1. Listed Property

Listed property with a business-use percentage of 50% or less must be depreciated using the straight-line method over an ADS recovery period.

Over the next few sections, we’ll break down this rule.

1a. What Is Listed Property?

Certain types of property that are commonly used for both personal and business use are classified as “listed property.”

They include:

- Passenger automobiles weighing 6,000 pounds or less.

- Any other property used for transportation property (with a few exceptions).

- There are exceptions for certain types of vehicle which, by their design, are not suitable for personal use. Examples include ambulances, hearses, taxis, marked police and fire vehicles, school buses, tractors, cherry pickers, cement mixers, combines, cranes, delivery trucks with seating only for the driver or the driver plus a folding jump seat, passenger buses with the capacity for 20 or more passengers, flatbed trucks, refrigerated trucks, and cargo vehicles with a gross vehicle weight of 14,000 pounds or more.

- Property generally used for entertainment, recreation, or amusement.

- This includes photographic, phonographic, and video-recording equipment. However, if used exclusively in a taxpayer’s trade or business or at the taxpayer’s regular business establishment, they are not considered listed property.

-

Cell phones and computers were both listed property at one time. Cell phones and other telecommunications equipment stopped being listed property beginning in 2010. Computers and related equipment were removed from this category beginning in 2018.

However, computers placed into service before 2018 and cell phones placed into service before 2010

are listed property.

1b. Business-Use Percentage

For any item of listed property, you must allocate the amount of use between business and personal use.

For cars and other means of transportation, this is done by looking at the number of miles driven for business purposes compared to the total number of miles driven during the year. If the number of business miles divided by the total miles exceeds 50%, the business-use requirement is met.

For other listed property, look at the time that this property is actually used for business versus other purposes.

In either case, good recordkeeping is essential! The IRS requires taxpayers claiming a depreciation or §179 deduction for listed property to have evidence to support their claim of business use. A good practice is to maintain a contemporaneous log that documents time used (or miles driven) for business and non-business purposes.

-

EXAMPLE

Joshua owns a cake decorating business and drove his personal car 5,780 miles making deliveries. The total number of miles that he drove his car during the year was 9,995 miles.

Joshua used his car 57.83% for business [5,780 ÷ 9,995 = 57.83% business use], which means that the car meets the business-use test and does not have to be depreciated using the straight-line method over an ADS recovery period.

-

EXAMPLE

Paige operates an administrative assistant business. She drove her personal car 590 miles for business purposes. The total number of miles she drove her car this year was 5,288.

She used her car 11.16% for business [590 ÷ 5,288 = 11.16% business use]. Since an automobile is listed property, and the business use is less than 50%, if she depreciates the vehicle, she must use the straight-line method over an ADS recovery period.

1c. If the Property Fails the Business-Use Test

If the use is 50% or less in the year placed in service, the property does not qualify for the §179 deduction or special depreciation allowance (discussed later).

If the asset’s business-use percentage begins above 50% but then decreases to 50% or less in a later year, the taxpayer must include recapture of any depreciation claimed (including special depreciation and the §179 deduction) that is in excess of the amount they could have claimed under the ADS straight-line method. The recapture must occur in the first year that the business-use percentage falls below the required amount. The taxpayer must use the straight-line method over an ADS recovery period for all subsequent years (even if the business-use percentage later rises over 50%).

-

- Recapture

- The inclusion of a previously deducted or excluded amount in gross income or tax liability. Recapture may be applicable to accelerated depreciation, cost recovery, amortization, and various credits.

Although you should be aware of the concept of depreciation recapture, you will not be asked to calculate or report recapture amounts in this course.

You will, however, need to understand how to claim the regular depreciation for listed property. We discuss this next.

2. Reporting Depreciation for Listed Property

Taxpayers calculating depreciation for listed property will need to report the deduction in the same three places as for non-listed property:

- The Depreciation Worksheet or a similar recordkeeping tool.

- Form 4562, Depreciation and Amortization.

- The appropriate business schedule (e.g., Schedule C, D, E, or F).

-

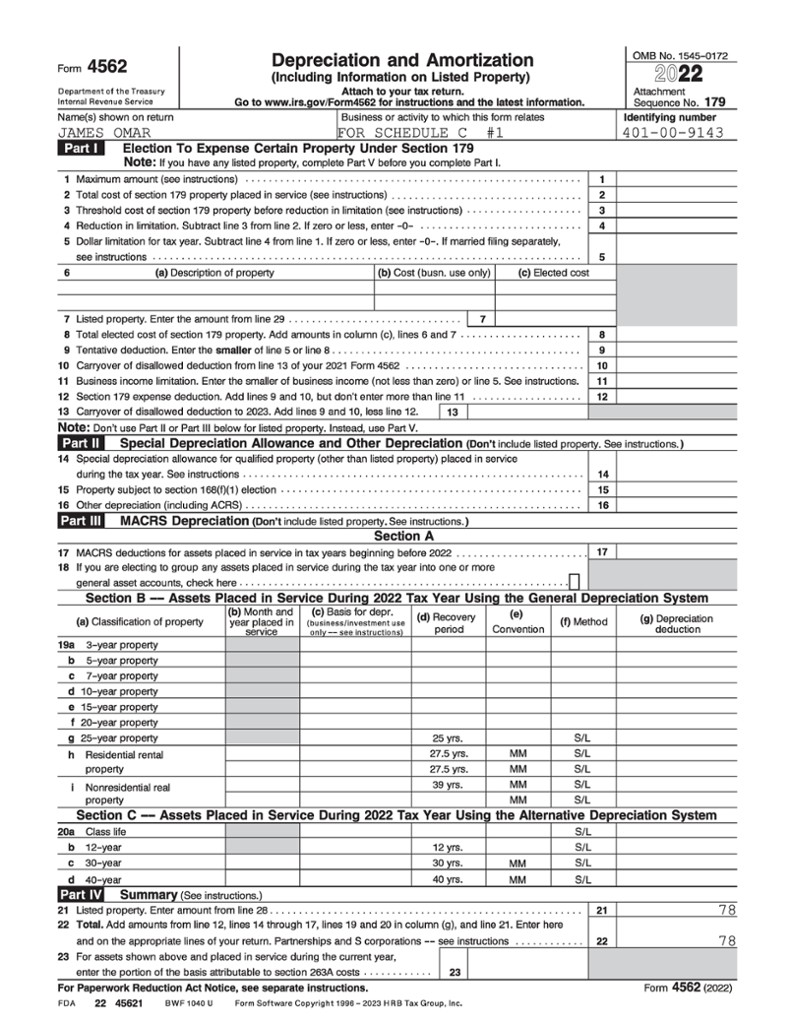

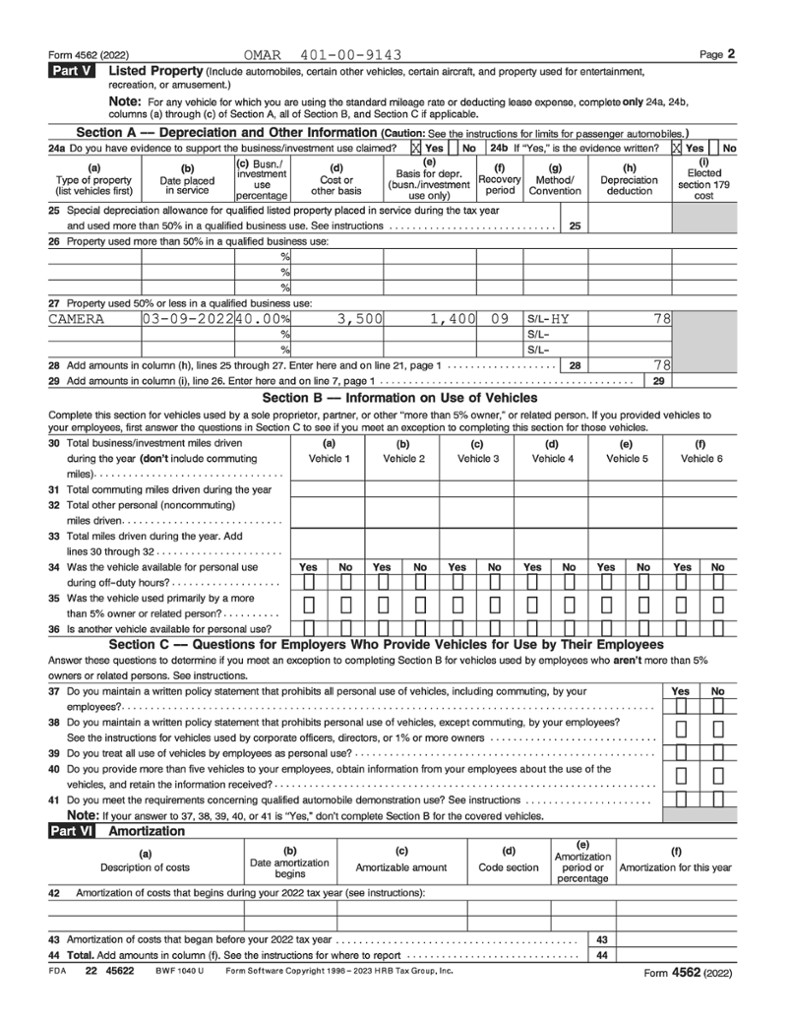

EXAMPLE

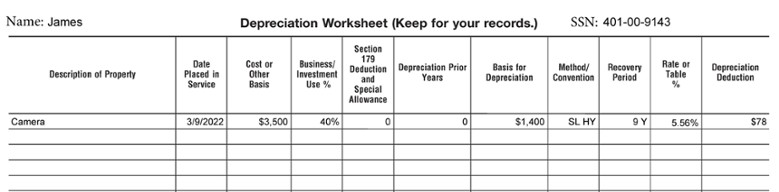

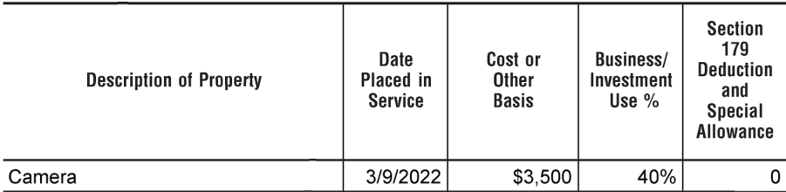

On March 9, 2022, James Omar purchased and placed in service a camera that cost $3,500. He uses the camera 40% of the time for his photography portraiture business. He also uses it 60% for his personal photography hobby. James keeps a written log of how he uses the camera.

The camera is listed property, and it is not used exclusively in a place of business. Thus, it must be reported on page 2 of Form 4562. Because it is used 50% or less for business, the camera is not eligible for special depreciation or the §179 deduction. Further, James must use the ADS straight-line depreciation method.

James’

Depreciation Worksheet for his camera is shown below.

Let’s examine James’

Depreciation Worksheet in more detail.

-

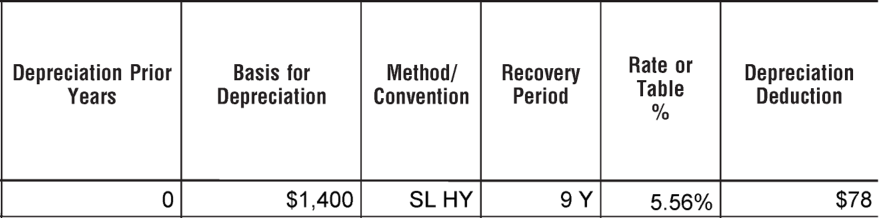

Basis for Depreciation: James’ basis for depreciation is the adjusted basis of the camera multiplied by his 40% business-use percentage [$3,500 × 40% = $1,400].

-

Method/Convention: Because James does not use his camera more than 50% for business use, he must use the straight-line method over an ADS recovery period to depreciate it.

-

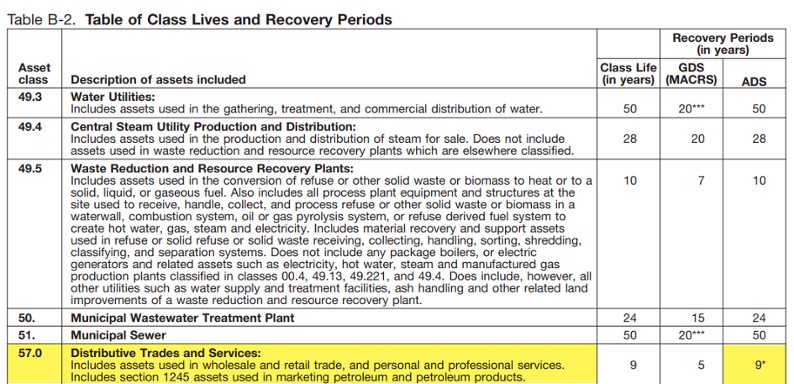

Recovery Period: Photography portraiture is a personal or professional service under Asset Class 57.0, Personal and Professional Services, of the CLADR table. The ADS class life for this category is nine years.

-

Rate or Table %: This percentage was obtained from Table A-8 in IRS Publication 946.

Form 4562

Form 4562 must be filed with the return whenever a depreciation deduction is claimed for listed property, regardless of whether it is the first year the property was placed into service.

Form 4562 for James Omar appears below.

Business Schedule

Business Schedule

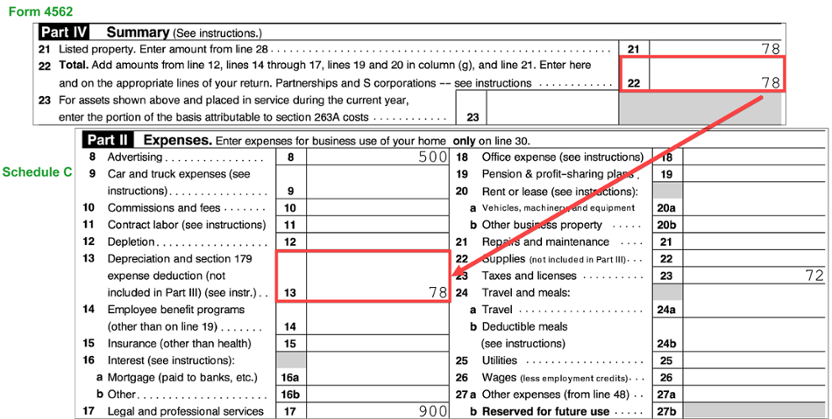

After completing Form 4562, the amount of the depreciation deduction is transferred from Form 4562, line 22, to the appropriate business schedule.

3. Form 4562 Overview: Video 2

-

The following video clip discusses how this form is used to claim depreciation on listed property.