In this lesson, you will understand the life stages of personal finance. You’ll also uncover why your life stage matters. Specifically, this lesson will cover the following:

-

Before diving into the specifics of life stages, let’s ask a few reflective questions:

- Where are you on your financial journey?

- What’s your biggest money goal right now?

- Have you considered how your priorities might shift over the next decade?

Understanding your current stage and anticipating future ones help you take actionable steps toward financial confidence. No matter where you’re starting, this course is designed to help you navigate financial transitions and make empowered choices that align with your life values.

1. The Life Stages of Personal Finance

Personal finance can feel overwhelming, especially if you’re just starting out. There’s a sea of advice coming at you from every direction—save for retirement, pay off debt, invest, stick to a budget, build an emergency fund—and it’s enough to make anyone’s head spin. The truth is it can feel like there’s so much to do, and no clear road map for where to even start.

But here’s the thing: Managing money doesn’t have to be complicated or stressful. The key is to focus on the basics; take small, manageable steps; and understand that your financial life is a journey, not a sprint. It’s okay if you don’t know everything right now. The important thing is to start where you are.

Think of your financial life as a story with three main chapters known as life stages. Each chapter builds on the one before it, and, together, they form the bigger picture of your financial journey:

- Building Your Foundation (Getting Started with Money): This is the starting line—the part of your story where you’re learning to manage your income, expenses, and maybe even debt. It’s about creating habits that set you up for success in the long run.

- Protecting What You’ve Built (Keeping Things Steady): As you gain more stability and responsibilities, this chapter focuses on maintaining what you’ve worked hard to achieve and preparing for unexpected events that could derail your plans.

- Leaving Your Legacy (Making Sure It Lasts): Eventually, you’ll reach the point where you’ll think about what happens after you’re gone. This chapter is about ensuring that the money and resources you’ve built go to the people or causes you care about in the way you want.

Each chapter has its own focus and challenges, but here’s the good news: You don’t have to tackle everything all at once. Wherever you are in your money story, there are simple, actionable steps you can take to keep moving forward.

Let’s break it all down into bite-sized, relatable pieces that make sense—because personal finance shouldn’t feel like an impossible puzzle. It should feel like a series of steps that build toward the life you want.

-

Many of the terms and financial decisions we discuss in this lesson will be detailed in future lessons. Don’t worry about learning everything you need to know at this point; we’ll guide you through it all during this course. For now, focus on some of the key concepts that come with each life stage.

|

Financial Life Stages

|

|---|

|

Life Stage

|

Life Events

|

Financial Events

|

|

Building your foundation

|

- Entry into the workforce

- Marriage

- Children

|

- Development of financial habits

- Purchase of a car

- Purchase of a home

|

|

Protecting what you’ve built

|

- Family growth

- Career advancement

- Inheritance

|

- More home purchases

- Accumulation of wealth

- Funding of college educations

|

|

Leaving your legacy

|

- Major promotion

- Retirement

- Grandchildren

- Death of spouse

|

- Greater tax sensitivity

- Wealth preservation

- Estate planning

|

-

- Life Stages

- The phases of building, protecting, and passing on your wealth.

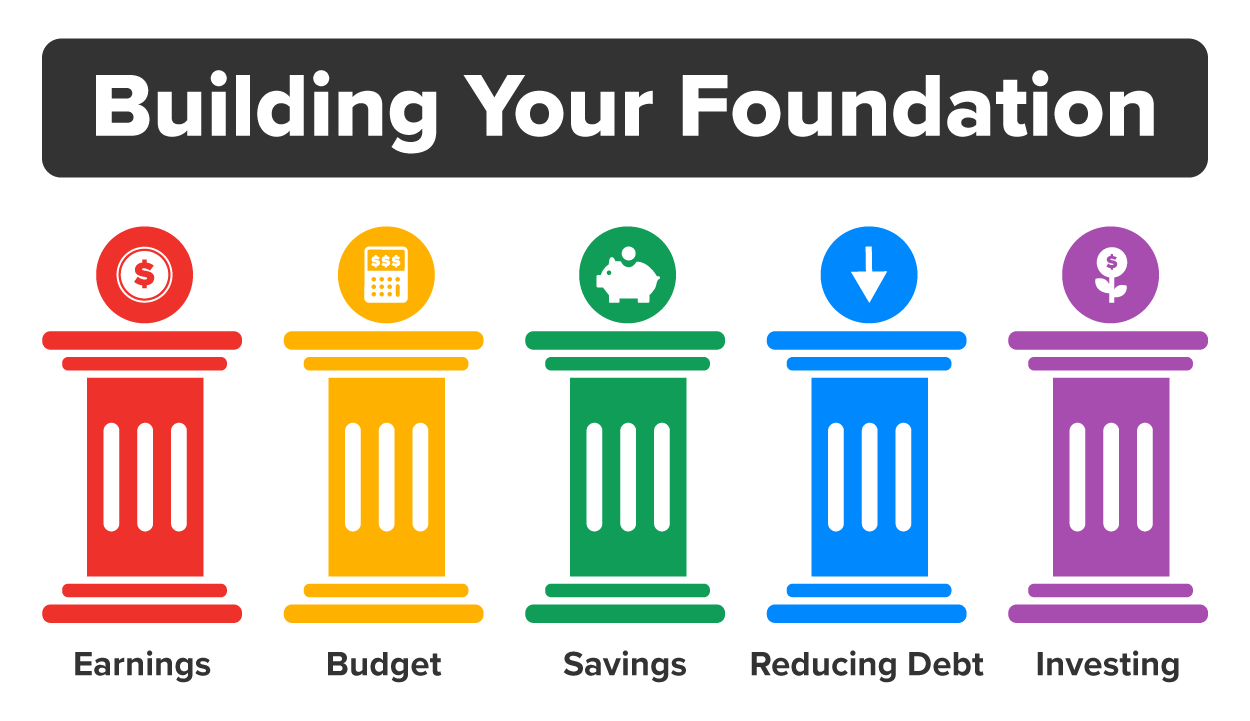

1a. Building Your Foundation

This is where your financial journey begins. Think of it as the stage where you lay the groundwork for everything that comes later. It’s about building habits, setting up systems, and figuring out how to manage money so it works for you, not against you.

If you’re just starting out—maybe in your 20s or 30s—this chapter might feel like a whirlwind. You’re earning money, probably paying rent or a mortgage, handling bills, and trying to save for the future, all while balancing other goals like paying off debt or traveling. It can feel like there’s never enough money to go around.

Five Items to Focus On

1. Earning

Your income is your biggest tool in this stage. Whether you’re working your first job, freelancing, or pursuing a side hustle, think about ways to grow your earnings. Can you negotiate a raise? Learn a new skill to boost your career prospects? Every dollar you earn gives you more flexibility to manage your financial goals.

2. Budgeting (Or Something Close)

If the word “budget” makes you cringe, don’t worry—this doesn’t have to mean tracking every penny. The goal here is to understand where your money is going. In future lessons, you’ll learn what a budget is and how to create a budget and analyze where you’re at. For now, just understand the importance of knowing how you spend and save your money.

3. Saving

Even if it’s just a little, start setting money aside regularly. Your first goal is to start building a savings account—anything you can save is great and will be there if something unexpected happens, like losing a job or facing a big repair bill. This cushion is what keeps financial stress at bay. We’ll talk about all the ins and outs of savings accounts in an upcoming lesson.

4. Paying Down Debt

If you have credit card debt or student loans, make a plan to tackle them. High-interest debt like credit cards can feel like a weight on your shoulders, so prioritize paying those off while still saving a little.

5. Starting to Invest

Investing doesn’t have to be complicated or scary. Start small, like contributing to a 401(k) through your job or opening an IRA (Individual Retirement Account). Even a little can grow over time and be there for you when you decide to retire.

Challenges in This Chapter

- It’s easy to feel like there’s too much to do and not enough money to do it all. Start with small, actionable goals to build confidence.

- As you earn more, it’s tempting to spend more. Keep your spending in check so you can stay focused on your bigger goals.

-

EXAMPLE

Example 1: Starting Your First Job

- Situation: You just got your first full-time job and are excited about finally earning a steady paycheck.

- What to Do: When your employer asks how you want to get paid, you choose direct deposit so your paycheck goes straight into your bank account. You decide to save $50 from each paycheck in a separate savings account for emergencies, like car repairs or unexpected bills. Your employer also offers a retirement savings plan, called a 401(k), and they’ll add money to it if you do. You start small, contributing 5% of your paycheck so you don’t miss out on the free money.

Example 2: Dealing With Debt

- Situation: You have $25,000 in student loans and a $1,200 balance on your credit card. The credit card feels like a weight hanging over you because the payments barely make a dent.

- What to Do: You decide to tackle the credit card first because it has the highest interest rate (that’s the extra money the credit card company charges you for borrowing). You commit to paying an extra $100 each month to knock it out faster. Once the credit card is paid off, you’ll focus on paying more toward your student loans.

Example 3: Learning to Budget

- Situation: You notice that most of your paycheck disappears by the end of the month, and you’re not sure where it all goes. You want to start saving but feel like you don’t have any money left.

- What to Do: You download a free budgeting app that tracks your spending. After a week, you realize you’re spending $300 a month on takeout. You decide to cook at home more often, which saves you $200 a month. You put that extra money into your savings for future goals or emergencies.

This stage is all about learning, experimenting, and building habits. It’s okay to make mistakes—what matters is that you keep moving forward. Now, let’s look at the next life stage, protecting what you’ve built.

1b. Protecting What You’ve Built

Once you’ve built a solid foundation for your finances, the next step is to protect what you’ve worked so hard to achieve. Think of this as the stage where you’re starting to feel more settled in life. You might have a steady job, a family to support, and maybe even a house. But with more responsibilities come new challenges, and it’s important to make sure your finances are prepared for whatever life throws your way.

This stage often happens in your 40s or 50s, but it could start earlier depending on your situation. At this point, your money situation might feel a little more complicated, and the stakes are higher because you’ve got more to lose. That’s why this stage is all about protecting and maintaining what you’ve built.

Four Items to Focus On

1. Insurance (Your Safety Net)

Life can be unpredictable, and insurance is your way of being prepared for the unexpected. Think of it as a financial safety net. There are a few types of insurance to consider:

- Health Insurance: Covers medical expenses so one unexpected hospital visit doesn’t wipe out your savings

- Life Insurance: Ensures your loved ones will be taken care of financially if something happens to you

- Disability Insurance: Provides income if you can’t work due to an illness or injury

- Long-Term Care Insurance: Helps cover the cost of things like nursing homes or in-home care as you get older

These policies might feel like an extra expense, but they provide peace of mind for you and your family.

2. Saving for Retirement

If you haven’t started seriously saving for retirement yet, now’s the time. Retirement might seem far off, but the earlier you save, the easier it is to reach your goals. Use accounts like a 401(k) (offered by some employers), IRA, or Roth IRA to set aside money. These accounts help your money grow over time, so you’ll have something to live on when you stop working.

If you’re unsure how much you should be saving, a financial advisor can help you make a plan that works for you.

3. Adjusting Your Investments

When you’re younger, you might take more risks with your investments because you have time to recover from ups and downs in the market. But as you get closer to retirement, it’s a good idea to play it a little safer. That means moving some of your money into more stable investments, like bonds, that don’t change as much when the stock market fluctuates. This helps protect the money you’ve worked hard to save.

-

You’ll learn all about investing in stocks, the stock market, and bonds later in the course.

4. Big-Picture Planning

At this stage, you’re starting to think about bigger goals. Do you want to pay off your mortgage? Help your kids with college? Save for a dream retirement? Now’s the time to get clear on those goals and make a plan to reach them.

It’s also smart to start thinking about estate planning. That means making sure your assets (like your home, savings, or investments) will go where you want them to after you’re gone. Even if retirement feels far away, having a plan now will make things easier later.

Challenges You Might Face

- Unexpected Expenses: Life doesn’t always go according to plan. A medical emergency, job loss, or major home repair can throw a wrench in your finances if you’re not ready for it. Having a solid emergency fund and the right insurance can help you weather these surprises.

- Balancing Competing Goals: You might feel pulled in a million directions—saving for retirement, helping your kids pay for college, or taking care of aging parents. It can be overwhelming but remember: you don’t have to do it all at once. Focus on what’s most important right now, and tackle one goal at a time.

This part of your financial journey is about keeping things steady. You’ve worked hard to build a foundation, and now it’s time to protect it so you’re ready for whatever comes next. Taking these steps now will give you more peace of mind and help you stay focused on what matters most—your family, your future, and your goals.

-

EXAMPLE

Example 1: Buying a Home

- Situation: You and your partner are ready to buy your first house. You’re excited but nervous about taking on such a big expense.

- What to Do: Before you buy, you talk to a lender who explains how mortgages work (a mortgage is a loan you take out to buy a home). You compare different mortgage options to find one with a low monthly payment. You also get homeowner’s insurance, which protects you financially if something happens to your house, like a fire or storm damage. To stay on track, you create a budget to make sure you can handle the new costs, like property taxes and maintenance.

Example 2: Thinking About Retirement

- Situation: You’re 45, and you’ve been saving for retirement, but you’re not sure if it’s enough. You’re starting to think more about what life will look like when you stop working.

- What to Do: You meet with a financial advisor (a professional who helps people with money decisions) who helps you figure out how much you’ll need to retire comfortably. They recommend increasing how much you’re saving each month into your retirement account and adjusting your investments to make them less risky as you get older.

Even if it feels like a lot, you don’t have to figure it all out at once. Start with small steps, like reviewing your insurance or contributing a little more to your retirement account, and build from there. The more you plan now, the more confident you’ll feel about your financial future. Now, let’s look at the third stage, leaving a legacy.

-

- Financial Advisor

- A professional who helps you manage your money.

1c. Leaving a Legacy

When we talk about leaving your legacy, we’re not just talking about money. This stage is about making sure the things you’ve worked hard for—your savings, your home, your investments—are passed on to the people or causes you care about in a way that feels meaningful and smooth.

This stage might seem far away, especially if you’re still building your finances. But it’s never too early to start thinking about what happens to your money and assets after you’re gone. Taking steps now can save your loved ones a lot of stress and ensure your wishes are carried out exactly the way you want.

Five Items to Focus On

1. Make a Will (It’s Simpler Than You Think)

A will is a legal document that says who gets what when you pass away. It doesn’t have to be fancy or expensive—you can even create one online. Without a will, your assets (like your home or savings) might go through a complicated legal process called probate, which can take a long time and cause unnecessary stress for your loved ones.

In your will, you can:

- Decide who gets your money, property, or personal items

- Name a guardian for your children if they’re still minors

- Specify any special instructions, like leaving money to a charity or setting up a fund for your grandkids’ education

2. Name Beneficiaries

For accounts like life insurance, retirement accounts (like a 401(k) or IRA), and even some bank accounts, you can name beneficiaries—people who will automatically get the money if something happens to you. This is an easy way to make sure your money goes where you want it to without needing to go through probate.

3. Set Up a Trust (If You Need One)

A trust is like a special container for your assets that lets you have more control over how they’re distributed. For example, if you want to leave money to your kids but want to make sure they use it for college or receive it at a certain age, a trust can help. It’s not necessary for everyone, but if you have specific goals or a lot of assets, it’s worth exploring with a financial or legal advisor.

4. Have Open Conversations With Your Family

Talking about money can feel awkward, but it’s important to let your family know your plans. For example, if you want to leave money for your grandkids’ education, tell your kids so there’s no confusion later. These conversations help prevent misunderstandings and make things easier for everyone.

5. Consider Giving While You’re Alive

Leaving a legacy doesn’t have to wait until you’re gone. If you’re financially comfortable, consider giving to your loved ones or favorite causes now. This could mean helping a family member with a down payment on a house, starting a college fund for your grandkids, or donating to a charity that’s close to your heart.

If you don’t have a plan, the government will decide how your assets are distributed—and that might not align with your wishes. Planning ahead ensures the people you care about are taken care of and helps avoid unnecessary stress for your family.

Challenges You Might Face

- Procrastination: It’s easy to put this off because it feels like a “later” problem. But getting started now—writing a simple will or naming beneficiaries—can save your loved ones a lot of trouble down the road.

- Family Disagreements: Money can be a sensitive topic. Clear communication and proper planning can help avoid arguments or confusion after you’re gone.

- Overthinking It: You don’t have to make everything perfect right away. Start with the basics, like naming beneficiaries and writing a will. You can always make updates as your life and finances change.

Leaving your legacy might feel like a big, complicated idea, but it’s really just about making things easier for the people you care about. Start small—write a will, update your beneficiaries, and have an open conversation with your family.

These simple steps can help ensure that what you’ve worked hard for goes exactly where you want it to, giving you peace of mind and leaving behind a lasting impact. Remember, it’s not just about money—it’s about making sure your values and priorities live on.

-

EXAMPLE

Example 1: Writing a Will

- Situation: You’re in your 60s, and you’ve worked hard to save money, buy a home, and build a comfortable life. You want to make sure your family knows what to do with your things when you’re gone.

- What to Do: You write a will (a document that says who gets your money, house, or personal items). You decide to leave your home to your kids and some savings to your grandkids for college. You also name someone you trust to handle your affairs, called an executor. This way, your family doesn’t have to guess what you wanted.

Example 2: Talking With Family

- Situation: You’ve decided to leave money for your grandkids’ education, but you realize your kids might not know your plans.

- What to Do: You sit down with your family and explain what you’re planning so there’s no confusion. You tell them why you think education is important and how you want to help the grandkids in the future. Having this conversation helps avoid misunderstandings later.

Stage 3 is all about leaving your legacy, but the truth is, what you focus on changes as you move through different stages of life. What matters when you’re starting out isn’t the same as when you’re planning for the future. That’s why understanding your life stage is so important—it helps you focus on what’s most important right now without getting overwhelmed by everything else. Let’s talk about why knowing where you are in your financial journey makes all the difference.

-

- Will

- A legal document that states how you want your assets distributed and who will care for minor children after your death.

- Probate

- The legal process of validating a will, settling debts, and distributing assets to beneficiaries.

- Beneficiaries

- The people named to receive assets from a will, trust, or insurance policy.

- Trust

- A legal arrangement where a trustee manages assets for the benefit of beneficiaries.

2. Why Your Life Stage Matters

No matter where you are in your financial journey, knowing your life stage is like having a map for your money. It helps you focus on what’s most important right now instead of feeling overwhelmed by everything you “should” be doing. Each stage has unique challenges and priorities, and understanding where you are allows you to make better decisions and feel confident about your progress.

Why It’s Important

- Keeps You Focused on the Right Goals:

- If you’re just starting out, you don’t need to worry about complex estate planning. Instead, focus on building good habits like saving and budgeting. If you’re nearing retirement, it’s less about growth and more about protecting what you’ve built.

- Knowing your stage helps you put your energy into actions that matter most for you right now.

- Reduces Overwhelm:

- Personal finance can feel like a million different things to do at once—save, invest, pay off debt, buy a house, save for retirement. But when you know your life stage, you can break it down into manageable steps.

- For example, someone in the “building your foundation” stage should prioritize paying off high-interest debt and starting small with savings instead of worrying about investing in complex financial tools.

- Prepares You for the Next Stage:

- Each stage builds on the one before it. By focusing on the right priorities now, you set yourself up for success in the future. For instance, building an emergency fund in your 20s gives you a safety net that helps you in your 40s when you might face unexpected expenses like home repairs or medical bills.

- Helps You Adapt to Change:

- Life doesn’t always go according to plan—job changes, starting a family, or unexpected expenses can shift your financial needs. Knowing your stage helps you adjust quickly and stay on track.

- Keeps You Aligned With Your Values:

- As you move through life, your goals and priorities will change. Understanding your life stage helps you align your money decisions with what truly matters to you, whether that’s building stability, creating freedom, or leaving a legacy.

-

Take a few minutes to think about where you are in your financial journey. Use these questions to guide you:

- What are your biggest financial goals right now?

- Are you focused on building savings, paying off debt, protecting what you’ve built, or planning for the future?

- What challenges are you facing?

- Are you juggling bills, trying to save for retirement, or figuring out how to make your money last?

- What feels most important to you right now?

- Is it creating stability, growing your wealth, or making sure your family is taken care of?

Write down your answers and take note of what stage aligns with your current priorities. This reflection can help you focus on the financial actions that matter most for where you are today.

Understanding your life stage is like having a financial GPS—it points you toward what’s most important right now, helps you avoid unnecessary stress, and keeps you on track toward your goals. No matter where you are in your journey, the key is to focus on what’s right for you at this moment while staying flexible enough to adapt as life changes.

In this lesson, you learned about the life stages of personal finance, including building your foundation, protecting what you’ve built, and leaving a legacy. You also now understand why your life stage matters in your personal finance journey.