In this lesson, you will learn what a mortgage is, how it works, and the different types of mortgages available. Specifically, this lesson will cover the following:

1. What Is a Mortgage?

-

Think of a mortgage as a partnership between you and a lender, like a bank or credit union. You need money to buy a house, and the lender has the funds to help you. In exchange, you agree to repay the loan over time with interest, essentially “renting” the money you borrow.

-

EXAMPLE

Imagine your dream home costs $300,000. You’ve saved up $60,000 for a down payment, but that leaves $240,000 you need to finance. A mortgage covers that $240,000, and you agree to repay it over 15, 20, or 30 years in monthly installments.

A mortgage is unique because the loan is directly tied to the property. If you can’t make payments, the lender has the right to take ownership of the house through foreclosure. This makes a mortgage a secured loan, with the home as collateral. While that might sound scary, it’s simply a way for lenders to manage their risk while helping you achieve homeownership. Let’s look at how a mortgage works.

1a. How Does a Mortgage Work?

At its core, a mortgage is a long-term payment plan that allows you to buy now and pay later. Each monthly payment is divided into four key parts:

- Principal: The original amount you borrowed (e.g., $240,000) is your principal.

- Interest: This is the cost of borrowing money, calculated as a percentage of the loan.

- Taxes: Many lenders collect property taxes as part of your monthly payment and pay them on your behalf.

- Insurance: This includes homeowner’s insurance and, in some cases, private mortgage insurance (PMI), which protects the lender if you default on the loan.

When you first start paying your mortgage, most of your payment goes toward interest. For example, if your monthly payment is $1,500, only $300 might go toward the principal in the early years, while the remaining $1,200 covers interest. Over time, this balance shifts, and more of your payment reduces the principal.

-

EXAMPLE

Let’s say you have a 30-year mortgage with a 5% fixed interest rate. In the first year, you might pay $12,000 in interest but only reduce your loan balance by $3,000. By Year 15, those numbers flip—you’re paying more toward principal and less toward interest.

There’s a lot of terminology when it comes to understanding the inner workings of a mortgage. These terms are important to understand so you can make a wise decision when buying a house. Don’t worry; let’s break them all down.

Mortgage Terms to Know

Understanding mortgage jargon is essential to feeling confident about your home buying decision. You’ve already learned about a few of these concepts in previous lessons, but let’s demystify the most common terms you’ll encounter:

- Down Payment: This is the cash you pay up-front. A 20% down payment is typical, but some loans allow as little as 3%–5%. For example, on a $300,000 home, a 20% down payment is $60,000, while 5% is just $15,000.

- Interest Rate: This is the percentage the lender charges for borrowing money. Fixed rates stay the same over the life of the loan, while adjustable rates can increase or decrease based on market conditions.

- Loan Term: The length of time you agree to repay the loan is your loan term. A 30-year term offers smaller monthly payments, but a 15-year term reduces the total interest paid.

- Amortization: This is the gradual repayment of your loan through monthly payments. Your lender will provide an amortization schedule showing exactly how your payments will break down over time.

- Escrow: This is the account where your lender holds funds for property taxes and insurance. Escrow is like a savings account that ensures these costs are paid on time.

- Closing Costs: These include fees for processing the loan, such as appraisal fees, title insurance, and attorney fees. These usually total 2%–5% of the home’s purchase price.

Now that you understand how a mortgage works and some of the important terminology, let’s examine the types of mortgages available to you so you can make a smart financial decision when buying a house.

-

- Private Mortgage Insurance (PMI)

- Insurance you pay if your down payment is less than 20%, protecting the lender if you default.

- Amortization

- The process of paying off a loan through regular payments of principal and interest over time.

- Escrow

- A special account where funds for property taxes and insurance are held by your lender.

2. Types of Mortgages

You know how a mortgage works, but the big question is what type of mortgage you should get. Mortgages aren’t one-size-fits-all. The type of mortgage you choose depends on your financial situation, long-term goals, and comfort with risk. Let’s explore six (6) of the most common types of mortgages, who they’re best suited for, and important details to consider.

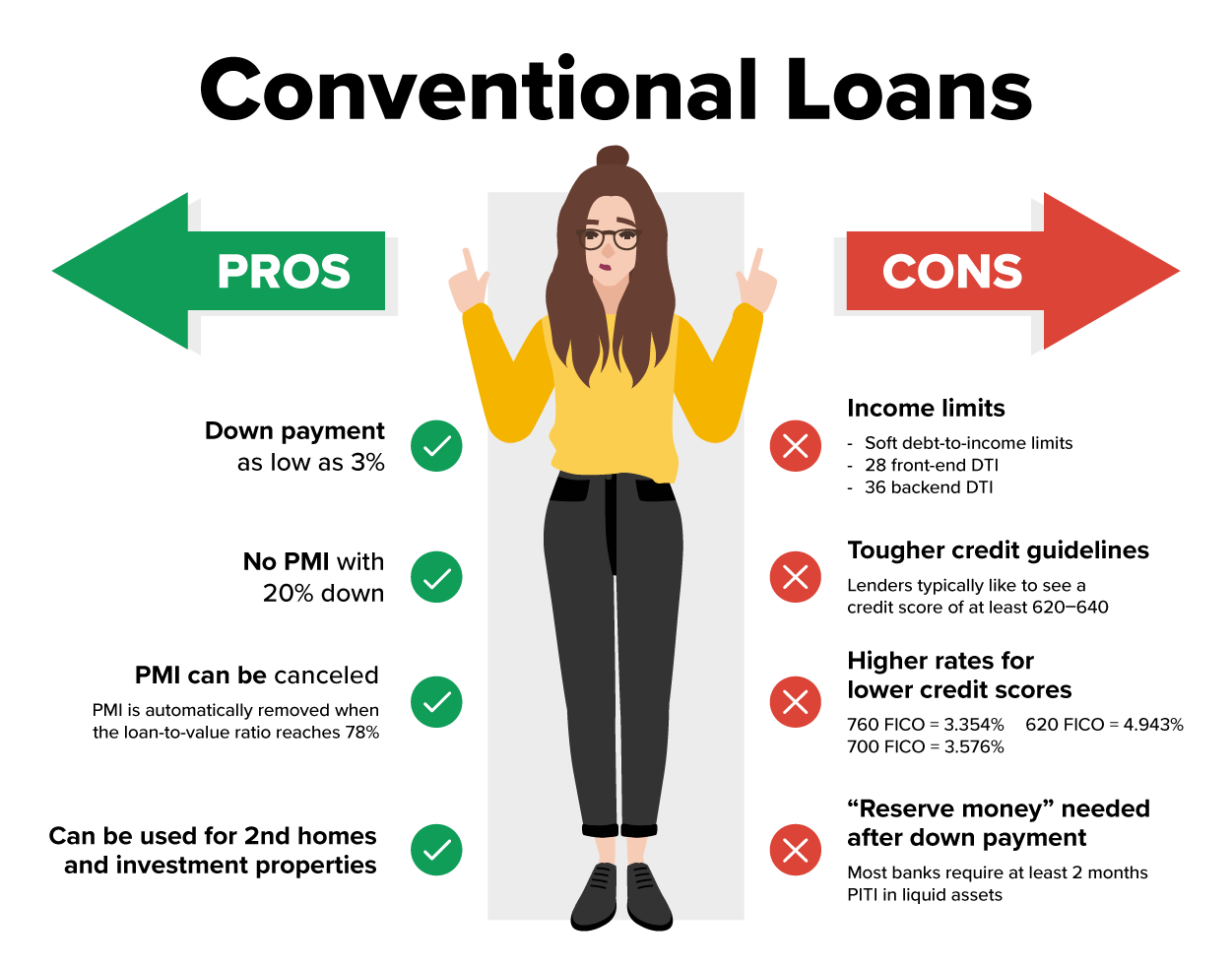

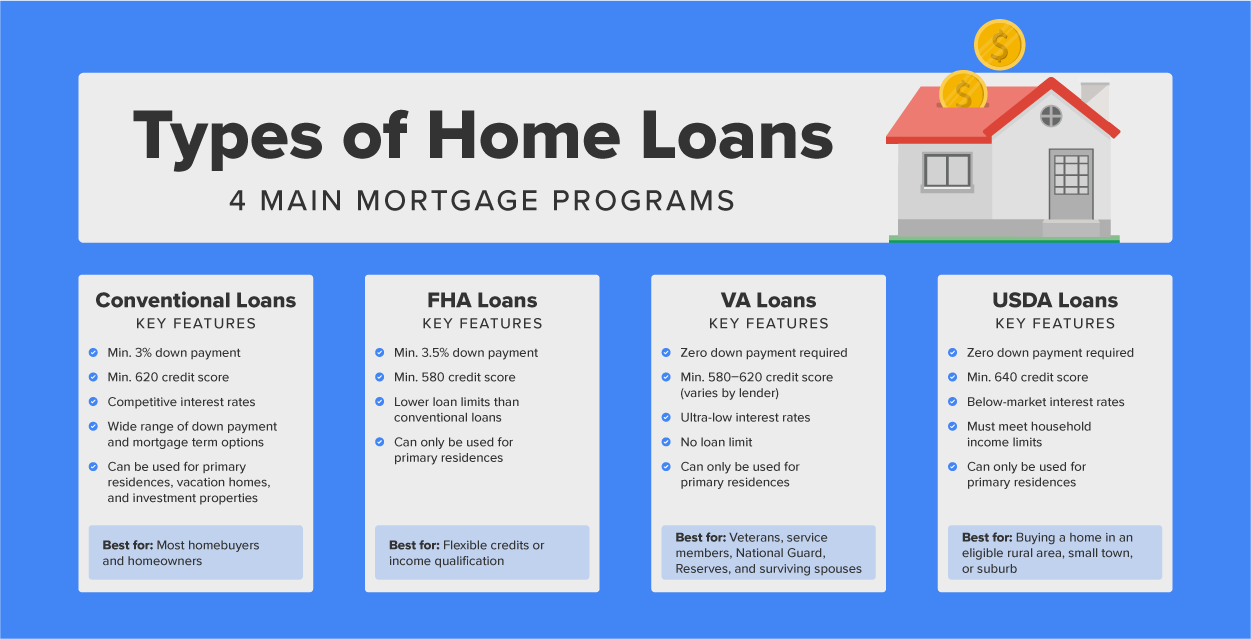

1. Conventional Loan

A conventional loan is the go-to option for many buyers. It’s not insured or guaranteed by the government, which means lenders typically have stricter requirements. You’ll need the following:

- A good credit score (usually 620 or higher)

- A down payment of at least 5%–20% of the home’s price (if your down payment is less than 20%, you may need to pay for PMI)

A conventional loan is best for buyers with solid credit and a substantial down payment. Here are a few advantages of getting a conventional loan:

- Conventional loans often offer competitive interest rates, but they vary depending on your credit score and the size of your down payment.

- Once you reach 20% equity in your home, you can request to cancel PMI, reducing your monthly payments.

2. FHA Loan

An FHA loan, backed by the Federal Housing Administration, is designed to help buyers who might not qualify for a conventional loan. Here are a few details of FHA loans:

- They have lower credit score requirements (as low as 500 with a 10% down payment or 580 with 3.5% down).

- They have smaller down payment options, making homeownership more accessible.

- They require a mortgage insurance premium (MIP), which can’t be canceled like PMI on conventional loans. This adds to your long-term costs.

- While they’re great for affordability, the up-front and annual insurance fees can make FHA loans more expensive over time compared to conventional loans.

An FHA loan is best for first-time homebuyers or buyers with lower credit scores or limited savings.

3. VA Loan

A VA loan is a fantastic option for veterans, active-duty service members, and some military spouses. These loans are guaranteed by the Department of Veterans Affairs. Here are a few details of VA loans:

- There is no down payment requirement.

- There is no PMI or MIP.

- They offer competitive interest rates.

- You’ll need to meet specific service requirements to qualify.

- They often have a one-time funding fee (which can be rolled into the loan), but it’s usually much lower than ongoing mortgage insurance costs on other loans.

- They are best suited for eligible veterans and military families.

4. Fixed-Rate Mortgage

A fixed-rate mortgage locks in your interest rate for the life of the loan. This means your monthly principal and interest payments remain consistent, even if market rates change. Common terms are 15, 20, and 30 years.

A fixed-rate mortgage is best suited for buyers who plan to stay in their home long term and value payment stability, which is a very good thing. Here are a few things to know:

- While a 30-year term offers lower monthly payments, you’ll pay more interest over time.

- A 15-year term reduces your total interest but comes with higher monthly payments. It’s a great choice if you can afford it and want to pay off your home faster.

5. Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage (ARM) starts with a lower introductory interest rate (e.g., 4% for the first 5 years in a 5/1 ARM) that adjusts periodically based on market conditions.

An ARM is best for buyers who plan to sell or refinance within a few years or expect interest rates to stay low. Here are some important things to know about ARMs:

- After the initial fixed period (e.g., 5 years), your rate can increase, which means your monthly payment might rise. This is why you need to really understand the terms of your loan before you agree to an ARM loan.

- ARMs carry more risk, so they’re better suited for financially stable buyers who are prepared for potential payment increases.

-

In 2008/2009, ARMs were one of the biggest culprits behind the housing market crash. Back then, ARMs were a hit because they started with super low payments—perfect if money was tight. But the catch? Those rates weren’t locked in. After a few years, they shot up, and suddenly people had monthly payments they just couldn’t afford.

On top of that, lenders were giving out mortgages to almost anyone, even if they didn’t have steady income or solid credit. It was like a ticking time bomb. When payments skyrocketed, people started losing their homes, the housing market tanked, and it took the whole economy down with it. What seemed like a great deal at first ended up being a total disaster.

6. USDA Loan

A USDA loan, backed by the U.S. Department of Agriculture, is aimed at buyers in rural or suburban areas. These loans often include the following:

- No down payment requirement

- Low interest rates and mortgage insurance costs

A USDA loan is best suited for buyers with moderate income looking to purchase a home in eligible rural areas. USDA loans are a great option, but they come with a few rules:

- These loans are for people with low to moderate incomes, so your household income needs to be below a certain level based on where you live and how many people are in your family. Think of it as making sure the loans go to those who really need them.

- The home you’re buying has to be in a rural or suburban area the USDA approves, and it must be your main home (not a vacation spot or rental). Plus, it has to meet safety and livability standards.

-

For most buyers, a

fixed-rate conventional loan is the best choice. It offers stability, competitive rates, and flexibility if you can afford at least a 5% down payment and have a decent credit score. If you don’t meet those criteria, an FHA loan is often the next best option because it opens the door to homeownership for those with less-than-perfect credit or smaller savings.

You’re now a pro at the different types of mortgages that are available, so let’s learn about how to actually qualify for a mortgage. You’ve already learned most of what we’ll cover in previous lessons, but it’s important to apply these concepts to qualifying for a mortgage.

-

- Conventional Loan

- A home loan not backed by the government.

- FHA Loan

- A government-backed loan with a lower down payment and easier credit requirements.

- Mortgage Insurance Premium (MIP)

- Fees borrowers pay to protect lenders in case they default on their mortgage.

- VA Loan

- A no-down-payment loan for eligible military members, backed by the Department of Veterans Affairs.

- Fixed-Rate Mortgage

- A loan with a stable interest rate and monthly payment over the entire term.

- Adjustable-Rate Mortgage (ARM)

- A loan with an interest rate that can change over time, starting low and adjusting later.

- USDA Loan

- A loan for low- to moderate-income buyers in rural areas.

- Fixed-Rate Conventional Loan

- A home loan with a stable interest rate and consistent monthly payments, not backed by the government.

2a. How to Qualify for a Mortgage

Now that you’ve learned what a mortgage is and explored the different types of mortgages, qualifying for one might still feel a bit intimidating. But, really, it’s just about showing lenders that you’re financially reliable. They want to make sure you can handle the monthly payments and won’t default on the loan. By understanding what lenders look for—like your income, credit score, and debt—and preparing in advance, you can make the process much smoother and improve your chances of getting approved.

Step 1: Build and Maintain a Good Credit Score

You already know how important your credit score is from a previous lesson, but let’s refresh your memory. Your credit score is one of the first things lenders check. Scores range from 300 to 850, and higher scores mean better loan terms and lower interest rates.

What’s a Good Score?

- 620 or higher: Typically required for conventional loans

- 580 or higher: For FHA loans (with a 3.5% down payment)

- 740 or higher: Often qualifies for the best interest rates

-

If your credit score is low, start improving it before applying for a mortgage. Here are three things you can work on:

- Pay down credit card balances to below 30% of your credit limit. Remember, this is called your credit utilization rate.

- Avoid opening new lines of credit or taking on new debt.

- Check your credit report for errors and dispute any inaccuracies. There are lots of resources we gave you for easily checking your credit report in previous lessons.

Step 2: Manage Your Debt-to-Income Ratio

Lenders want to ensure your monthly income can comfortably cover your mortgage payments alongside other debts. This is measured by your debt-to-income (DTI) ratio—the percentage of your monthly income that goes toward paying debt.

How It’s Calculated:

Divide your total monthly debt payments by your gross (pretax) monthly income.

- If you pay $1,200 for a car loan, credit cards, and other debts, and you earn $5,000 a month, your DTI will be 24%.

What Lenders Prefer:

- A DTI of 43% or lower is typically required.

- Lower DTIs (under 36%) make you a more attractive borrower and may qualify you for better terms.

Here are two ways you can improve your DTI before you apply for a mortgage:

- Pay off small debts to lower your DTI.

- Avoid taking on new debt, such as financing a car, right before applying.

Step 3: Show Stable Income and Employment History

Lenders need to see that you have a steady and reliable income. Most will require these:

- Two years of consistent employment history in the same field or industry

- Pay stubs showing your current income (If you recently switched jobs, provide documentation showing your income is consistent or higher than before. Stable, predictable income reassures lenders.)

- Tax returns (especially if you’re self-employed)

You may also be self-employed or run your own business. While this is great for your financial future, it can complicate the mortgage process. You’ll need the following:

- Two years of personal and business tax returns

- Profit and loss statements or other documentation to verify your income

Step 4: Save for a Down Payment

Your down payment plays a big role in qualifying for a mortgage. It directly affects:

- The amount you need to borrow.

- Whether you’ll need PMI (remember, this is required if your down payment is less than 20% for a conventional loan)

What’s the Minimum Down Payment?

- Conventional Loans: As low as 3%–5% (but PMI applies if under 20%)

- FHA Loans: 3.5% if your credit score is 580 or higher; 10% for scores under 580

- VA and USDA Loans: Often require no down payment

Start saving early! Even small monthly contributions to a dedicated savings account can add up over time.

Step 5: Have Enough Cash Reserves

Lenders like to see that you’ll have money left after closing to handle emergencies or unexpected expenses, known as cash reserves. Cash reserves include these:

- Money in savings or checking accounts

- Retirement funds (like 401(k)s or IRAs), though tapping these for mortgage payments is discouraged

- At least 2 to 3 months’ worth of mortgage payments in reserve

-

Avoid draining your savings for a larger down payment if it means you won’t have an emergency fund. You’ll want to make sure you have some savings left after you purchase your home for any unexpected expenses.

Step 6: Be Prepared for Closing Costs

In addition to your down payment, you’ll need to cover closing costs, which you learned typically range from 2% to 5% of the home’s purchase price. These include the following:

- Appraisal fees

- Title insurance

- Loan origination fees

- Property taxes (prepaid for the first few months)

Ask your lender for a breakdown of the estimated closing costs early in the process. Some sellers may also agree to cover part of these costs during negotiations.

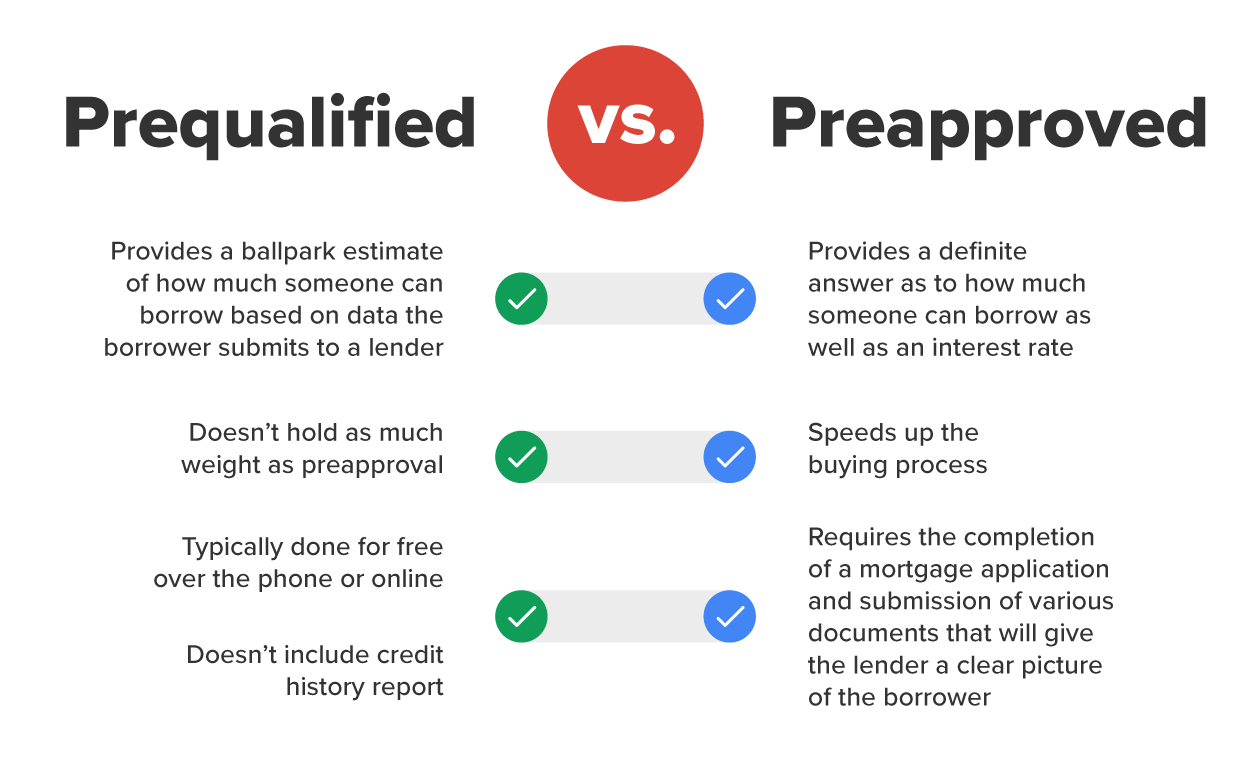

Step 7: Get Preapproved

Before you start house hunting, getting preapproved for a mortgage is a smart move. If you remember from a previous lesson, preapproval is like getting a green light from a lender—they review your finances and let you know how much they’re willing to lend you. It shows sellers you’re serious and helps you focus on homes within your budget. Preapproval gives you:

- A clear idea of how much you can afford, so that you don’t go look at houses that are more expensive than you can afford

- A stronger negotiating position with sellers, who will see you as well prepared to buy their house when you are preapproved

What You’ll Need for Preapproval:

- Proof of income (pay stubs and tax returns)

- Proof of assets (bank statements and investment accounts)

- Proof of identity (government-issued ID)

- Credit check authorization

Don’t confuse preapproval with prequalification.

Prequalification is a quick estimate of what you might qualify for, while preapproval involves a more thorough review of your finances and carries more weight with sellers.

Step 8: Avoid Big Financial Changes

Between getting preapproved and closing on your home, avoid making any major financial moves that could impact your credit or savings, like these:

- Opening new credit accounts since this is one of the factors that can impact your credit score

- Making large purchases, like a car or furniture

- Changing jobs or becoming self-employed

Keep your finances stable during this period. Lenders often recheck your credit and financial situation right before closing, so make sure you don’t purchase anything until your home purchase is finalized.

Qualifying for a mortgage boils down to showing lenders that you’re financially prepared and trustworthy. Focus on building good credit, saving for a down payment and closing costs, and maintaining a stable income. By tackling these steps early, you’ll make the process smoother and increase your chances of securing the keys to your dream home.

-

- Cash Reserves

- Savings set aside to cover mortgage payments or emergencies after buying a home.

- Prequalification

- An estimate of how much you might borrow, based on basic financial information you provide.

In this lesson, you got a good understanding of what a mortgage is and how a mortgage works when purchasing a home. You also learned about all the different types of mortgages and how to qualify for a mortgage when you’re ready to purchase.