In this lesson, you will learn about the types of life insurance policies and how to develop a plan for optimal life insurance coverage. You will better understand how problem solving and technology skills can help you determine the coverage you need. Specifically, this lesson will cover:

1. The Basics of Life Insurance

Before jumping into the details of life insurance, you need to know the basics. Essentially, there are three parties to a life insurance contract.

-

When you decide to purchase an insurance policy, you need to decide who owns the policy, who is the insured, and who will be the beneficiary.

- The policy owner is the person who makes premium payments. Recall that a premium represents the cost of insurance.

- The insured is the person that must die for the policy to pay off (most often, the policy owner is the insured but not always). If you want to buy an insurance policy naming someone else as the insured, you must prove an insurable interest before purchasing the policy. An insurable interest means that if the insured individual were to die unexpectedly, the policy owner would suffer a financial loss. Family members, business partners, and employers typically can show an insurable interest.

- The beneficiary is the person or entity that receives the policy death benefit when the insured dies. Policy owners may also list contingent beneficiaries. These individuals will receive the death benefit if the primary beneficiary dies before the policy owner. For example, a husband might own a policy and be the insured individual, with his wife as the beneficiary and his children as the contingent beneficiaries.

It’s generally best to have two of the three parties in a life insurance policy be the same person. Most often this means that the policy owner is also the insured individual, as shown in the illustration below.

Risk is a normal part of life. Although we can’t control the world around us, we can use our problem solving skills to take steps to lessen the aftermath of an unexpected event. Purchasing life insurance is one way to mitigate risk and to ease the financial burden of an unplanned hardship.

-

- Life Insurance

- Provides a tax-free, lump-sum insurance benefit that can be used to pay final expenses, burial costs, debts, and other expenses.

- Policy Owner

- The person who makes premium payments. Recall that a premium represents the cost of insurance.

- Insured

- The person that must die for the policy to pay off (most often, the policy owner is the insured but not always).

- Beneficiary

- The person or entity that receives the policy death benefit when the insured dies.

- Insurable Interest

- If the insured individual were to die unexpectedly, the policy owner would suffer a financial loss. Family members, business partners, and employers typically can show an insurable interest.

2. Types of Life Insurance

Although the process of life insurance may seem straightforward, the market for coverage is complex. There are two types of life insurance products to choose from, each of which offers several options.

- Term life insurance

- Cash value life insurance

2a. Term Life Insurance

Most consumer advocates recommend that you purchase term life insurance unless you have a special need, such as a preexisting medical condition, a disabled child, or a complex family situation. Term life insurance (also known as pure term insurance) provides only a death benefit if the insured individual dies before reaching a predetermined age. If you buy term life insurance, here’s what to expect.

-

Term life insurance is usually recommended by consumer advocates because of its low cost, which allows a policy owner to buy ample coverage.

- The death benefit will equal the face value of the policy, which is the initial dollar amount of insurance that you select (as the policy owner) to be paid to the beneficiary upon the insured’s (most likely you) death. For example, you might buy a policy with a face value of $25,000, $100,000, or even $1,000,000 or more.

- As the name implies, your beneficiary only gets paid if you die within the “term” of the policy. A term can be as short as 1 year or as long as 30 or 40 years. An annual renewable term policy needs to be purchased yearly, whereas a level term policy is purchased for periods ranging from 5 to 30 or more years.

- Term insurance tends to be inexpensive, but you will need to qualify for the right to purchase insurance. This means that the insured – which could be you or someone else – must be in reasonably good health. The good news is that many employers provide term insurance as an employee benefit, in which case even those in poor health can still obtain insurance coverage.

- As you age, the cost of term insurance increases. For example, a 20-year $100,000 term policy for a healthy 30-year-old can be purchased for as little as $150 per year; the same policy for a 50-year-old might cost $600 per year.

-

- Term Life Insurance

- Provides only a death benefit if the insured individual dies before reaching a predetermined age. Also known as pure term insurance

- Face Value

- The initial dollar amount of insurance that you select (as the policy owner) to be paid to the beneficiary upon the insured’s (most likely you) death.

2b. Cash Value Life Insurance

Although term life insurance is generally recommended by consumer advocates – term insurance is inexpensive and flexible – there may be times in your life when you want insurance that is more permanent. When this happens, your second option is to purchase a cash value life insurance policy. A cash value life insurance policy is one that blends pure term insurance with a savings option (see Hint below). Why might you prefer a cash value policy? Well, the cash value grows on a tax-deferred basis. Also, you may borrow from the account without a credit check and, like all life insurance, benefits paid to your beneficiary are received on a tax-free basis.

-

Insurance agents sometimes call cash value insurance

permanent insurance.

Reasons to Use a Cash Value Policy.

A cash value policy often appeals to individuals who need to force themselves to save money. Also, consider the following:

- It is possible to borrow the cash value without a credit check; a portion of the interest paid on the loan goes back into the insurance policy.

- It is also possible to cancel or surrender a policy and gain access to the unused portion of “cash” in the policy. However, you might owe taxes on the distribution if the amount taken from the account exceeds the premiums paid into the account.

These types of policies are widely used by business owners and others who need to shelter large sums of money in tax-advantaged accounts. Cash value policies also provide lifetime coverage that can be used to pay for the needs of disabled family members in case the family breadwinner dies unexpectedly.

- A cash value policy provides the ability to leave a generous sum to a charity or family members on a tax-free basis.

- A cash value policy preserves insurability in case you become ill in the future.

- A cash value policy provides estate liquidity for those with significant wealth.

Why to Avoid Cash Value Policies.

A significant disadvantage of cash value policies is that these policies cost much more than similar term policies. For example, a $100,000 guaranteed lifetime (to age 100) term policy might cost about $300 per year. The premium on a basic $100,000 cash value policy, on the other hand, could be $2,000 to $5,000 yearly. Further, if you should cancel or surrender your policy before death, you may pay a substantial surrender penalty on any cash taken from the account. Most surrender penalties, however, disappear after 7 to 10 years.

-

- Cash Value Life Insurance Policy

- Blends pure term insurance with a savings option.

3. Do You Need Life Insurance?

Now you know a bit about the different types of life insurance available in the marketplace. But you may be asking yourself, "Do I really need it?" You should consider buying some coverage if you answer yes to any of the questions in the following illustration.

Keep in mind that even if you answered no to each question in the previous questionnaire, you should take advantage of purchasing insurance through your employer for the following reasons:

- You cannot be denied because of a medical condition and premiums tend to be low.

- Your employer will sometimes provide a baseline level of coverage at no cost to you.

-

If you leave employment, however, you will likely lose your life insurance coverage.

It’s important to understand how to analyze the cost of purchasing (or not purchasing) insurance protection and to think critically about this cost before you make a decision. To make insurance choices, you’ll need your technology skill to track, visualize, and understand risk data.

3a. Life Insurance Premiums

Recall that premiums are based on the face value of the policy and health factors of the insured individual. The greater the face value, the higher the premium. Similarly, more negative health factors experienced by the insured individual will also drive up the price of a policy. You might be surprised by some of the things that will cause your insurance premium to increase. The illustration below shows six common premium escalators.

3b. How Much Life Insurance Do You Need?

Insurance companies are for-profit businesses. It is in their interest to sell you the most insurance possible. At the same time, it is in your interest to buy the right amount of coverage. Remember, you do not want to be insurance-rich but cash-poor. You need just enough insurance to meet your needs. It turns out that there are numerous ways to calculate an insurance need. Here are a few examples.

- Complex needs analyses, which require calculating present values of future cash flows and adding together all current debts, bills, and liabilities. These calculations are the most accurate estimates of life insurance needs and are based on unique individual and family circumstances.

You can use an app to do these calculations.

- Income multiplier estimation, which is simply your current income multiplied by 10 and decreased by any current insurance you may currently have. For example, if you earn $35,000, you need about $350,000 in coverage. If you already have $150,000 in coverage from your employer-provided life insurance, you need an additional $200,000 life insurance policy. It is that simple!

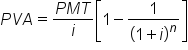

- Human life value approach, which is essentially a time value of money calculation. Here is the formula:

-

- Present Value of an Annuity

In this formula:

-

PVA is the present value of an annuity.

-

PMT is your current income.

-

i is the current interest rate you can earn on investments.

-

n is the estimated number of years your beneficiary will need income.

IN CONTEXT

Using the previous example, let’s say that you earn $35,000 and that a diversified investment portfolio can generate a 6% annual return. If your beneficiary will need income for 25 years, you should purchase an insurance policy with a face value of approximately $450,000, as the following calculation shows.

-

You can also do this on your calculator by inputing 25 for

n, 6 for

i, 35,000 for

PMT, and then computing

PVA.

In this lesson, you learned about the basics of life insurance. The two primary types of life insurance are term life insurance and cash value life insurance. Term life insurance provides a death benefit should the insured pass away. Cash value life insurance blends term life insurance with a savings option. Consumers who have difficulty saving money on their own might choose this insurance option. Your problem solving and technology skills can help you determine what will work best for you.

Here’s the main question: Do you need life insurance? Complete the life insurance need questionnaire to find out. Having a spouse, children, debts, or large tax liabilities are just several reasons for getting life insurance. Remember, your premiums are higher if you lead an unhealthy or risky lifestyle. You might also be asking, “How much life insurance do I need?” There are numerous ways to calculate your need, three of which you saw in this lesson.

Source: This content has been adapted from Chapter 9.4 of Introduction to Personal Finance: Beginning Your Financial Journey. Copyright © 2019 John Wiley & Sons, Inc. All rights reserved. Used by arrangement with John Wiley & Sons, Inc.

Wiley and the Wiley logo are trademarks or registered trademarks of John Wiley & Sons, Inc. and/or its affiliates in the United States and other countries.