Table of Contents |

A cost can be classified by how it changes with fluctuations in the volume of activity. These costs are either classified as fixed costs or variable costs. Fixed costs are costs that do not change with increases or decreases in the number of goods produced or services provided, and remain constant. Variable costs, on the other hand, change with increases or decreases in the number of goods produced or services provided.

When we consider fixed costs, we explore total fixed costs and fixed costs per unit.

The total fixed costs for a company do not vary based on the production volume. These amounts won’t change whether we produce 10 products or 10,000 products.

EXAMPLE

Some examples of fixed costs are factory rent, insurance, or property taxes. The owner of your factory building expects the same amount of rent each month regardless of how productive your company has been.If a manager wants to know the total cost per unit, they will need to identify the fixed cost per unit. In this case, we can expect that the fixed cost per unit will change with fluctuations in volume.

EXAMPLE

If the monthly rent is $4,000 and the volume is 200 units, the fixed cost per unit is $20 ($4,000/200 units).Knowing the fixed cost per unit will help managerial accountants determine the total costs that are related to each unit that is sold or produced, or each service that is provided.

Variable costs change with fluctuations in the volume of activity. With variable costs, the total amount of variable cost changes with the level of production, while variable cost per unit stays the same as volume changes.

EXAMPLE

If a pizza shop increases its production from 100 pizzas to 200 pizzas per day, the amount of dough required per day to make pizzas would double. However, the amount of dough per pizza (variable cost per unit) would stay the same.For manufacturing companies, direct material is a variable cost since it will fluctuate depending on the units of production. A merchandising company, specifically a retailer, can recognize credit card fees as variable costs given that they will be dependent on the number of credit card sales. Sales commissions are variable costs for service companies because the amount of commission will fluctuate depending on the number of services that are provided.

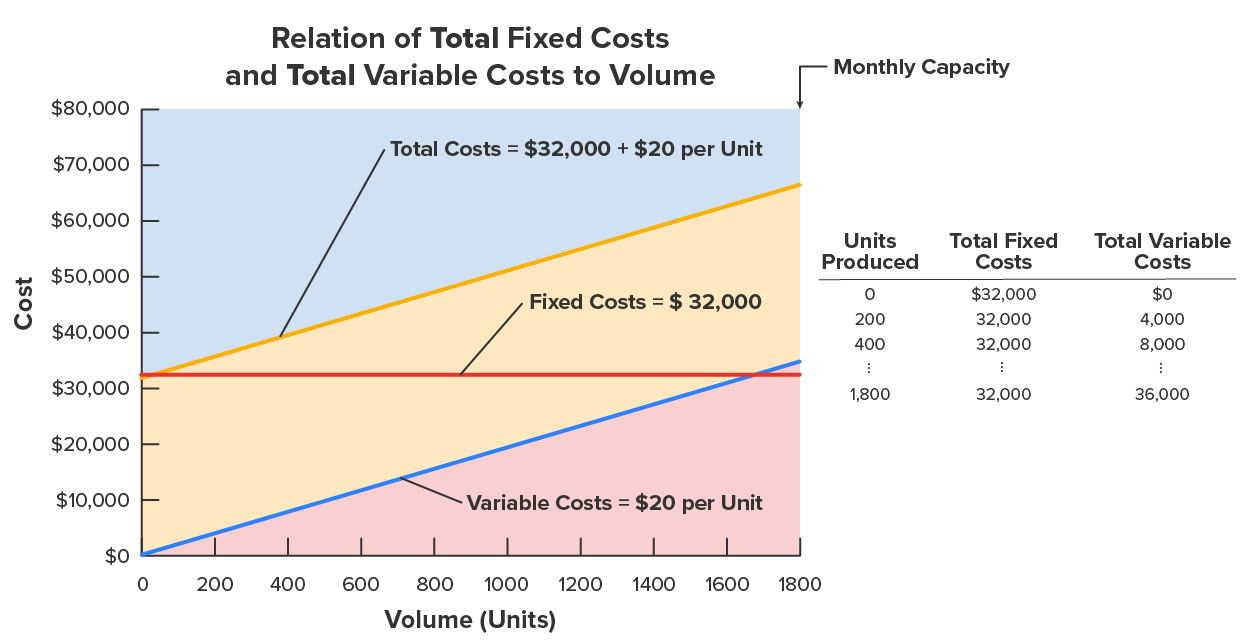

The image below shows the relationship between total fixed costs and total variable costs in relation to volume. Total fixed costs remain the same regardless of production level while total variable costs increase with each additional unit of production.

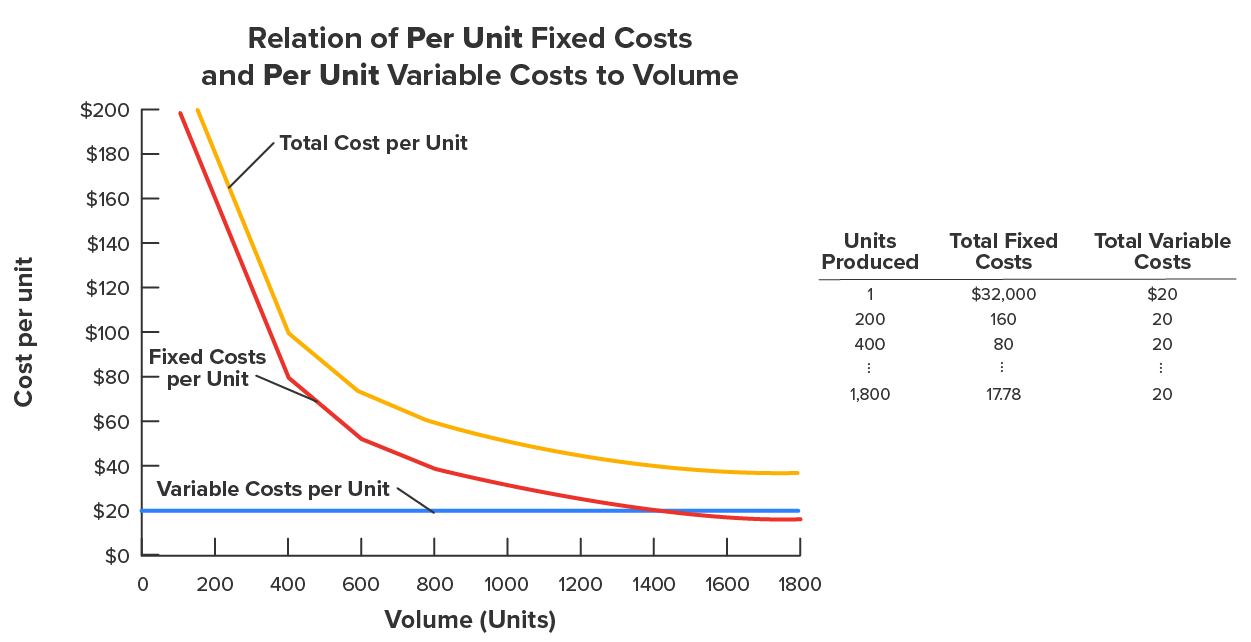

This graph shows how the fixed costs per unit decrease as production increases. We also see that variable costs per unit stay the same when the production levels change.

There might be instances where a company will have components of both fixed and variable costs; in this case, we have mixed costs. When the volume is at zero, the total cost equals the fixed costs and as the volume increases, the total cost increases at an amount equal to the variable cost per until. The total cost line is then a mixed cost.

EXAMPLE

An example of mixed cost would be electric service in which a company pays a fixed monthly service fee for electricity, along with a variable fee that depends on usage.IN CONTEXT

The global airplane manufacturing industry has a market size of $565.5 billion as of 2022. Airplane manufacturers sell thousands of airplanes and employ millions of people across the globe. These manufacturers have large facilities that are used to produce the airplanes and prepare them to be sold.

Even though the industry has over $500 billion in sales, managers of these companies know the costs that are related to the production process including seat belts, propellers, the wages paid to welders and computer programmers, and the salaries of production supervisors. Not only do airplane manufacturers know the costs that are related to producing airplanes, but they also know the level of profit that results from each sale. In most instances, managers are expected to know cost information on an ongoing basis in order to make decisions that will bring in the most profit for the company.

Costs may be either directly or indirectly related to a particular cost object. A cost object is a process, product, department, or other item for which costs are assigned. A cost object can be classified as either a direct cost or an indirect cost.

A direct cost is specifically traceable to a given cost object. As we learned in a previous lesson, examples of direct costs for manufacturing companies are direct materials and direct labor. For merchandising companies, the cost of goods sold can be considered a direct cost since it consists of the costs that are directly traced to the purchase of merchandise inventory. In service companies such as law firms, the lawyer’s salary can be directly traced to a specific case.

An indirect cost is not traceable to a given cost object. Indirect costs are referred to as overhead costs consisting of indirect materials, indirect labor, and any other indirect costs that are necessary for the company to complete its daily operations but are not directly traced to the production process, the sale of merchandise, or providing a service.

Manufacturing companies identify indirect costs as manufacturing overhead, such as factory depreciation or factory rent. For merchandisers, the company’s operating expenses can be considered indirect costs. These costs include selling and administrative expenses that are necessary for the merchandiser to operate, but that are not directly linked to the purchase of inventory to be sold. For service companies, the salary of the janitor who cleans the offices is an indirect cost.

Accountants can designate a particular cost as direct or indirect by making reference to a given cost object. Therefore, a cost that is direct to one cost object may be indirect to another.

EXAMPLE

The salary of a department manager may be a direct cost of a given manufacturing department but an indirect cost of one of the products manufactured by that department. In this example, the department and the product are two distinct cost objects.Since a direct cost is traceable to a cost object, the cost is likely to be eliminated if the cost object is eliminated.

EXAMPLE

If the plastics department of a manufacturing company closes down, the salary of the manager of that department will more than likely be eliminated.An indirect cost is not traceable to a particular cost object; therefore, it only becomes an expense of the cost object by splitting or allocating the expenses amongst the different departments. In a given situation, it may be possible to identify an indirect cost that would be eliminated if the cost object were eliminated, but this would be the exception to the general rule.

EXAMPLE

Consider the depreciation expense on the company headquarters building that is allocated to each department of the company. The depreciation expense is a direct cost for the company headquarters, but it is an indirect cost to each department. If a department of the company is eliminated, the indirect cost for depreciation assigned to that department does not disappear; the cost is simply allocated between the remaining departments.Because the direct costs of a specific department are clearly identified within that department, these costs are often controlled by the department manager. In contrast, indirect costs become department costs only through allocating the expenses; therefore, most indirect costs are not controlled by the department manager.

Another way to classify costs is as product costs or period costs. As discussed in the costs for manufacturer’s lesson, the product cost consists of the total costs that are necessary to make a product. Product costs in a manufacturing company will generally consist of direct materials, direct labor, and overhead. When a product is completed, it is transferred to the finished goods inventory and recorded as an asset on the balance sheet. Once the product is sold, it is then recorded as the cost of goods sold on the income statement.

A merchandising company identifies product costs as the cost of purchasing the inventory items that they sell. Similar to manufacturing companies, merchandising companies record their product costs as merchandise inventory in the balance sheet and later as the cost of goods sold on the income statement once the inventory is sold to customers. For service companies, there aren’t any costs that are classified as product costs since providing services does not involve inventoried products.

Period costs are nonproduction costs that are typically associated with activities that are linked to a time period rather than with completed products. Examples of period costs are selling and administrative expenses such as sales staff salaries, advertising expenses, rent for the administrative building, and utilities paid for the marketing office. While these examples reflect what we have previously identified as indirect costs, the difference between indirect costs and period costs is that period costs are matched with the revenue of a specific time period and expensed in the same accounting period. Period costs flow directly to the income statement as expenses, but they are not reported as assets on the balance sheet.

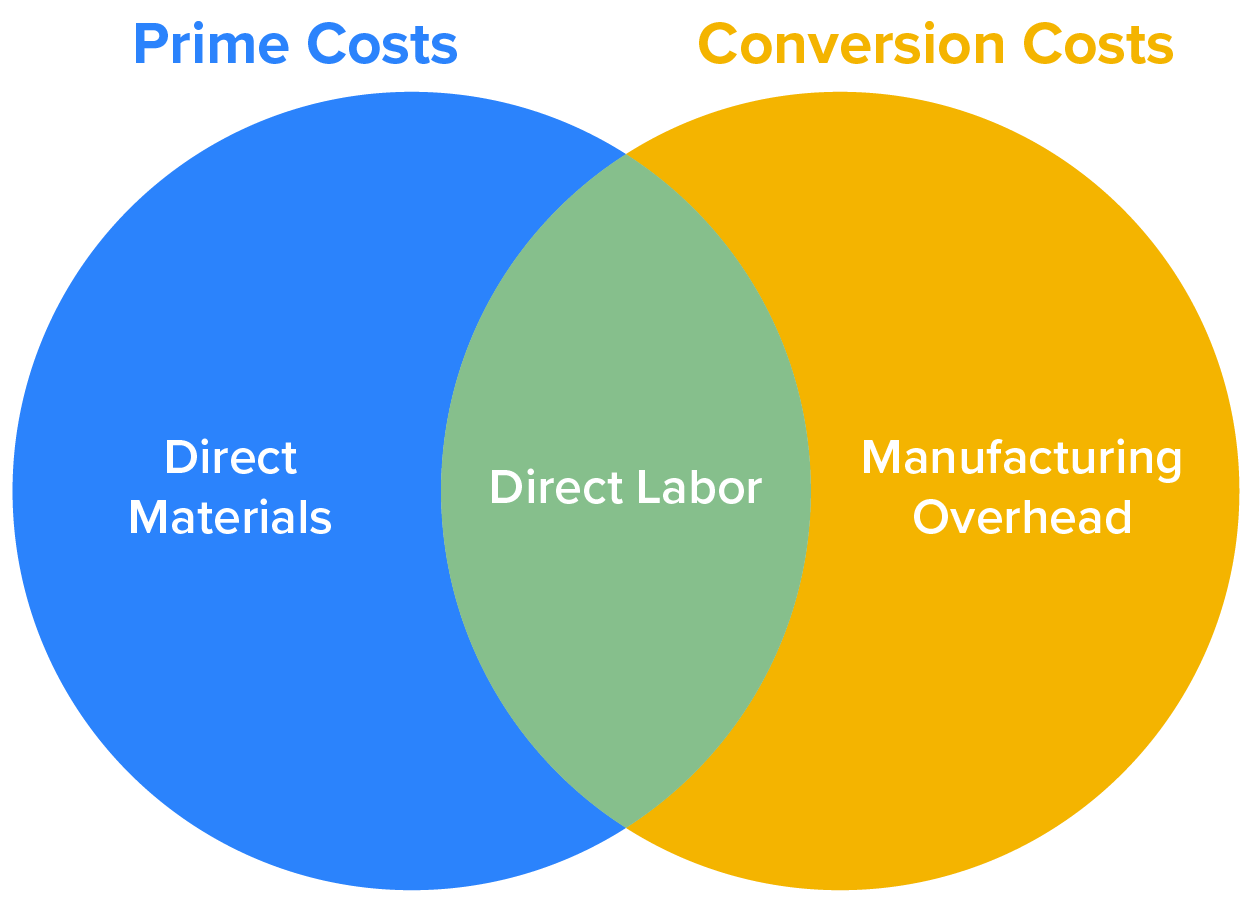

For manufacturing companies, we can go a step further and classify our product costs as either prime costs or conversion costs. Making this distinction helps managers determine the efficiency of their manufacturing processes and set a product’s price based on the desired profits. Prime costs and conversion costs are similar; however, there are some key differences between the two.

Prime costs are any expenses that are directly related to turning raw materials into finished products or the total of direct materials and direct labor. The prime cost helps to set the price at a level that can easily generate sufficient profit for the company.

EXAMPLE

Joe’s Building Company wants to determine the prime costs for their paint department in order to figure out ways to minimize their costs within the department. Their prime costs might consist of paint, paint supplies, and the painters’ wages since they are the direct materials and direct labor that are used in the process of creating finished products.Conversion costs, on the other hand, are the expenses that are incurred when turning raw material into finished products. These costs consist of combining the direct labor and the overhead without considering the raw materials. For a manager, determining the conversion costs can help to identify any areas in the production process that might need improvement, since they are looking at direct labor and the indirect labor that is included in the overhead. Conversion costs can also help managers track production expenses because the conversion of raw materials into finished products is highly dependent on the labor that is included in the process.

EXAMPLE

Joe’s Building Company wants to ensure that their painters are working efficiently. The painting department is highly labor intensive, so they will use the direct and indirect labor costs to determine if they are able to reduce the amount of wages that are being paid in the painting department.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM “ACCOUNTING PRINCIPLES: A BUSINESS PERSPECTIVE” BY hermanson, edwards, and maher. ACCESS FOR FREE AT www.solr.bccampus.ca. LICENSE: CREATIVE COMMONS ATTRIBUTION 3.0 UNPORTED.

REFERENCES

Kolmar (2022). The 10 largest aircraft manufacturers in the world. www.zippia.com/advice/largest-aircraft-manufacturers/