Table of Contents |

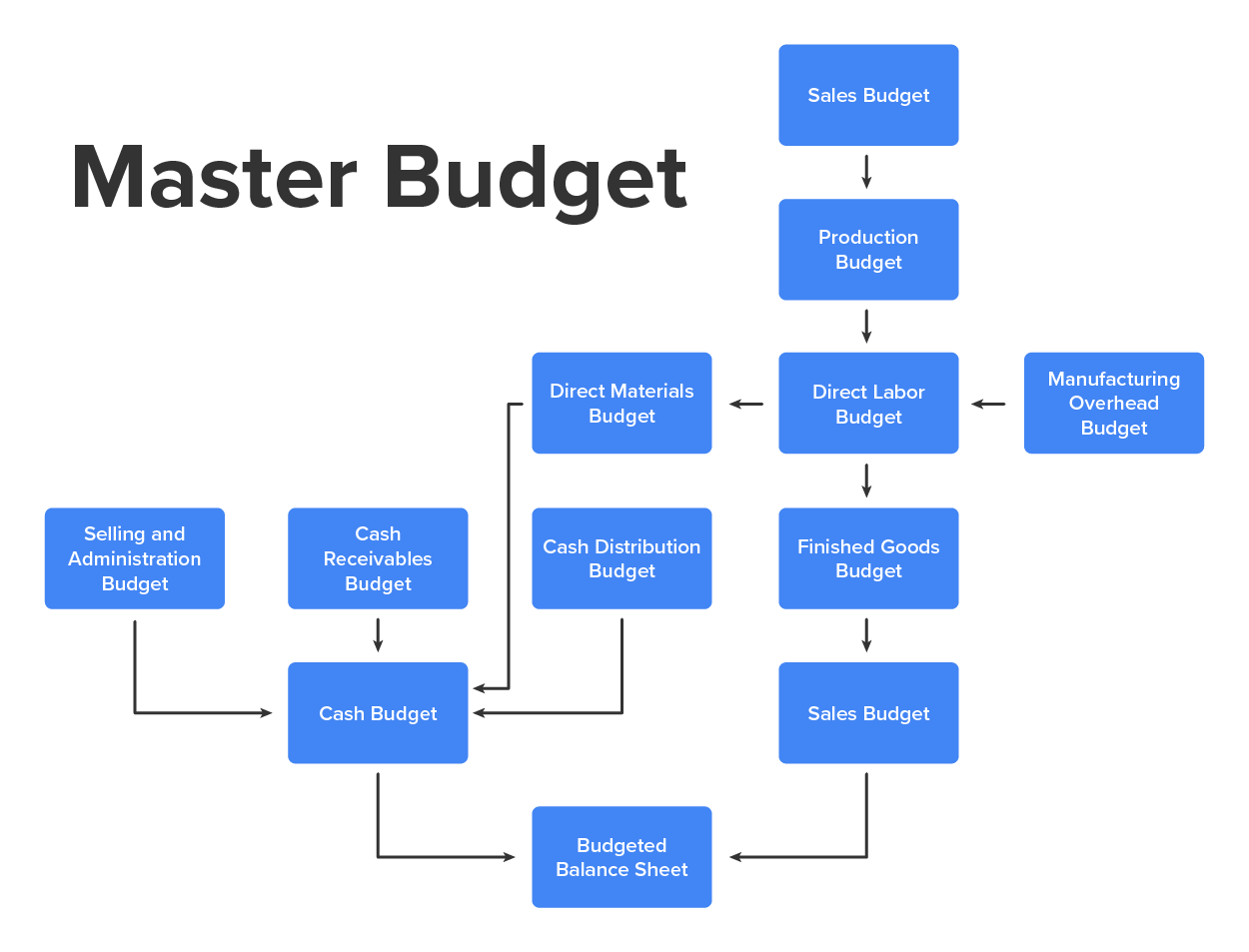

A master budget consists of both operating and financial budgets that show the organization’s objectives and proposed ways of attaining them. In the following diagram, we depict a flowchart of the financial planning process that you can use as an overview of the elements in a master budget.

The budgeting process starts with the management’s plans and objectives for the next period. These plans take into consideration various policy decisions concerning selling price, distribution network, advertising expenditures, and environmental influences from which the company forecasts its sales for the period (in units by product or product line). Managers arrive at the sales budget, which provides the projected number of units sold and sales dollars for the period. They use expected production, sales volume, and inventory policy to project the cost of goods sold. Next, managers project operating expenses such as selling and administrative expenses.

The following sections provide an overview of a budgeting procedure that many successful companies have used. We begin by preparing our sales budget, which then determines the production schedule and budget. The production budget determines the number of units that need to be produced to satisfy the projected sales by taking into account the units in the sales budget and the company’s inventory policy. Then we expand the production budget to detail the amount of direct materials, direct labor, and manufacturing overhead necessary to meet the company’s production needs.

The direct materials budget outlines the amount of direct materials that will need to be purchased to support production. Estimates are also made for the required direct labor and manufacturing overhead necessary to meet the production volume. The direct materials, direct labor, and manufacturing overhead budget provide the information to form the finished goods budget, which provides a unit product cost as well as finished goods inventory.

The next budget schedule summarizes our selling and administrative expenses. Along with the sales, production, direct materials, direct labor, manufacturing overhead, and finished goods budgets, this will make up our operating budgets and help us to form a budgeted income statement,

Our last group of budget schedules includes financial budgets. This includes our cash receivables budget, which outlines the expected amount and timing of cash to be received from customers. We will also build a cash disbursements budget, which will allow us to form a detailed cash budget that will act as an input to our budgeted balance sheet.

As our basis for planning and the source of our beginning balances, we will use the balance sheet from the end of the previous period. The ending balance sheet from the previous period acts as the beginning balance sheet for the new period to be budgeted and provides necessary information for many of the subsequent budget schedules.

EXAMPLE

For our example in this lesson, we will use MoTown Racing Tires, Inc., which provides tires to many auto racing associations and their participants. The balance sheet dated December 31, 2021, provides beginning balances for cash, receivables, and inventory, which will be used to determine the upcoming period’s budget.

The sales budget is the cornerstone of the budgeting process because the usefulness of the entire operating budget depends on it. The sales budget involves estimating or forecasting how much demand exists for a company’s goods and then determining if a realistic, attainable profit can be achieved based on this demand. Sales forecasting can involve either formal or informal techniques or both.

Formal sales forecasting techniques often involve the use of statistical tools. For example, to predict sales for the upcoming period, management may use economic indicators (or variables) such as the gross national product or gross national personal income, and other variables such as population growth, per capita income, new construction, and population migration.

To use economic indicators to forecast sales, a relationship must exist between the indicators (called independent variables) and the sales that are being forecast (called the dependent variable). Then management can use statistical techniques to predict sales based on economic indicators.

Management often supplements formal techniques with informal sales forecasting techniques such as intuition or judgment. In some instances, management modifies sales projections using formal techniques based on other changes in the environment. Examples include the effect on sales of any changes in the expected level of advertising expenditures, the entry of new competitors, and/or the addition or elimination of products or sales territories. In other instances, companies do not use any formal techniques. Instead, sales managers and salespersons estimate how much they can sell. Managers then add up the estimates to arrive at the total estimated sales for the period.

Usually, the sales manager is responsible for the sales budget and prepares it in units and then in dollars by multiplying the units by their selling price. The sales budget in units is the basis of the remaining budgets that support the operating budget.

EXAMPLE

We can see projected sales in units and sales dollars for MoTown Racing Tires here within the sales budget. Management projected the upcoming period’s sales broken into four quarters. Using previous periods’ sales, economic indicators, and their own intuition, the management team at MoTown is predicting that they will sell 8,000 tires during the first quarter, 14,000 in the second quarter, 10,000 in the third quarter, and 4,000 in the fourth quarter. The estimated selling price is $125 per tire; therefore, it has been projected that a total of 36,000 tires will be sold during the upcoming period for a total of $4,500,000 (36,000 tires x $125).

The production budget considers the units in the sales budget and the company’s inventory policy. Managers develop the production budget in units and then in dollars. Determining production volume is an important task. Companies should schedule production carefully to maintain certain minimum quantities of inventory while avoiding excessive inventory accumulation. The principal objective of the production budget is to coordinate the production and sale of goods in terms of time and quantity. In general, maintaining high inventory levels allows for more flexibility in coordinating purchases, sales, and production. However, businesses must compare the convenience of carrying inventory with the cost of carrying inventory; for example, they must consider storage costs and the opportunity cost of funds tied up in inventory.

The first line of the production budget is the budgeted sales in units, which are copied directly from the sales budget.

Next, we will determine our desired ending inventory for each quarter. It is important to determine an adequate amount of inventory to begin the next period with so that there are already enough completed products on hand to begin selling. The figure for the year is equal to the ending desired inventory for the fourth quarter.

EXAMPLE

We will build out the production budget for MoTown Racing. MoTown has decided that the desired ending inventory should be equal to 25% of the following quarter’s sales.

The total units needed represent the number of completed products that is required to meet our projected sales and provide us with the desired ending inventory. This is calculated by adding the budgeted sales for the quarter to the desired ending inventory. The total units needed for the year figure is equal to the budgeted sales for the year plus the desired ending inventory for the year. The figure used for the total year for the estimated beginning inventory is equal to the estimated beginning inventory for the first quarter.

EXAMPLE

Estimated beginning inventory:

The units of production needed are the number of new units the company must produce during the given period. This is calculated by subtracting the estimated beginning inventory from the total units needed. The figure for the units of production needed for the year is equal to the total units needed for the year minus the estimated beginning inventory for the year.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.