In this lesson, you will learn about the importance of understanding your plan coverage and how to maximize health savings and flexible spending accounts. Specifically, this lesson will cover the following:

1. Understand Your Plan Coverage

-

You’re sitting in a doctor’s office, feeling unwell, and the receptionist asks about your insurance coverage. You hesitate—do you really know what’s covered, what your co-pay is, or if you need prior approval for this visit? Suddenly, you’re scrambling through your phone, trying to find details about your plan. This kind of uncertainty can be stressful, especially when you’re already dealing with a health concern. But the good news? You can avoid this situation entirely by taking the time to understand your health insurance coverage before you need it.

Health insurance can feel overwhelming with all its terms, conditions, and fine print, but knowing the basics of your plan can save you from surprise medical bills and ensure you get the care you need without financial stress. The key document to review is your Summary of Benefits and Coverage (SBC)—a simple breakdown of what’s included in your plan. Here’s what you should focus on:

-

Covered Services: Does your plan include routine doctor visits, mental health care, prescriptions, hospital stays, or preventive care? Some services may only be covered under specific circumstances.

-

Cost-Sharing Details: Understand your deductible (the amount you pay before insurance kicks in), co-payments (fixed amounts for services like doctor visits), coinsurance (your percentage of costs after the deductible is met), and out-of-pocket maximums (the most you’ll have to pay in a year before insurance covers 100% of the costs).

- Network Providers: Seeing an out-of-network doctor can be significantly more expensive than staying within your insurance network. Check your plan’s directory to confirm which providers are covered.

- Referral and Pre-authorization Requirements: Some plans require a referral from your primary care doctor before you see a specialist or get certain tests and procedures. Not following these rules could mean denied claims and unexpected expenses.

-

Prescription Drug Coverage: Medications are covered under different tiers, with some being more affordable than others. Always check your plan’s formulary (drug list) before filling in a prescription to avoid costly surprises.

-

EXAMPLE

Sonora, a 32-year-old freelancer, learned this the hard way. She was prescribed a new medication and went to the pharmacy expecting a reasonable co-pay. Instead, she was hit with a $300 charge because her plan didn’t cover that specific drug. Had she reviewed her plan’s prescription coverage ahead of time, she could have asked her doctor for a covered alternative—potentially saving hundreds of dollars.

-

Take a few minutes to review your SBC or call your insurance provider for clarification regarding anything that seems unclear. Knowing what your plan covers before you need medical care can save you money, reduce stress, and help you make informed decisions about your health.

Now that you know your health plan coverage, let’s look at how utilizing your coverage can help you save money on preventive services and telehealth benefits.

-

- Summary of Benefits and Coverage (SBC)

- A document from your health insurance provider that explains what your plan covers, what it costs, and its key benefits in a simple format.

- Covered Services

- Medical treatments, procedures, and health-care services that your insurance plan pays for, either fully or partially.

- Cost-Sharing

- The portion of health-care costs you’re responsible for paying, including deductibles, co-pays, and coinsurance.

- Prescription Drug Coverage

- The part of your health insurance that helps pay for medications, including specifying which drugs are covered and how much you’ll have to pay.

- Formulary (Drug List)

- A list of prescription drugs covered by your insurance plan, categorized by cost and coverage level.

1a. Preventive Services

Many people only think about their health insurance when they need medical treatment, but most health insurance plans cover preventive care coverage at no extra cost if you visit an in-network provider.

Preventive care isn’t just about catching small problems early—it’s about avoiding serious, costly medical issues down the road. By taking advantage of these free services, you are investing in your long-term health and potentially preventing conditions that could impact your quality of life.

What Does Preventive Care Cover?

Most insurance plans provide full coverage for a variety of preventive health services, including the following:

- Annual Checkups: Routine wellness exams to assess your overall health

- Vaccinations: Flu shots, COVID-19 vaccines, and other immunizations to help prevent illness

- Screenings: Tests for blood pressure, cholesterol, diabetes, and certain types of cancer, such as colonoscopies or mammograms

- Women’s Health Services: Mammograms, Pap smears, birth control counseling, and prenatal care

These services are completely free as long as you visit a provider within your insurance network. Skipping preventive care can lead to undiagnosed conditions that become more serious over time.

-

EXAMPLE

Mark, a 45-year-old father of two, never scheduled his annual wellness exam because he assumed he was healthy. When he finally went for a checkup, his doctor detected high blood pressure early. With simple lifestyle changes and monitoring, he was able to get his health back on track before it became a major issue.

-

Schedule your preventive visits early in the year so you do not forget to use these free services. Taking care of your health now can prevent bigger problems later.

-

- Preventive Care Coverage

- Health services like checkups, screenings, and vaccines that are fully covered by insurance to help prevent illness and detect health issues early.

1b. Telehealth

Life is busy, and finding time to see a doctor can feel like a hassle. Between work, family, and everyday responsibilities, making an appointment, sitting in a waiting room, and taking time off aren’t always realistic options. That’s where telehealth comes in—allowing you to connect with a doctor, therapist, or specialist from the comfort of your home.

Many health insurance plans now cover telehealth visits for little to no cost, making it an easy and affordable way to get care without extra effort.

Why Telehealth Is a Game Changer

- Save Time: No need to drive across town, sit in traffic, or spend hours in a waiting room. You can have a doctor visit during your lunch break or after the kids go to bed.

- Cut Costs: Many insurance plans offer lower co-pays for telehealth than in-person visits. Some even cover them completely.

- Get Help When You Need It: Whether it’s a lingering cough, a skin rash, or a prescription refill, telehealth lets you talk to a doctor fast—often within minutes.

- Have Access to Mental Health Support: Finding a good therapist can be tough, but telehealth makes it easier to connect with licensed professionals from any place for therapy or counseling sessions.

- Have Better Access to Specialists: Need to see a dermatologist or a nutritionist? Telehealth gives you access to specialists without long wait times or unnecessary referrals.

-

Check your health insurance provider’s website or app to see what telehealth services are included in your plan. Many insurers partner with platforms where you can schedule virtual visits with doctors and therapists directly.

Next time you need nonemergency care, try a virtual visit first. It’s a simple way to maximize your health insurance benefits, save money, and get the care you need—on your schedule.

Telehealth makes accessing medical care easier and more affordable, but sometimes, in-person visits and medical bills are unavoidable. The good news? You don’t have to accept every bill at face value. Up next, we’ll cover how to review your medical bills, spot errors, and negotiate for lower costs or payment plans—helping you keep more money in your pocket while getting the care you need.

-

- Telehealth

- Virtual health-care visits with doctors, therapists, or specialists through phone or video, allowing you to get medical care from any place.

1c. Medical Bills

Getting a medical bill in the mail can be overwhelming, especially if it’s higher than expected. But here’s something most people don’t realize—you don’t have to accept the first bill you get as the final amount. Many health-care providers are open to negotiations, discounts, and payment plans to help make medical bills more manageable.

If you’re facing a high medical bill, don’t ignore it—take action instead. Here’s how you can advocate for yourself and lower your costs.

Steps to Lower Your Medical Bills:

- Check for Errors: Medical billing mistakes are common. Review your bill carefully and compare it to your insurance’s explanation of benefits (EOB). Look for duplicate charges, incorrect billing codes, or services you didn’t receive. If something looks off, call the billing department to ask for a correction.

- Ask for an Itemized Bill: Instead of a lump sum, request a detailed breakdown of charges. This can help you spot overcharges or unnecessary fees.

- Negotiate the Cost: Many hospitals and doctors offer self-pay discounts or financial assistance programs, especially if you’re uninsured or underinsured. Even if you have insurance, ask if they can lower the bill or offer a discount for paying in full.

- Set Up a Payment Plan: If you can’t pay the full amount, ask about interest-free payment plans. Most health-care providers would rather set up small monthly payments than send your bill to collections.

- Check for Charity Care Programs: Many hospitals have programs that reduce or eliminate medical bills based on income. It never hurts to ask if you qualify.

-

If you’re calling your provider to negotiate, here’s a simple script:

“Hi, I recently received my medical bill, and I’d like to go over the charges. Is there a way to reduce the cost, or do you offer financial assistance or payment plans?”

Be polite but persistent. If the first person you talk to can’t help, ask to speak with someone in the billing or financial assistance department.

Never assume that a medical bill is set in stone. Always ask about discounts, payment plans, or financial aid. A simple phone call could save you hundreds or even thousands of dollars on your medical expenses.

Negotiating medical bills helps, but health savings accounts and flexible spending accounts let you save money up front. These tax-free accounts cover health-care costs and reduce expenses. Up next, we’ll break down how they work and which one is right for you.

-

- Self-Pay Discounts

- Reduced medical costs offered to patients who pay out of pocket instead of using insurance.

- Charity Care Programs

- Hospital or clinic programs that provide free or discounted medical services based on financial need.

2. Health Savings and Flexible Spending Accounts

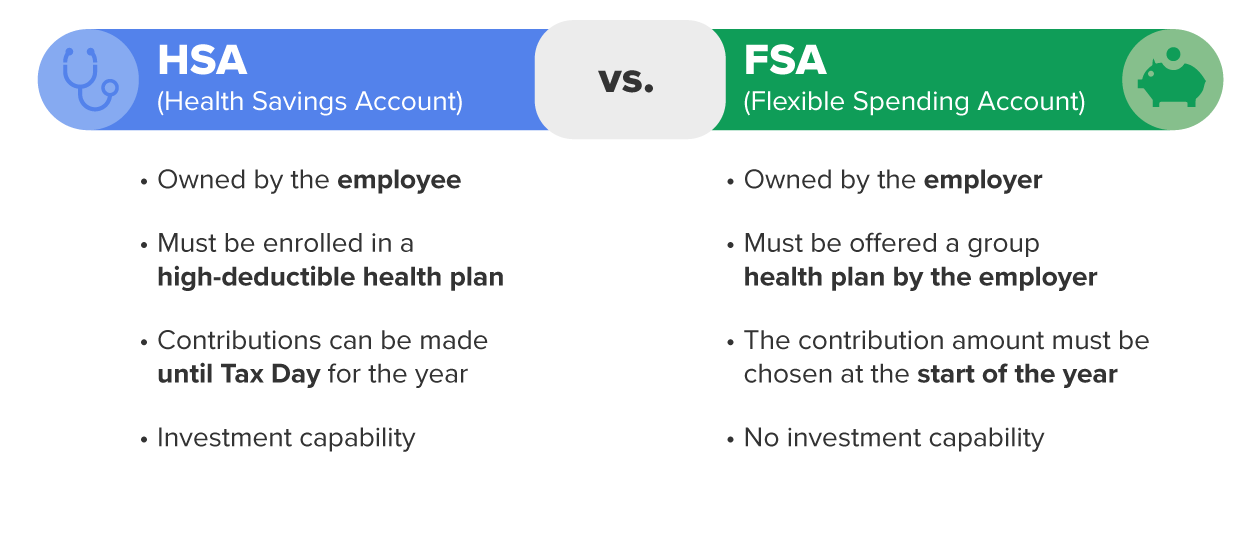

Saving money on health-care costs doesn’t have to be complicated—if you have the right tools. Health savings accounts (HSAs) and flexible spending accounts (FSAs) are two powerful ways to set aside pretax money for medical expenses, but they work a little differently.

If you’ve ever been hit with an unexpected medical bill or wished you had extra cash for health-care expenses, these accounts can help you maximize your health insurance benefits and keep more money in your pocket.

Both HSAs and FSAs let you use pretax dollars to pay for medical expenses, meaning you’re spending money before taxes are taken out of your paycheck—which saves you money. However, they have key differences in who qualifies, how funds roll over, and what you can use them for.

The Main Differences Between HSAs and FSAs

|

Feature

|

Health Savings Account (HSA)

|

Flexible Spending Account (FSA)

|

|

Who Qualifies?

|

Only people with a high-deductible health plan

|

Anyone whose employer offers an FSA (not tied to a specific health plan)

|

|

Who Owns It?

|

You

|

Your employer

|

|

Does the Money Roll Over?

|

Yes, you keep your money year after year

|

Usually, no—most FSAs have a “use it or lose it” rule at the end of the year (some allow a small rollover or grace period)

|

|

Contribution Limits (2024)

|

$4,150 for individuals, $8,300 for families *

*These change each year.

|

$3,200 per year

|

|

Can You Change Contributions?

|

Yes, any time

|

No, only during open enrollment or with a qualifying life event

|

|

Can It Be Used for Retirement?

|

Yes, after the age of 65, you can withdraw HSA funds for any reason (taxed like a 401k)

|

No, FSAs do not carry over past your employment

|

|

What Can You Spend It On?

|

Doctor visits, prescriptions, vision/dental appointments, medical supplies, and even some over-the-counter medications

|

Similar to an HSA, but more restrictions on nonprescription items

|

How These Accounts Help You Save Money:

1. Reduce Your Taxes

Since contributions to HSAs and FSAs are made before taxes, you lower your taxable income, meaning that you keep more of your paycheck. If you’re in the 22% tax bracket and contribute $3,000 to an HSA, you effectively save $660 in taxes just by using the account.

2. Make Health Care More Affordable

Both accounts allow you to pay for medical expenses with pretax dollars, making routine expenses like prescriptions, co-pays, or even eyeglasses cheaper than if you paid out of pocket.

3. Prepare for Unexpected Medical Costs

Instead of scrambling to cover a big medical bill, having money set aside in an HSA or FSA gives you a built-in emergency fund for health-care expenses.

4. Maximize Your Health Insurance Benefits

- With an HSA, you can invest the money and grow it tax-free over time, which can help cover major health-care costs later in life.

- With an FSA, you can plan ahead and use pretax money for things like dental work, prescription glasses, or physical therapy sessions.

Which One Should You Choose?

- If you have a high-deductible health plan (HDHP) and want a flexible, long-term savings option, an HSA is your best bet. You can keep the money year after year and even use it in retirement.

- If you have a standard health plan through work and want to set aside money for routine medical expenses, an FSA works well—as long as you’re okay with the “use it or lose it” rule.

-

EXAMPLE

Meet Malik and Jasmine. They both want to save money on health-care expenses but have different health insurance plans, so they each use a different type of account.

Malik’s HSA Story

Malik is self-employed and has an HDHP. Since his plan doesn’t cover much until he meets a high deductible, he opens an HSA to help with medical costs.

- He contributes $3,000 to his HSA this year, which lowers his taxable income, saving him money on taxes.

- He uses $500 from his HSA to cover a surprise ER visit after a basketball injury. Since he paid with pretax dollars, he saved money compared to what he would have had to pay out of pocket.

- The rest of his HSA money stays in his account and rolls over into the next year, growing tax-free.

- In a few years, Malik plans to use his HSA funds for LASIK surgery—a qualified medical expense.

Jasmine’s FSA Story

Jasmine works a 9-to-5 job with a traditional health insurance plan provided by her employer. Since she wants to save money on health-care expenses, she signs up for an FSA during open enrollment.

- She estimates she’ll spend about $1,500 on health care this year and contributes that amount to her FSA.

- Throughout the year, she uses her FSA to pay for co-pays, prescription medications, and new glasses—all with tax-free money.

- By December, she still has $200 left in her FSA, so she books a dental cleaning and buys over-the-counter medicines before the money expires.

- Because FSAs usually have a “use it or lose it” rule, she makes sure to spend all her funds before the year ends.

The Key Difference in Their Stories

- Malik’s HSA is more flexible—his money rolls over and can even be invested in the future.

- Jasmine’s FSA is great for covering expenses now, but she has to use the money within the year or risk losing it.

-

If you have access to an HSA or FSA, make sure you’re using it to pay for eligible medical expenses. Visit

The Complete HSA Eligibility List to see a list of eligible medical expenses for an HSA and

The Complete FSA Eligibility List to see a list of eligible medical expenses for an FSA.

Every dollar you put in is tax-free, helping you save money while covering health-care costs more efficiently. If you have an FSA, be sure to spend the money before the year ends to avoid losing any unused funds.

-

- Flexible Spending Account (FSA)

- A tax-free account offered by employers to help pay for medical expenses; the money must be used within the year.

- Health Savings Account (HSA)

- A tax-free savings account for medical expenses available to those with high-deductible health plans; the money rolls over yearly.

In this lesson, you figured out how to understand your plan coverage, including how to maximize preventive services and telehealth. You also learned how to understand your medical bills and access low-cost payment programs. Lastly, you dove deep into the benefits of health savings and flexible spending accounts.