Table of Contents |

You may recall from earlier in this challenge that the main goal of inventory management is determining the optimal amount of inventory to keep for both salable goods and the raw materials to make them. There are several strategies for calculating these levels.

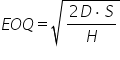

One of the oldest is economic order quantity (EOQ), a process for determining the optimal amount of an item to order at one time to minimize holding costs (also referred to as carrying costs), the amount it costs to keep a unit in inventory, including storage, depreciation (loss of value over time), and shrinkage (theft, damage, etc.). Effective inventory control is paramount for optimizing profitability. Holding costs, the expenses associated with storing unsold inventory, can significantly impact a company's bottom line. These costs encompass storage space, labor for managing inventory, insurance, taxes, and potential obsolescence or spoilage of goods.

Holding costs are determined by multiplying the cost of an item by a known percentage, usually about 20% for nonperishable goods, which itself is determined by dividing total inventory costs by total value of inventory. Some of the specific components of holding costs include the cost of storage, such as the cost of rent for a warehouse, insurance on the goods stored in the warehouse, inventory handling costs, such as the maintenance of forklifts to move inventory, depreciation costs, such as the costs associated with obsolescence or spoilage, and the cost of the capital, which is the interest on funds used to finance the inventory (if applicable).

are all part of holding costs.")

EXAMPLE

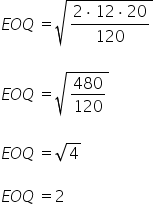

A bicycle store determines that the value of inventory over a year divided by inventory costs is 20%. A bicycle that costs $600 would have a holding cost of $120 ($600*20%).Determining the EOQ, like any inventory management technique, requires good data. The values the manager needs to know, and the variables we will assign to them, are:

While EOQ is relatively easy to find using a calculator, it has some limitations. Underlying assumptions are:

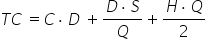

The EOQ formula considers an optimal order quantity for a single product. However, there are a number of other questions an inventory manager might have, such as how often to place orders. Another formula they can use is the total cost formula to determine annual inventory costs. The total cost formula determines the total cost for ordering items. An inventory manager can change variables within the formula to see how changes in practice will affect the total cost.

Recall the three values we used to determine EOQ (the optimal quantity to keep in inventory):

However, each of these items must be calculated first.

IN CONTEXT

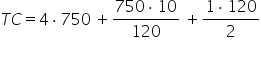

Let’s return to the bicycle shop and consider a product sold in higher quantity, bicycle locks. The store sells 750 locks a year. The locks are ordered in batches of 40 for $4 per item, have a modest setup fee of $10 per order, and a holding cost of $1 per lock (15% of the retail cost). The shop has already determined the EOQ is 120 (rounded down to a factor of 40, since they are sold in packs of 40).

To determine the total holding cost, let's plug the numbers into the formula.

We can calculate the total cost for this item at $3,000 (the purchasing cost, 750*4) plus $62.50 (the ordering cost, 750*10/120), plus $60 (the holding cost, 1 x 120/2). The total cost is thus $3,122.50.

The formula can be used to help determine how changes in practice would impact the total cost. For example, the bicycle store might wonder if they should order 240 locks at a time instead of 120. The cost per lock is slightly cheaper with larger orders, at $3.90 per unit instead of $4.00. This change would double the setup costs, since it takes twice as long to ship, unpack, price, and shelve twice as many locks. The holding costs also go up since the locks are taking up more space, and the store must drop another item to make room. These are called opportunity costs, the loss of potential gain from alternative use of resources. For these reasons, the holding cost will be $1.50 per lock instead of $1.00.

How would doubling the quantity ordered affect total cost? We can insert the new numbers into the formula to find out.

The purchasing cost at the expanded order size will be $2,925. Although the quantity per order is increased and the setup cost per order has increased, these are offset by fewer orders, so the order cost is the same. Finally, the holding costs are increased due to opportunity costs.

The total cost now adds up to $3,167.50, which is more than their current total cost, despite the discount for a larger order. This is due to opportunity cost—that is, the larger orders would mean dropping another product to make room on the shelf for more locks.

The examples above are for nonperishable goods, but for many situations across the supply chain, there are some materials or products that require special handling, special storage, or which must be used immediately. Materials management is a field within operations management that specializes in procurement and storage of a variety of materials, some that require special handling.

ABC analysis is an inventory categorization technique often used in material management. It is also known as “selective inventory control.” The essence of ABC analysis is to assign grades to materials based on the need for control and recordkeeping.

EXAMPLE

A restaurant will have some items that are high cost, require refrigeration, and must be used immediately, such as meat and seafood. These A items are also the most crucial to the menu and daily operations of the restaurant. B items, like onions and potatoes, would have a longer shelf life and may not require refrigeration, but still must be used within a certain timeframe. C items would have a very long shelf life, such as dry grains, salts, and oils.A items are very important for a business. Because of the high value of these A items, frequent value analysis is required. In addition to that, a business needs to choose an appropriate order pattern (e.g., “just-in-time”) to avoid excess capacity.

B items are important, but less important than A items; they may require modest analysis but will not have as much impact on total costs.

C items are least important, at least in terms of inventory management. They tend to be less expensive items that have a long life and can be stored in large quantities.

The use of an ABC analysis can help set different holding costs for items that are more expensive, cost more to store, and have more risk (such as meat and seafood going bad). ABC analysis is also crucial to purchasing schedules. A store without an ABC inventory model is likely to have uniform purchasing, where all materials are ordered on the same schedule, such as once a month. A store using an ABC model is likely to have weighed purchasing, where each category has its own schedule.

EXAMPLE

A restaurant might make A purchases (meat, seafood, dairy, etc.) every 2–3 days, B purchases (fruits, vegetables, etc.) once a week, and C purchases (dry goods, oils, etc.) once a month. As you’ve guessed, making a “mistake” and over-ordering or under-ordering C purchases does not have much impact, while making a mistake on A purchases could mean the restaurant runs out of critical menu items!As we learned earlier, just-in-time (JIT) is a production strategy striving to optimize costs by reducing in-process inventory and associated holding costs. While the JIT process might seem to be the simple practice of operating without (much) inventory, it still relies on inventory management of the resources used to make their goods. For the materials manager, this is quite different from a more traditional inventory method.

EXAMPLE

If Gordon decides on a JIT system for his bicycle company, he will need less space and lower costs, but he will need to be in constant contact with suppliers and runs the risk of production halting if any component is not delivered promptly.In terms of day-to-day work, the inventory manager for a JIT manufacturer will be on the floor most of the day, receiving and directing supplies. They will likely be on the phone calling suppliers throughout the day. A more traditional manager would do more long-term planning from their office, determining holding costs, scouting out suppliers, and perhaps overseeing occasional shipments at the warehouse.

To achieve continuous improvement, it is crucial to have good communication between the materials manager and the workers they support. For example, a shop may use a Kanban system; taken from the Japanese word for signboard, a Kanban system is any highly visual project management tool that communicates where a product is in the production cycle, as well as any needs that must be filled by the materials manager. This may be as simple as a highly organized shelving system so the materials manager can see what materials are low in stock, but it may be a digital system where materials are scanned, and the materials manager can receive an alert when a material falls below a certain level. Whatever the system, it is crucial for clear and reliable communication from employees, whether it is remembering to scan materials so inventory measures are accurate or some other visual queue, even a brightly colored sticky note on the shelf that needs refilling.

Implemented correctly, JIT focuses on continuous improvement and can improve a manufacturing organization’s return on investment, quality, and efficiency. There are other advantages and disadvantages to a just-in-time system not directly related to inventory or materials management.

Source: This tutorial has been adapted from Saylor Academy and NSCC “Operations Management”. Access for free at https://pressbooks.nscc.ca/operationsmanagement2/. License: Creative Commons Attribution 4.0 International.