Table of Contents |

The lifetime learning credit is claimed on Form 8863, Parts II and III. It is simpler than the AOTC calculation and is pretty straightforward.

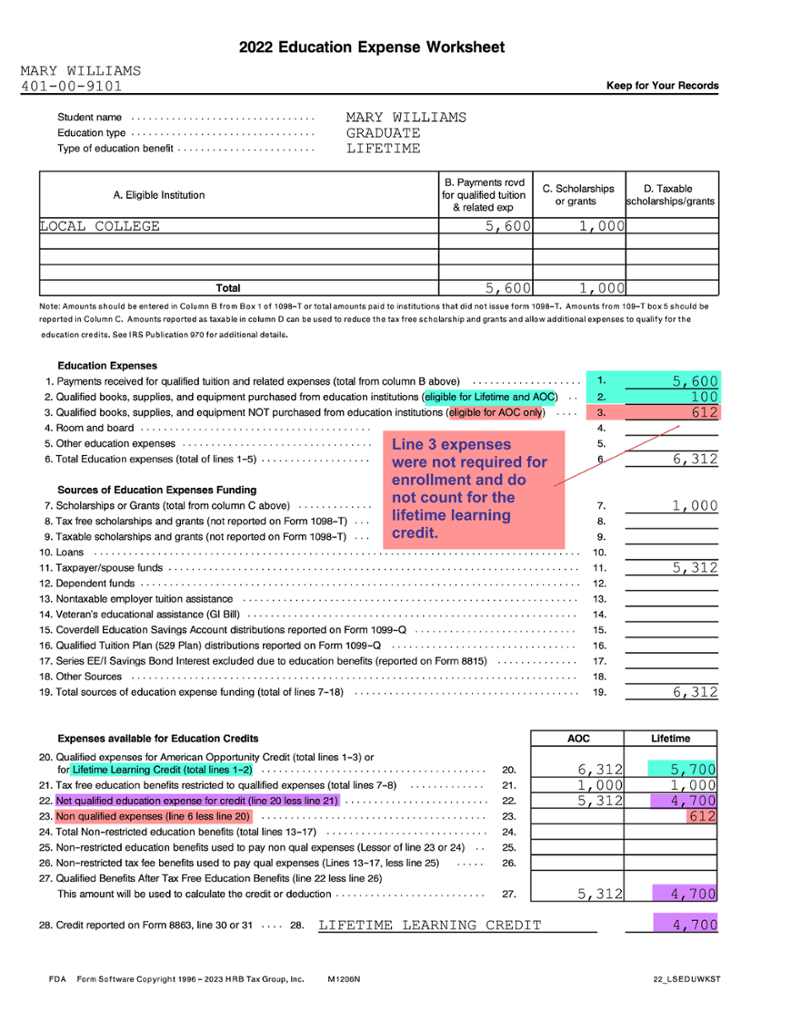

Recall Mary Williams from the previous example in the AOTC Example section. If all the facts are the same from the previous example, except she has claimed the AOTC in four previous years, Mary will not qualify for the AOTC. However, she will qualify for the lifetime learning credit.

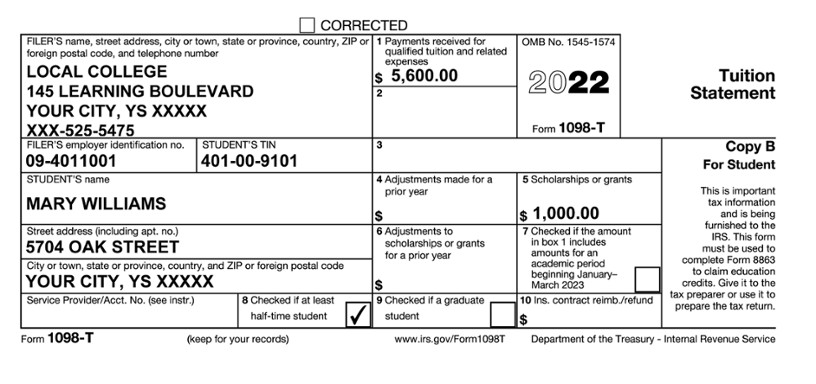

Just to recap, Mary received a Form 1098-T from Local College. Mary’s tuition expenses of $5,600 meet all of the qualifications for the AOTC. Mary also received a $1,000 grant. In addition to the expenses reported on Form 1098-T, Mary spent $712 on all of her textbooks, including one book ($100) required as a condition of enrollment and three other books ($612) not required as a condition of enrollment. She purchased them through an online book retailer and the school. Mary’s AGI (and MAGI) is $39,000. Mary’s Form 1098-T is shown below.

The books not required as a condition of enrollment are entered on line 3 of the Education Expense Worksheet since they are not allowable expenses for the lifetime learning credit. The books purchased as a condition of enrollment are entered on line 2 since they are allowable expenses for the lifetime learning credit.

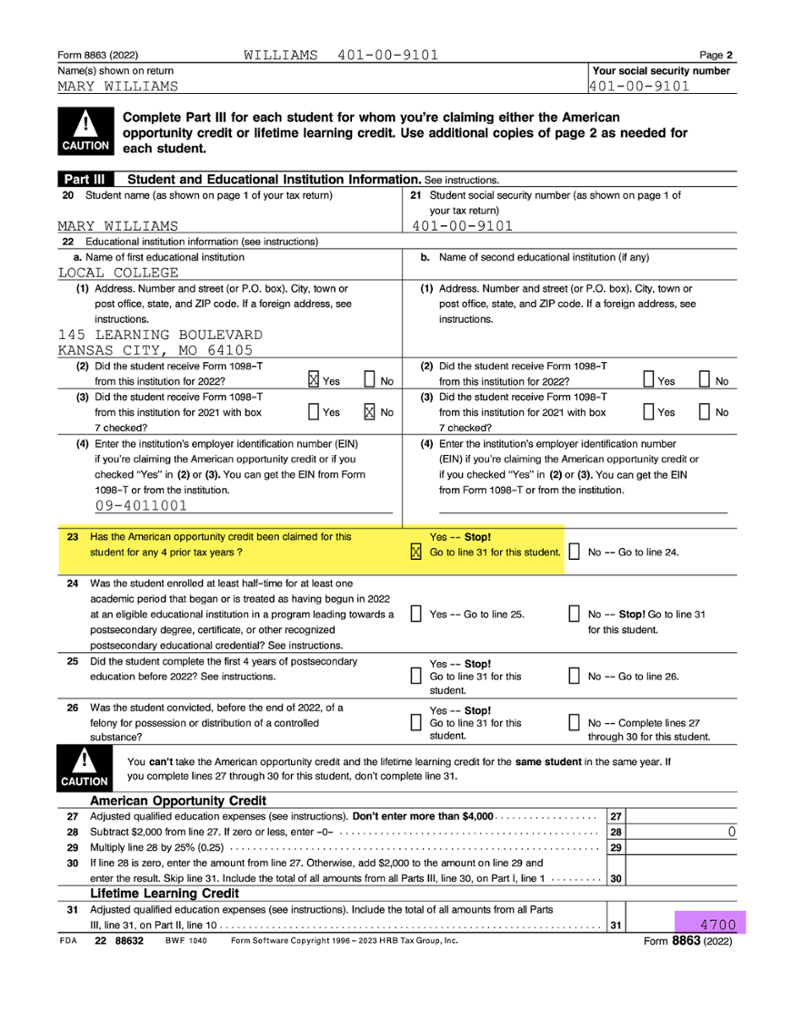

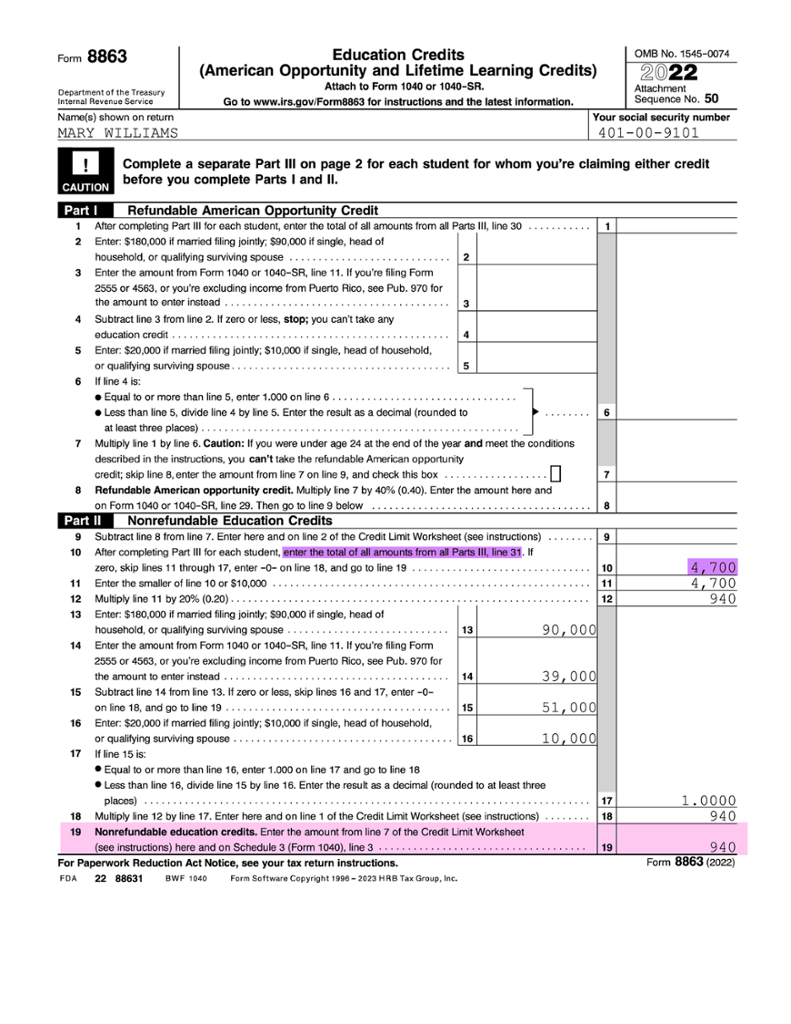

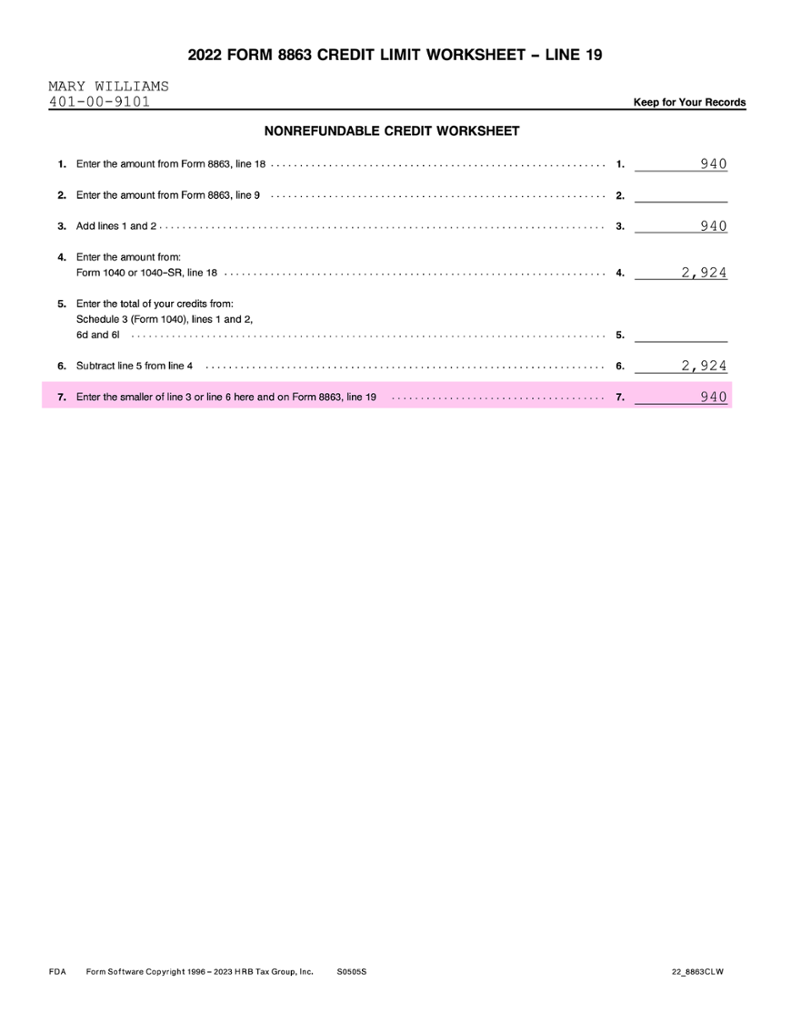

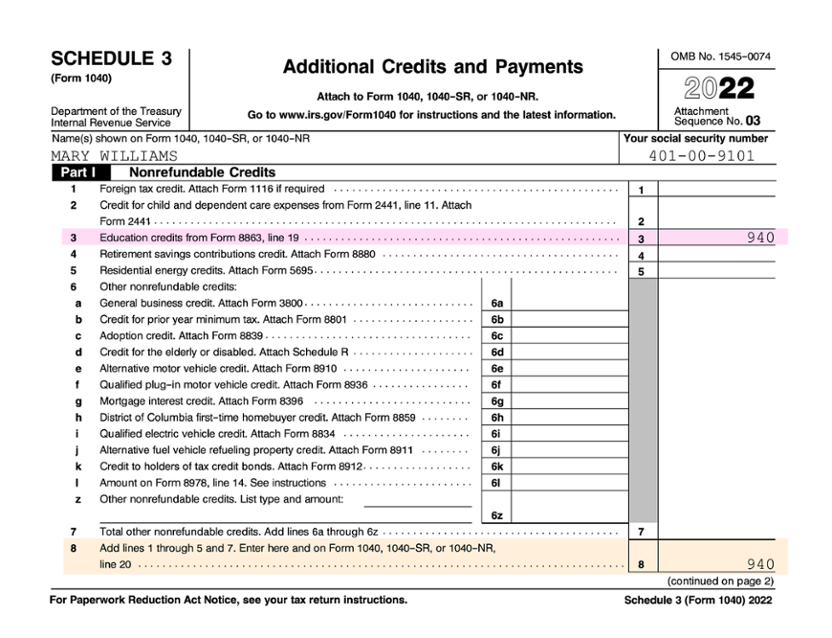

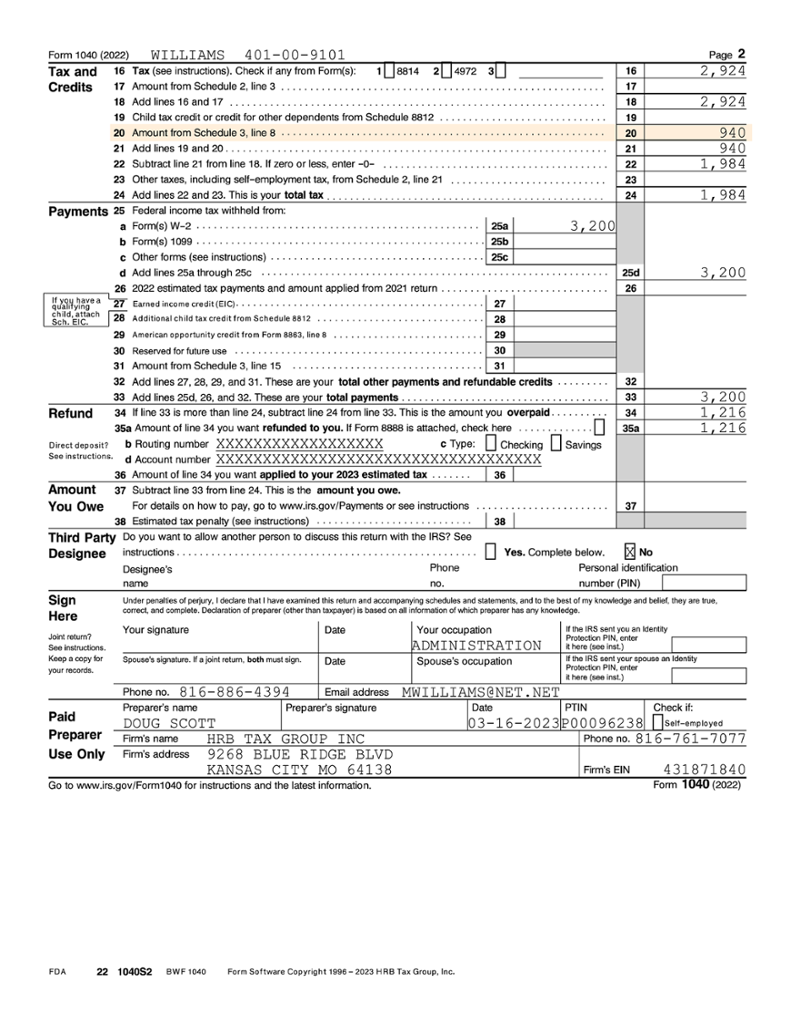

Mary’s MAGI of $39,000 is below the lifetime learning credit MAGI phaseout range of $80,000–$90,000, making her lifetime learning credit $940 [$4,700 qualified expenses × 20% = $940 lifetime learning credit]. Mary’s completed Form 8863 is presented below. Mary reports her $940 lifetime learning credit on Schedule 3, line 3, which then carries to Form 1040, line 20.

Mary’s forms are provided below in the order they would be completed when preparing the tax return, including the Education Expense Worksheet; Form 8863; Form 8863 Credit Limit Worksheet; Schedule 3; and Form 1040, page 2.

The table presented below provides an overview of the lifetime learning credit eligibility requirements for 2022. Generally, the lifetime learning credit may be claimed if all of the requirements shown in the table are met.

| Lifetime Learning Credit | |

|---|---|

| Maximum credit | $2,000 per tax return. |

| Limited credit based on MAGI |

MAGI between $80,000 and $90,000 if single, HOH, or QSS. MAGI between $160,000 and $180,000 if MFJ. |

| Excluded from the credit based on MAGI |

MAGI $90,000 or above if single, HOH, or QSS. MAGI $180,00 or above if MFJ. |

| Refundable or nonrefundable | Nonrefundable. |

| Number of years of postsecondary education | Available for all years of postsecondary education and for courses to acquire or improve job skills. |

| Number of tax years credit is available | Available for an unlimited number of years. |

| Degree requirement | The student does not need to be pursuing a postsecondary degree if they are taking the courses to acquire or improve job skills. |

| Course load requirement | Available for one or more courses. |

| Felony drug conviction | Felony drug convictions do not disqualify the student for the lifetime learning credit. |

| Qualified expenses |

Tuition and fees required for enrollment. The cost of books, supplies, equipment, student activity fees, etc. is not a qualified expense, unless it is required to be paid directly to the institution as a condition of enrollment or attendance. A book purchased from the school bookstore is NOT the same thing as being purchased from the school as a condition of enrollment or attendance. If the book must be purchased from the school in order to enroll in the course, then it is an eligible expense. |

| Academic periods | Payments made in 2022 for academic periods beginning in 2022 and the first three months of 2023. |