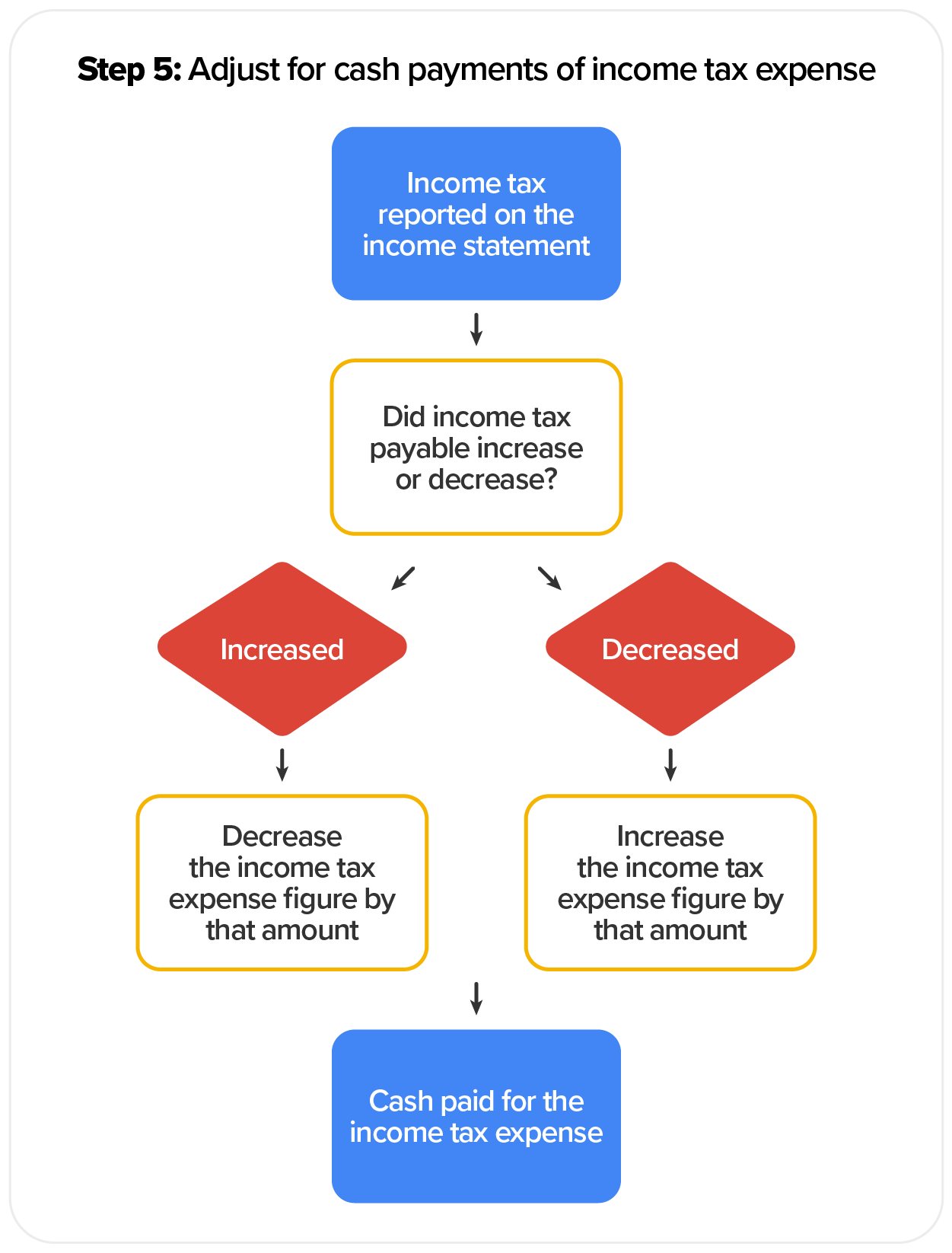

Begin with the income tax expense that was reported on the income statement. The income tax expense will be adjusted for the increase or decrease in income tax payable during the period. The change in income tax payable balances will be found on the balance sheet.

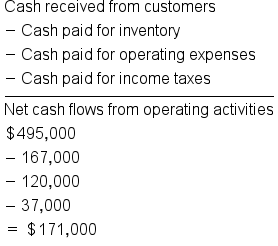

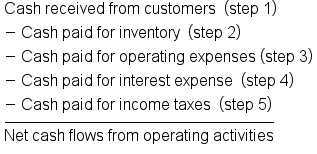

Finally, we can now put together the results of each of these steps to find the net cash flows from operating activities.

Allentown Hydraulics Inc. is a midsized producer of hydraulic parts used in many industries and has customers all over the world. We will use their most recent income statement for 2022 and a comparative balance sheet for 2022 and 2021 to demonstrate the process for preparing the operating activities section of the statement of cash flows using the direct method.

EXAMPLE

First, let’s take a look at Allentown Hydraulics’s income statement for 2022.

Now, we will walk through the steps of the direct method using the information from the Allentown income statement and balance sheet.

EXAMPLE

Cash received from customers = Revenues + decrease in accounts receivableEXAMPLE

Cash paid for inventory = Cost of goods sold + decrease in accounts payable + increase in inventoryEXAMPLE

Cash paid for operating expenses = Selling and administrative expenses + other operating expenses + increase in prepaid expenses – increase in accrued expenses payableEXAMPLE

Cash paid for interest expense = Interest expense (There is currently no interest payable on the balance sheetEXAMPLE

Cash paid for income tax expense = Income tax expense + decrease in income tax payable

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.