1. What is Income?

“It is better to have a permanent income than to be fascinating.”— Oscar Wilde

Generally speaking, income is financial gain derived from labor (work), capital (money), or a combination of the two. The financial gain derived from labor is generally referred to as wages or salary. Unless specifically exempt or excluded by law, all income is subject to income tax and is reported on a tax return.

2. Gross Income

Gross income means all worldwide income from whatever source derived unless specifically excluded from taxation by law. Gross income includes income realized in any form, whether in money, property, or services.

Gross income can be broken into two categories:

-

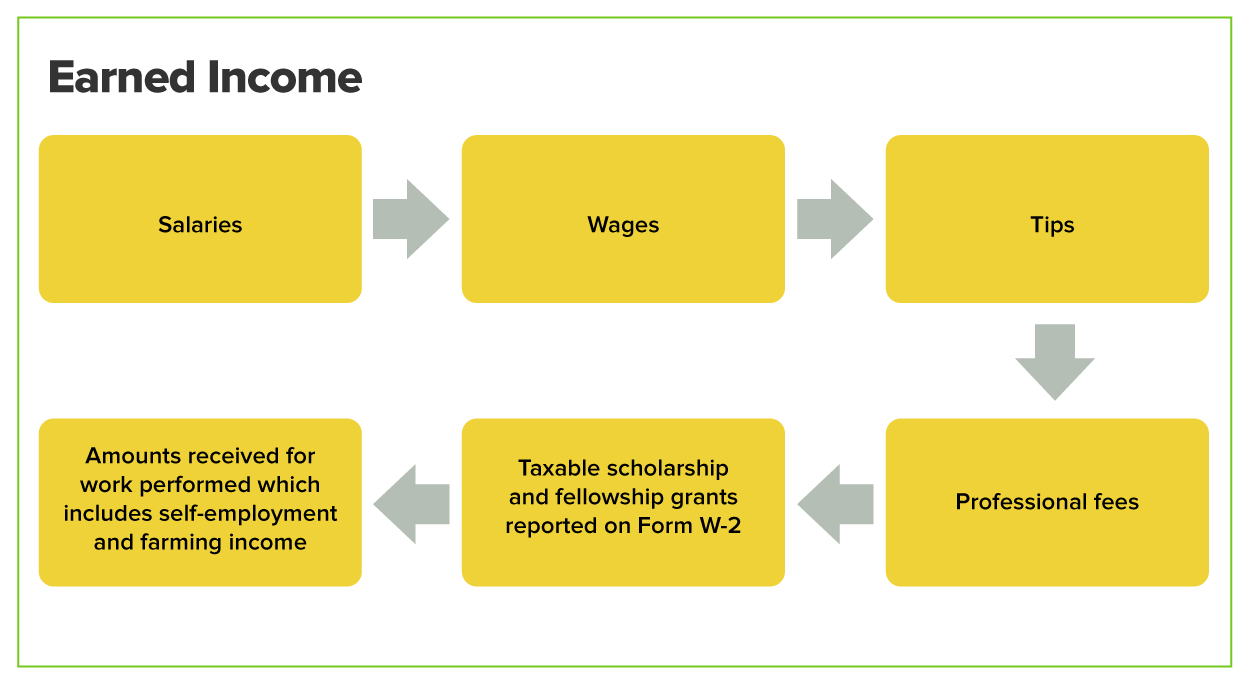

Earned income is received for services performed. Some examples are wages, salaries, commissions, tips, and generally farming and other business income.

IN CONTEXT: Disability Retirement Benefits

Disability retirement benefits qualify as earned income until the taxpayer reaches minimum retirement age. Minimum retirement age is the earliest age the taxpayer could have received a pension from their employer or an annuity if they did not have the disability. Social security disability payments, Social Security Disability Insurance (SSDI) payments, and military disability pension payments are not considered earned income.

-

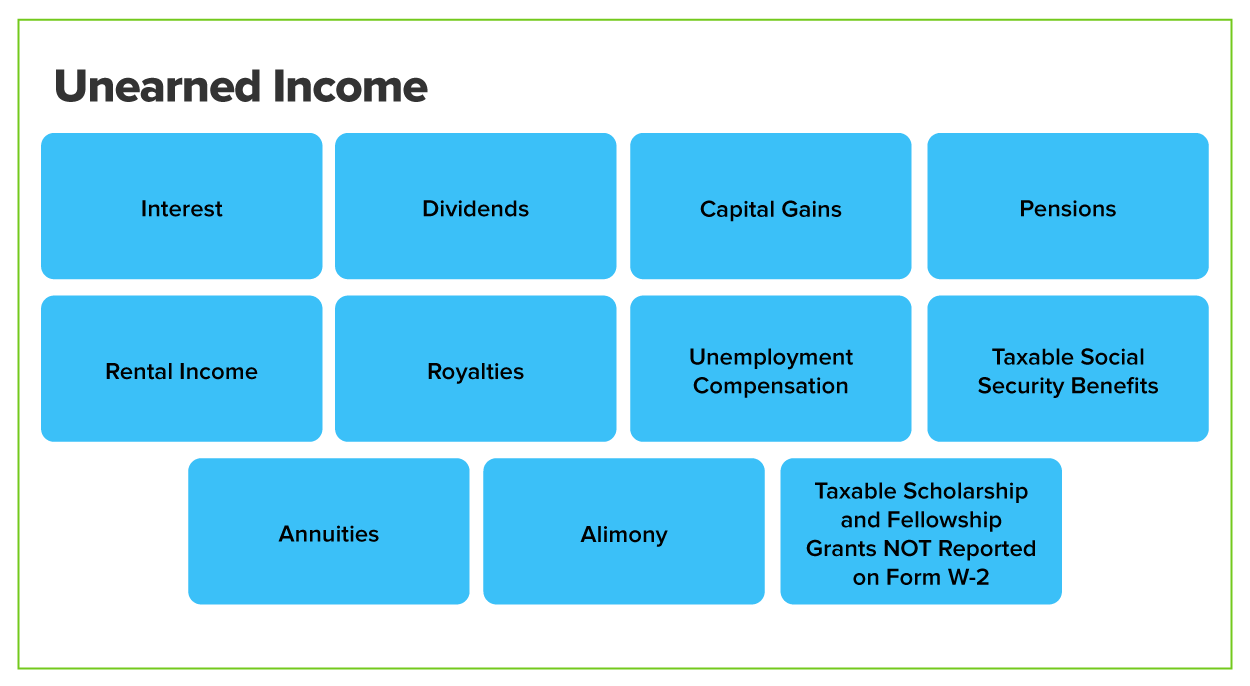

Unearned income is taxable income that does not meet the definition of earned income. It includes money received for the investment of money or other property, such as interest, dividends, capital gains, rents, and royalties. (This is often referred to as “investment income.”)

It also includes pensions, alimony, unemployment compensation, social security benefits, and other income that is not from performing services.

IN CONTEXT: Social Security Benefits

Social security benefits may be included in taxable income. Benefits are included in the taxable income (to the extent they are taxable) of the person who has the legal right to receive the benefits. You will learn more about social security benefits when you learn about retirement distributions.

-

EXAMPLE

Mary Moore earned $95,000 as vice president of a local bank. Mary also earned $750 of interest from a certificate of deposit from the same bank where she worked. Her salary of $95,000 is earned income. Her interest of $750 is unearned income. Mary’s total gross income is $95,750.

-

- Earned Income

- Income from personal services as distinguished from income generated by property or other sources. Earned income includes all amounts received as wages, tips, bonuses, other employee compensation, and self-employment income, whether in the form of money, services, or property.

- Unearned Income

- Taxable income other than that received for services performed (earned income). Unearned income includes money received for the investment of money or other property, such as interest, dividends, and royalties. It also includes pensions, alimony, unemployment compensation, and other income that is not earned.

3. What is and is not Gross Income?

Remember, gross income is all worldwide income from whatever source derived, unless specifically excluded from taxation by law. We will cover what is excluded by law first. Then we will look at some of the most common types of income included in gross income.

3a. Items Excluded From Gross Income

The slideshow below provides a list of some items of income excluded from gross income.

-

Alimony and separate maintenance payments executed or modified after 2018.

As a result of the Tax Cuts and Jobs Act, for divorces initiated or modified after 2018, alimony will be neither taxable to the spouse receiving it, nor deductible by the spouse paying it, and it is not included in gross income.

-

(Certain) foster care payments are not included in gross income. A qualified foster care payment is one made pursuant to a foster care program of a State or political subdivision thereof and paid for the care of a qualified foster individual or is paid as a difficulty care payment.

-

Certain income from the discharge of indebtedness includes debt discharged by Title 11 bankruptcy, insolvency, qualified farm indebtedness, and qualified principal residence indebtedness. Additionally, certain student loans that are canceled under the Public Service Loan Forgiveness Program are included. This was expanded by the Tax Cuts and Jobs Act (2017) and adds a new provision that student loan debt forgiveness due to death or permanent and total disability is excludable from income. Form 982, Reduction of Tax Attributes Due to Discharge or Indebtedness (and Section 1082 Basis Adjustment), is used to compute the amount of discharged indebtedness included, or excluded, from gross income.

-

Child Support. Amounts received as child support are not included as gross income.

-

Damages (other than punitive damages) received for personal injuries and physical sickness. Emotional damage is not considered a physical injury unless damages were paid for emotional distress attributable to an excluded physical injury or physical sickness. A best practice is to have the taxpayer's attorney provide specific instructions on what the legal settlement agreement is based on.

-

Disaster relief payments. Income received from a qualified disaster relief payment is excluded from income. These include reimbursements that are reasonable and necessary for the following if they are the result of, or due to, a qualified disaster:

- Personal, family, living, or funeral expenses.

- Repair or rehabilitation of a home or repair or replacement of the home’s contents

-

Educational assistance programs. Employees who receive educational assistance from their employers from a qualified educational assistance program. There is a maximum exclusion amount of $5,250. Publication 970, Tax Benefits for Education, provides more information.

-

Employer-purchased medical insurance premiums and reimbursements. Employer-provided coverage under an accident or health plan such as contributions to Archer MSAs, long-term care benefits provided through flexible spending accounts, and contributions to Health Savings Accounts (HSAs).

“Reimbursements by an employer of amounts paid by an employee for medicines and drugs purchased by the employee without a physician's prescription are excludable from gross income under IRC §105(b). However, amounts paid by an employee for dietary supplements that are merely beneficial to the general health of the employee or the employee's spouse or dependents, are not reimbursable or excludable from gross income under § 105(b).”Rev. Rul. 2003-102

-

Federal income tax refund is the amount of tax overpaid and returned to a taxpayer as a refund is not included as gross income. It is a return of an overpayment of tax.

-

Fringe Benefits. Many fringe benefits and other employment-related payments are excluded from gross income. These may include the following:

-

Company car. An employer provided a vehicle exclusively for business purposes, not personal use or commuting. De minimis (meaning too trivial to be considered, especially with regard to legal matters) personal use may also be excluded from gross income. An example would be doing a quick personal errand en route to an appointment.

-

De minimis fringe benefits. The term “de minimis fringe” means any property or service the value of which is (after taking into account the frequency with which similar fringes are provided by the employer to the employer's employees) so small as to make accounting for it unreasonable or administratively impracticable.

-

Purchase discounts. To be excludable, the property or service must be offered to the public in the ordinary course of business. Certain limitations to the amount of the discount apply.

-

No-additional-cost-to-employer services, such as: free travel for airline employees; hotel rooms for hotel employees; and use of facilities by spa or hotel employees.

-

Transportation. This includes transportation in a commuter highway vehicle, transit pass, qualified parking, and any qualified bicycle commuting reimbursement, as long as they meet the necessary requirements.

-

Other: Occasional coffee, donuts, office party, etc.

-

Gifts occur when the value of the property transferred is greater than what is received in return for the transfer. If a mother gives their child $500 cash, it is not included in the recipient’s gross income. Interestingly, the person who gives the gift may have a tax obligation. Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return, is completed by the individual giving the gift if over the annual exclusion amount, which is $16,000 for 2022 and is indexed for inflation annually.

-

Group-term life insurance. Usually, it is the cost of up to $50,000 of group-term life insurance provided by the employer.

-

Inheritance. Property and funds inherited are not included in gross income, however, any income produced from the inherited property is included in gross income. For example, if you inherit $50,000 and place the funds in a savings account, the interest earned on the $50,000 is included in gross income.

-

Interest on state and local bonds. A state or local bond is an obligation of a State or a political subdivision thereof. This includes the District of Columbia and any possession of the United States.

-

Life insurance. Life insurance payments, if paid by reason of the death of the insured. Life insurance contracts purchased as a "reportable policy sale" are an exception and are included in gross income. A reportable policy sale is when someone purchases life insurance for someone who has no substantial family, business, or financial relationship with the insured. For example, a life insurance policy payout I receive from the death of my mother is not included in my gross income. However, if I purchased a life insurance policy that covered the life of John Doe, someone I am not related to or work with, the funds would be included in gross income.

-

Meals or lodging furnished for the convenience of the employer. The meals must be provided on the employer’s business premises. The lodging must be accepted by the employee on the business premises as a condition of their employment.

-

(Certain) Medicaid waiver payments are considered payments to an individual who provides care for eligible individuals who would otherwise require care in a hospital, nursing facility, or intermediate care facility.

More information on this can be found in the Schedule 1 (Form 1040) instructions for line 8s.

-

Qualified cafeteria plan benefits. Employee benefits included as qualified "Cafeteria Plan Benefits" include accident and health benefits, adoption assistance, dependent care assistance, group-term insurance, and health flex spending arrangements.

-

Qualified clergy housing allowances. Although typically exempt from income tax, the clergy housing allowance cannot be more than the reasonable pay for service. It is also generally subject to self-employment tax.

-

Qualified military benefits. A qualified military allowance or veterans' benefits paid to any member, or former member, of the uniformed services of the United States, or a dependent of one.

-

Qualified scholarships and fellowships. A qualified scholarship or fellowship is for an individual who is obtaining a degree at a qualified educational organization. It includes any amount received to the extent the amount was used for qualified tuition and related expenses.

-

Student Loan Debt Cancellation (2021 through 2025) The treatment of student loan forgiveness for discharges in 2021 through 2025 was modified by the American Rescue Plan Act of 2021. Normally, if the taxpayer is responsible for making payments on a loan, and the loan is canceled or paid on their behalf, the amount is included as gross income for tax purposes. However, for Tax Years 2021 through 2025, if the loan was one of the following: postsecondary education expense, a private education loan, a loan from select educational organizations, or a loan from a tax exempt organization, the taxpayer may be able to exclude the amount forgiven from gross income.

More information can be found in Publication 4681, Canceled Debts, Foreclosures, Repossessions, and Abandonments (for individuals) or Publication 970, Tax Benefits for Education.

-

Welfare payments are exempt from tax, and not included in gross income.

-

Workers’ compensation paid under a workers’ compensation act. The amount of workers’ compensation paid for occupational sickness or injury is fully exempt from tax. This would also apply to this type of compensation paid to a taxpayer’s survivors.

IN CONTEXT: Cobra Premium Assistance

Sometimes tax laws are created for a very specific place in time and is not meant for all years going forward. An example is Consolidated Omnibus Budget Reconciliation Act (COBRA) premium assistance. For a six-month period of April 1 through September 30, 2021, individuals who elected COBRA coverage may have been eligible for 100% premium assistance. The premium assistance granted for that time period was not included in the individual’s gross income.

3b. Most Common Items Included in Gross Income

The table below provides a list of some items of income included in gross income.

|

Included in Gross Income

|

|---|

|

Alimony and separate maintenance payments executed before 2019

|

|

Annuities

|

|

Compensation for services, including fees, commissions, and certain fringe benefits

|

|

Distributive share of partnership gross income

|

|

Dividends

|

|

Gains derived from the sale or exchange of property

|

|

Gross income derived from business

|

|

Income from an interest in an estate or trust

|

|

Income from life insurance and endowment contracts

|

Income from the discharge of indebtedness

(For example, a credit card company writes off the taxpayer’s debt. The amount the taxpayer now does not owe to the credit card company is included as gross income, unless the discharge meets certain requirements.)

|

|

Income in respect of a decedent

|

|

Interest

|

|

Jury Duty Income

|

|

Pensions

|

|

Qualified sick leave wages and qualified family leave wages

|

|

Rents

|

|

Royalties

|

|

Self-employment (business income)

|

|

Social security and tier 1 railroad retirement benefits

|

|

Unemployment income

|

|

Wages and tips

|

-

- Alimony Payments

- Payments made by one spouse to the other spouse or former spouse under a written separation or divorce instrument. Qualified alimony and separate maintenance payments are included in the gross income of the recipient and are deductible by the payer if the orders were executed before January 1, 2019. Child support payments, voluntary payments, and property settlements are not treated as alimony.

- Annuity

- A fixed sum payable to a person at specific intervals for a specific period of time or for life. Payments represent a partial return of capital and a return on the capital investment. Once the cost in the investment has been recovered, all payments are then included in gross income.

- Dividend

- A stockholder’s share of the profits of a corporation. Dividends may be classified as either ordinary or qualified. Ordinary dividends are taxable as ordinary income, while qualified dividends must meet certain requirements and are taxed at lower capital gain rates. For tax purposes, an insurance dividend is not a true dividend, but a return of premium, and dividends from a savings and loan association or credit union are interest, not dividends.

- Decedent

- A person who has died.

- Interest Received

- An amount received for the use of money that is to be repaid in full at a specified time or on demand.

- Pension

- Defined periodic payments made over a specified period (usually life) from an employer-maintained plan to workers who have met the stated requirements. The primary purpose of a pension is to provide retirement income.

- Gross Rents

- Total income from rents before expenses or the depreciation or cost recovery deduction.

- Royalty

- A payment received for the right to exploit a taxpayer’s ownership of natural resources or a taxpayer’s literary, musical, or artistic creation.