In this lesson, we will discuss the purposes of the statement of cash flows, its uses, and what information it provides. Specifically, we will discuss the following:

The statement of cash flows is one of three financial statements required for external reporting, the other two being the balance sheet and income statement. While the income statement and balance sheet provide information pertaining to a business’s operating performance and financial position, the statement of cash flows evaluates events that create a change in the amount of cash that is available to the company.

Our study of the statement of cash flows will focus on activities that impact the inflow and outflow of cash and the ability of a company to maintain a sufficient cash balance throughout a given period.

events to know

In November 1987, the Financial Accounting Standards Board issued Statement of Financial Accounting Standards No. 95, “Statement of Cash Flows.” The Statement became effective for annual financial statements for fiscal years ending after July 15, 1988. Since then, the statement of cash flows has been one of the major financial statements issued by a company. The statement of cash flows replaced the statement of changes in financial position, on which funds were generally defined as working capital. Working capital is equal to current assets minus current liabilities.

The main purpose of the statement of cash flows is to report on the cash receipts (inflows) and cash disbursements (outflows) of an entity during an accounting period. Broadly defined, cash includes both cash and cash equivalents, such as short-term investments. Another purpose of this statement is to report on the entity’s investing and financing activities for the period. The statement of cash flows reports the effects on cash during a period of a company’s operating, investing, and financing activities. A separate schedule is used by firms to show the effects of significant investing and financing activities that do not affect cash.

The statement of cash flows summarizes the effects on cash of the operating, investing, and financing activities of a company during an accounting period; it reports on past management decisions on such matters as the issuance of capital stock or the sale of long-term bonds. This information is available only in bits and pieces from the other financial statements. Since cash flows are vital to a company’s financial health, the statement of cash flows provides useful information to management, investors, creditors, and other interested parties.

By reviewing the statement, management can see the effects of its past major policy decisions in quantitative form. The statement may show a flow of cash from operating activities large enough to finance all projected capital needs internally rather than having to incur long-term debt or issue additional stock. Alternatively, if the company has been experiencing cash shortages, management can use the statement to determine why such shortages are occurring. Using the statement of cash flows, management may also recommend to the board of directors a reduction in dividends to save cash.

The information in a statement of cash flows assists investors, creditors, and others in assessing the following:

A company’s ability to generate positive future net cash flows

A company’s ability to meet its obligations

A company’s ability to pay dividends

A company’s need for external financing

The reasons for differences between net income and associated cash receipts and payments

The effects on a company’s financial position of both its cash and noncash investing and financing transactions during the period (disclosed in a separate schedule)

terms to know

Statement of Cash Flows

A required financial statement that shows the amount of cash that flows in and out of a company.

Working Capital

The amount of current assets minus current liabilities that is used in daily operations.

Cash Equivalents

Short-term investments that can easily and quickly be converted into cash, such as treasury bills and money market accounts.

2. The Structure of a Statement of Cash Flows

Both U.S. Generally Accepted Accounting Principles (GAAP) and the International Financial Reporting Standards (IFRS) require that companies prepare the statement of cash flows in a uniform way by classifying cash receipts and disbursements as either operating, investing, or financing activities. Both inflows and outflows are included within each category.

EXAMPLE

Here is what a statement of cash flows can look like:

Example of a Statement of Cash Flows

2a. Cash Inflows and Outflows of Operating Activities

Operating activities generally include the cash effects (inflows and outflows) of transactions and other events that enter into the determination of net income. Cash inflows and outflows from operating activities affect items that appear on the income statement.

The cash inflows and outflows from operating activities include:

Cash Inflows from Operating Activities

Cash Outflows from Operating Activities

Cash receipts from sales of goods or services

Interest received from making loans

Dividends received from investments in equity securities

Cash received from the sale of trading securities

Cash receipts from lawsuits, proceeds of certain insurance settlements, and cash refunds from suppliers

Cash paid to vendors for merchandise

Cash paid to vendors for supplies

Cash paid for general expenses needed to operate the business including rent, utilities, etc.

Cash paid for employee salaries and wages

Cash payments for interest and taxes

The format in the operating activities section differs for the direct and indirect methods. The direct method adjusts each item in the income statement to a cash basis by deducting only the operating expenses that are paid in cash from cash sales. The indirect method makes these same adjustments but to net income rather than to each item in the income statement. It is performed by adjusting net income for items that affected net income but did not involve cash. Both methods eliminate not only the effects of non-cash items, such as depreciation, but also gains and losses on sales of plant assets. A large majority of companies use the indirect method. We will discuss each of these methods in later lessons.

2b. Cash Inflows and Outflows of Investing Activities

Investing activities generally include transactions involving the acquisition or disposal of noncurrent assets.

The cash inflows and outflows from investing activities include:

Cash Inflows from Investing Activities

Cash Outflows from Investing Activities

Sale of property, plant, and equipment

Sale of long-term investments (stocks and bonds)

Collecting the principal on loans made

Purchase of property, plant, and equipment

Purchase of long-term investments (stocks and bonds)

Lending money

2c. Cash Inflows and Outflows of Financing Activities

Financing activities generally include the cash effects (inflows and outflows) of transactions and other events involving creditors and owners.

The cash inflows and outflows from financing activities include:

Cash Inflows from Financing Activities

Cash Outflows from Financing Activities

Borrowing money from a lender

Cash received from issuing capital stock, bonds, mortgages, and notes

Repaying the principal amount borrowed from a lender

Purchase of treasury stock

Paying cash dividends

Payment of interest is not included because interest expense appears on the income statement and is, therefore, included in operating activities. Cash payments to settle accounts payable, wages payable, and income taxes payable are not financing activities. These payments are included in the operating activities section.

terms to know

Operating Activities

Business activities that include the cash effect of transactions and other events that enter into the determination of net income.

Direct Method

An accounting method used to prepare the statement of cash flows that deducts only the operating expenses that are paid in cash from cash sales.

Indirect Method

An accounting method used to prepare the statement of cash flows by adding or subtracting the differences between noncash activities from the net income.

Investing Activities

Business activities that include transactions involving the acquisition or disposal of noncurrent assets.

Financing Activities

Business activities that include transactions with creditors and owners.

3. Steps for Preparing a Statement of Cash Flows

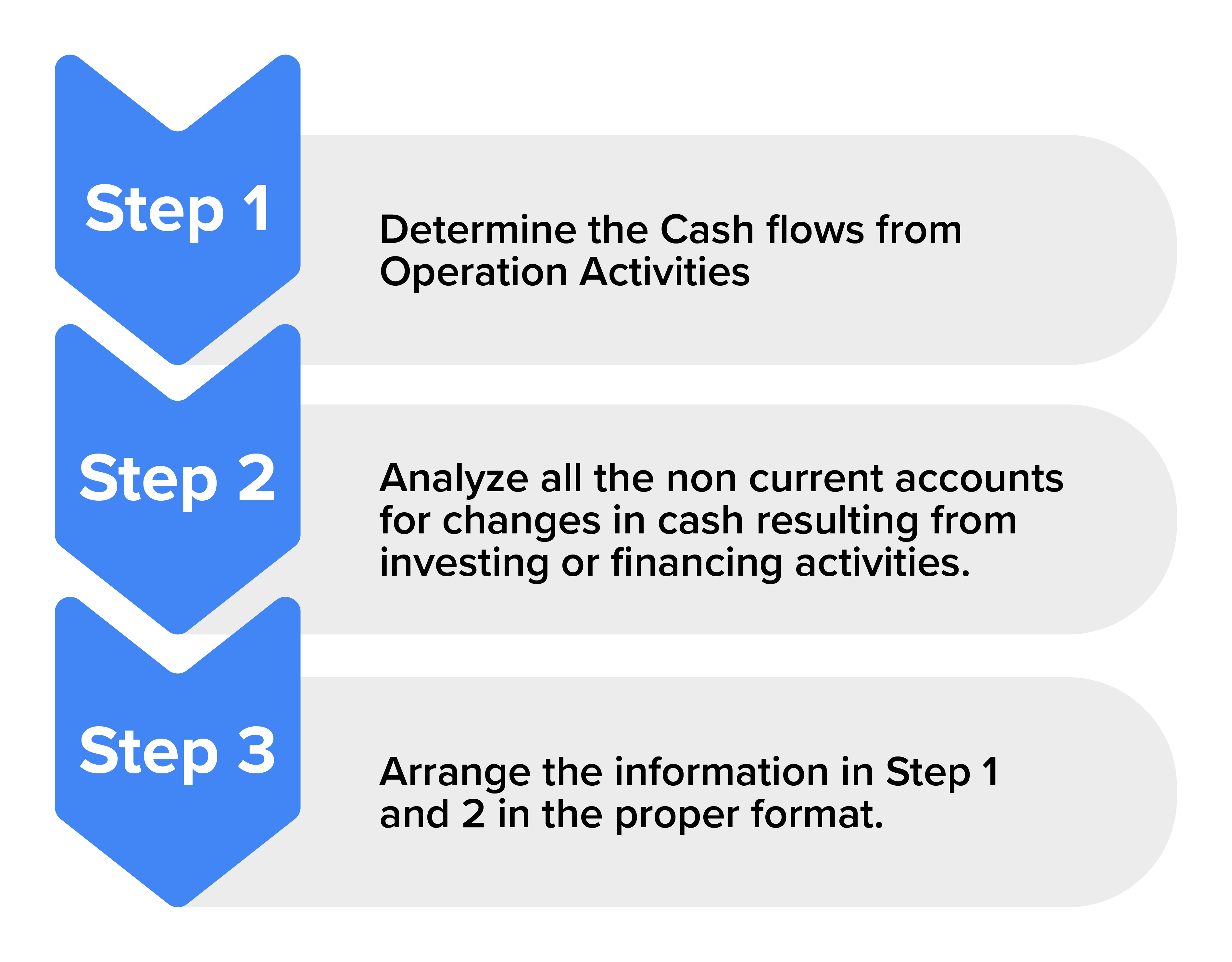

Accountants follow specific procedures when preparing a statement of cash flows.

step by step

Determine the cash flows from operating activities. Either the direct or indirect method may be used. The direct method of calculating cash flows involves adding all the cash collections from operations and subtracting all of the cash disbursements from operations. The indirect method begins with the net income from the income statement and makes adjustments to undo the impact of the accruals made during the period. Both direct and indirect methods will yield the same number.

Analyze all the noncurrent accounts for changes in cash resulting from investing and financing activities. Investing activities detail cash flows stemming from the buying and selling of long-term assets. Financing activities include cash flows from debt and equity financing, like raising cash and paying debts.

Arrange the information gathered in steps 1 and 2 into the format required for the statement of cash flows. The net change in cash is equal to the sum of the cash flows from operating, investing, and financing activities.

Subsequent tutorials will go into further detail about these procedures.

summary

In this lesson, we discussed the uses of the statement of cash flows, the structure of the statement of cash flows, and the steps that are used in preparing the statement of cash flows. The statement of cash flows evaluates events that create a change in the amount of cash that is available to a company. The primary purpose of the statement of cash flows is to report the inflows and outflows of cash during a specific accounting period. That statement of cash flows provides a summary of the effects on cash from operating, investing, and financing activities.

Operating activities include the inflows and outflows of transactions and other events that enter into the determination of net income. Some operating activities might include cash receipts from sales of goods or services, dividends received from investments in equity securities, cash paid to vendors for supplies, or cash payments for interest and taxes. The operating activities section of the statement of cash flows can be prepared using the direct method that adjusts each item in the income statement to a cash basis or the indirect method that makes these same adjustments but to net income rather than to each item on the income statement.

The next section of the statement of cash flows outlines the investing activities which include transactions that involve the acquisition or disposal of noncurrent assets. Some possible activities might include the sale or purchase of property, plant, and equipment, collecting or making long-term notes to others, and selling or purchasing available-for-sale and held-to-maturity securities.

Finally, we discussed the financing activities that are included in the statement of cash flows. Financing activities include the inflows and outflows of transactions that involve creditors and owners such as chase received from issuing capital stock and bonds, mortgages, and notes, repayments of amounts borrowed, and payments of cash dividends.

Short-term investments that can easily and quickly be converted into cash, such as treasury bills and money market accounts.

Direct Method

An accounting method used to prepare the statement of cash flows that deducts only the operating expenses that are paid in cash from cash sales.

Financing Activities

Business activities that include transactions with creditors and owners.

Indirect Method

An accounting method used to prepare the statement of cash flows by adding or subtracting the differences between noncash activities from the net income.

Investing Activities

Business activities that include transactions involving the acquisition or disposal of noncurrent assets.

Operating Activities

Business activities that include the cash effect of transactions and other events that enter into the determination of net income.

Statement of Cash Flows

A required financial statement that shows the amount of cash that flows in and out of a company.

Working Capital

The amount of current assets minus current liabilities that is used in daily operations.