Table of Contents |

Now that you’ve learned about how companies find and use short-term financing, let’s take a look at how they might use long-term financing and the types of long-term financing.

Long-term financing involves funds that a business either borrows or raises for more than 1 year, typically extending over 10, 20, or even 30 years. These funds are mainly allocated for major capital projects or strategic growth initiatives that require time to produce returns.

Companies also seek long-term financing to do the following:

One main advantage of long-term debt financing is that it provides immediate access to significant capital while allowing the business to spread out repayment over time, which can ease short-term financial pressure. Additionally, interest payments are often tax deductible, and the business retains full ownership, unlike equity financing, which we will cover in an upcoming lesson.

However, the downside is that long-term debt creates a lasting financial obligation that can limit flexibility, especially if interest rates rise or the company’s revenue fluctuates.

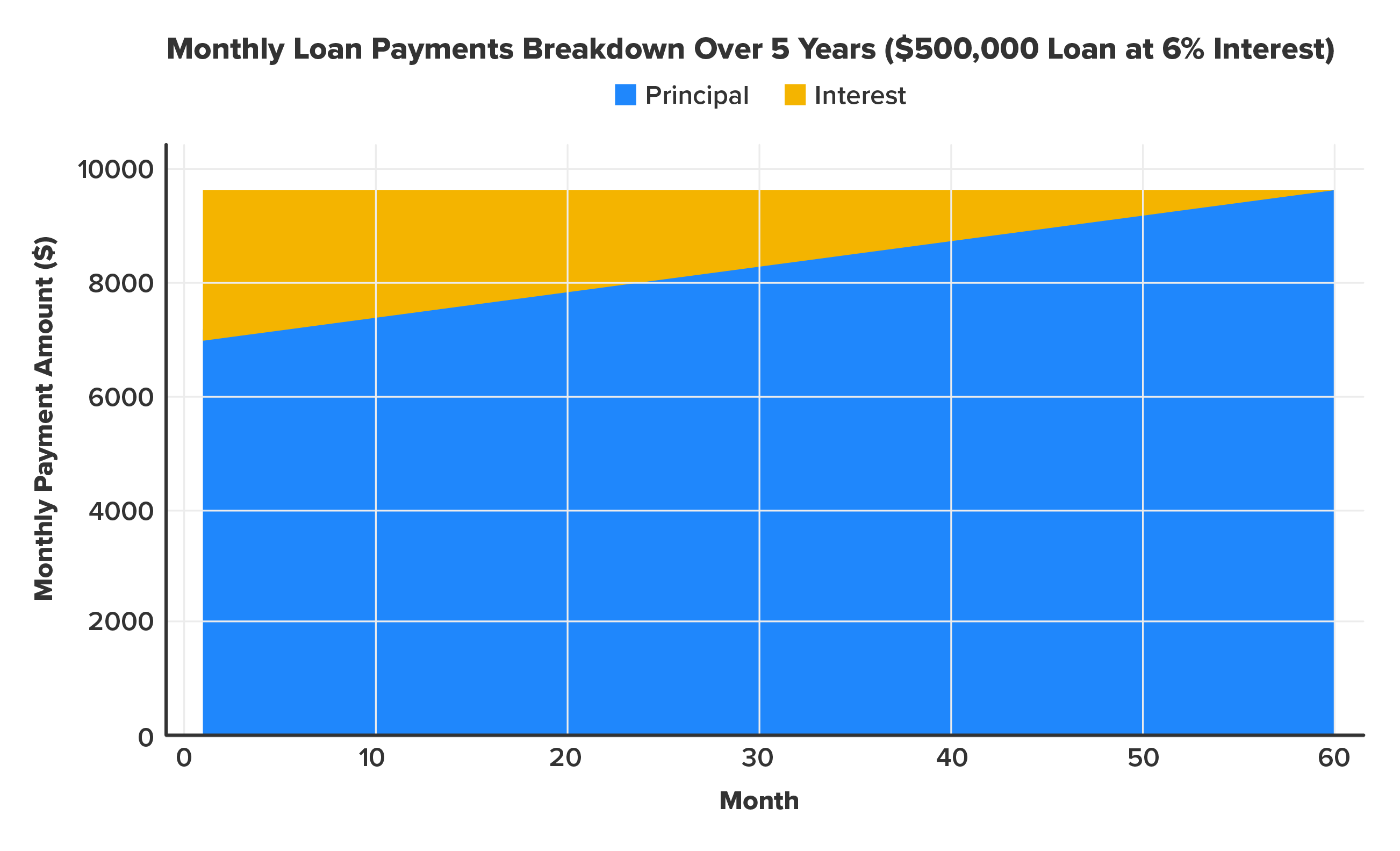

Let’s suppose Maria, the owner of Sweet Crumbs, decides to open a new location and takes out a loan to open the location and buy equipment and supplies.

IN CONTEXT: Sweet Crumb’s New Location

Assume the loan that Maria takes out is for $500,000, and she pays 6% interest over 5 years.

As you can see, Maria would be paying quite a bit of interest every month (in orange) at the beginning of the loan. As she nears the end of the 5-year repayment period, she is paying more toward the principal.

Corporate bonds are attractive to companies because they allow access to funding without giving up equity or ownership control. They are also more flexible than bank loans in terms of structure and repayment terms. However, issuing bonds requires the company to have a solid credit rating; otherwise, it may have to offer higher interest rates to attract investors.

Corporate bonds are a type of long-term debt financing that companies use to raise large amounts of capital from investors. When a business issues a corporate bond, it is essentially borrowing money from bondholders in exchange for a promise to repay the principal (the face value of the bond) at a specified future date, known as the maturity date.

Bonds can be either secured (backed by company assets) or unsecured (backed only by the company’s creditworthiness). Let’s look at some of the different types of corporate bonds.

| Type of Corporate Bond | Secured or Unsecured | Description |

|---|---|---|

| Secured Bonds | Secured | They are supported by assets such as equipment or real estate. |

| Debentures | Unsecured | They rely on creditworthiness and are not supported by assets. |

| Convertible Bonds | Unsecured | They can be converted into company stock at a later time. |

| Callable Bonds | Both | The company can repay it early before it reaches maturity. |

| Zero-Coupon Bonds | Both | They are sold at a discount with no interest charged during the bond’s duration; the full amount is paid at maturity. |

Usually, the only companies that issue bonds are mid to large corporations, and it would be unlikely that a smaller business, such as Maria’s bakery, would issue bonds.

Let’s look at some of the bonds issued in 2025 and the reasons why they were issued so that you can get an idea of how large corporations use bonds as a method for long-term financing.

| Picture | Issuer | Approx. Amount | Purpose |

|---|---|---|---|

|

JPMorgan Chase | $6 B | It issued bonds to raise money that helps the bank keep enough cash on hand and support its day-to-day business activities (Gelsi, 2025). |

|

Nissan Motor | $4.52 B | It issued bonds to get money to pay off older debts and to help finance its ongoing business plans, such as making new cars or investing in technology (Foley, 2025). |

|

Verizon | $1.79 B | Bonds were issued to fund network upgrades and 5G rollouts (Foley, 2025). |

|

Disney | $1.75 B | It issued bonds to support theme park expansions (Schmitt & Platt, 2025). |

|

Mars, Inc. | $25–30 B (multiyear bonds) | Bonds were issued to finance the acquisition of Pringles-maker Kellanova (Ramakrishnan, 2025). |

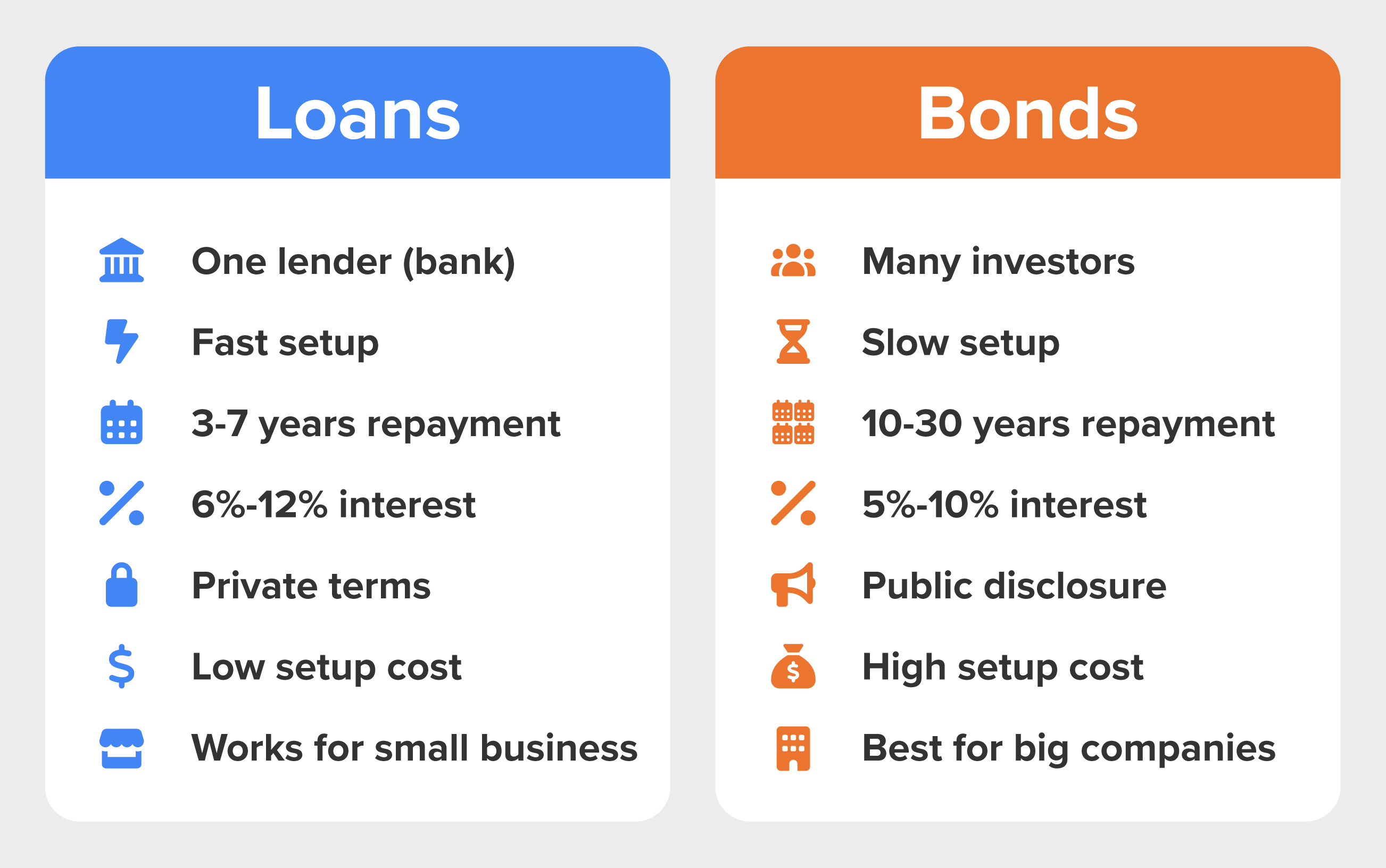

When deciding between long-term loans and bonds, companies consider several key factors. Bonds are typically favored for raising large amounts of capital because of their access to a broad range of investors, whereas loans are often more suitable for smaller financing needs. In terms of cost, loans may be less expensive upfront because of lower issuance fees, but bonds can offer more favorable long-term interest rates, particularly for companies with strong credit ratings. Flexibility also plays a role—loans tend to offer more customizable terms, while bonds are generally more rigid once issued. A company’s financial health is crucial as well; those with strong credit profiles can issue bonds more easily and at lower costs, while those with weaker credit may rely more heavily on bank loans. Finally, market conditions, such as prevailing interest rates and investor demand, significantly influence the choice between these two financing options.

Let’s take a look at bonds versus loans and compare the two.

Long-Term Loans:

It is hard to talk about finance without having a conversation about risk and return, which we touched on in the first lesson, Role of Financial Management. Risk, in finance, refers to uncertainty or variability in investment outcomes.

Recognizing and managing these risks helps investors balance their portfolios and align their investments with risk tolerance and financial goals. These risks are crucial for a company to understand because they directly impact the company’s financial health, decision making, and ability to meet its goals using long-term financing.

There are a few different types of risk—let's talk about those next.

One key type is market risk, which refers to the possibility that the overall market declines, negatively impacting most investments regardless of individual qualities. Another important risk is credit risk, the chance that a borrower will fail to meet its debt payments, potentially causing losses for lenders or bondholders. Investors also face liquidity risk, meaning they might not be able to sell an investment quickly without suffering a significant drop in its value, which can be problematic if cash is needed urgently. Additionally, there is inflation risk, the danger that rising inflation will reduce the real purchasing power of investment returns, causing the actual value of gains to be less than expected. Lastly, interest rate risk affects mainly bonds and other fixed income securities; it arises because changes in interest rates can cause the market value of these investments to fluctuate, often moving inversely to rate shifts.

Imagine you have $1,000 to invest:

Every business decision—whether it’s investing in new projects, expanding operations, launching products, or borrowing money—involves weighing the potential benefits against the possible downsides.

Source: THIS CONTENT HAS BEEN ADAPTED FROM OPENSTAX "INTRODUCTION TO BUSINESS". ACCESS FOR FREE AT openstax.org/details/books/introduction-business. LICENSE: CREATIVE COMMONS ATTRIBUTION 4.0 INTERNATIONAL. Accessed by May 2025.

REFERENCES

Foley, J. (2025, May 9). Big Tech covets an old-world status symbol: Long-term debt. Financial Times. www.ft.com/content/b8bbde6c-0147-4c59-a270-f1355e9d25b0

Gelsi, S. (2025, April 14). Fresh debt from JPMorgan, Morgan Stanley draws warm reception from investors in hopeful sign. MarketWatch. www.marketwatch.com/story/fresh-debt-from-jpmorgan-morgan-stanley-draws-warm-reception-from-investors-in-hopeful-sign-6f7cab9e

Ramakrishnan, S. (2025, March 5). Mars prices $26 billion 8-part bond, highlights big M&A financing week. Reuters. www.reuters.com/markets/deals/mars-announces-8-part-bond-headlines-big-ma-financing-week-2025-03-05/

Schmitt, W. & Platt, E. (2025, April 16). Venture Global debt deal wakes US junk bond market from tariff slumber. Financial Times. www.ft.com/content/fcb101b7-6c45-4afa-a1d5-9ab4b4921dec