In this lesson, you will learn about why you need health insurance and all of the associated terms you need to know. Specifically, this lesson will cover the following:

1. Why You Need Health Insurance

-

Imagine this: You wake up one morning with a sharp pain in your stomach. At first, you brush it off, thinking it’s just something you ate. But as the hours pass, the pain worsens until you’re doubled over, unable to ignore it any longer. You head to the emergency room, where doctors quickly diagnose you with appendicitis. You need surgery—now.

The good news? The procedure is a success. The bad news? The hospital bill arrives, and it’s a staggering $20,000.

If you have health insurance, your cost might only be a few hundred dollars, depending on your plan. But if you don’t, you’re on the hook for the full amount. Suddenly, a routine medical emergency can turn into a financial nightmare.

Health insurance isn’t just about avoiding massive hospital bills—it’s about peace of mind. It ensures that you can see a doctor when you need to, get prescriptions at an affordable rate, and access preventive care to stay healthy. Think of it like a seat belt: You hope you never need it, but when you do, it can save you from disaster.

-

Preventive (also known as preventative) care is all about staying ahead of health issues before they become serious. It includes routine checkups, screenings, vaccinations, and healthy lifestyle choices to catch problems early and keep you feeling your best. Think of it as maintenance for your body—just like you’d service a car to prevent breakdowns.

But let’s be real—health insurance can be confusing. Between premiums, deductibles, and coinsurance, it can feel like you need a degree just to understand it. That’s why we’re breaking it all down into plain English so you can make smart choices about your health and your wallet.

2. Health Insurance Terms

Health insurance can feel like learning a new language. The terms are confusing, the documents are long, and making sense of it all can be overwhelming. Let’s break it down into real-life comparisons to help make sense of it.

1. Premium: Your Monthly Membership Fee

You’ve already learned about what premium means, but let’s do a review. Think of your premium like a gym membership. Even if you don’t go to the gym every day, you still pay your membership fee to keep your access. Your health insurance premium works the same way—you pay a set amount every month to keep your coverage active, regardless of whether you use it.

The trade-off? If you ever do need medical care, you’ll be glad you kept it up.

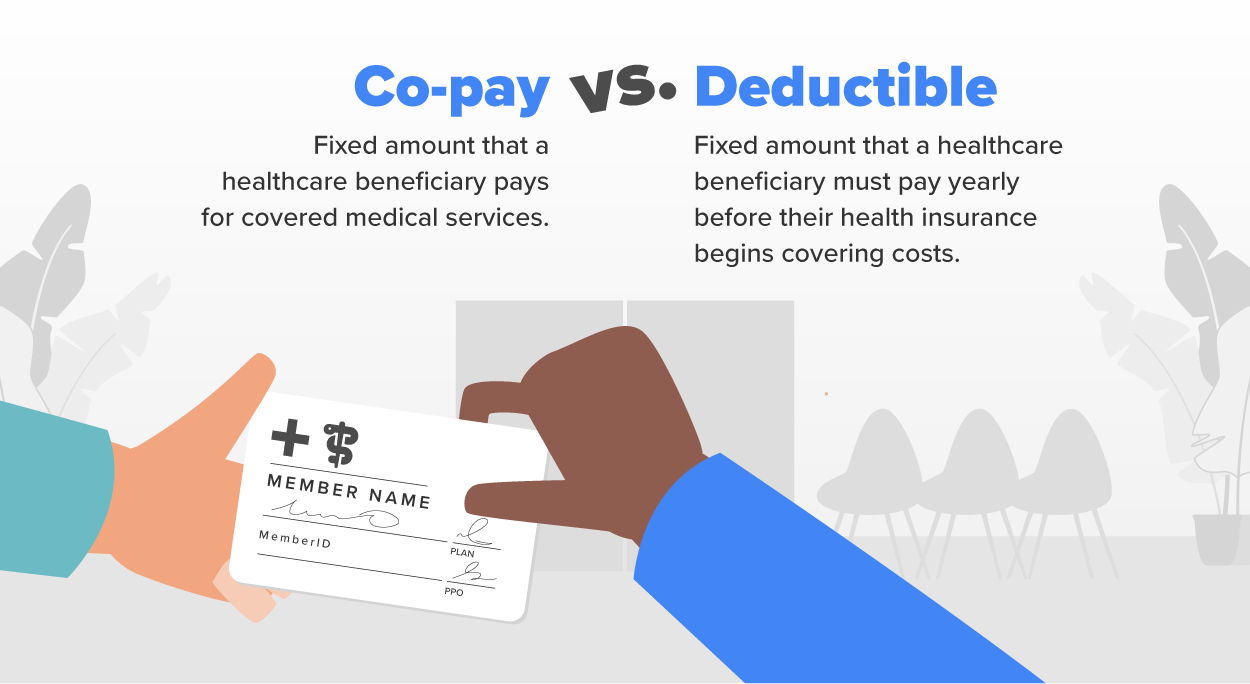

2. Deductible: The Amount You Pay Before Insurance Kicks In

Imagine you have a medical piggy bank labeled “expenses.” Before your insurance starts helping, you have to cover a certain amount yourself—that’s your deductible.

- If your deductible is $1,500, you must pay $1,500 in medical costs before your insurance starts covering a portion of the bills.

- Plans with low deductibles often have higher premiums (monthly payments).

- Plans with high deductibles have lower premiums, but you’ll pay more out of pocket when you need care.

It’s all about balance—do you want to pay more each month and less when you get care, or less each month and more when you get care?

3. Co-Pay: Your Ticket Fee for Health Care

A co-pay is like paying a cover charge at a concert.

- Your ticket (co-pay) might be $30 to see a doctor, even though the full cost of the visit is $150.

- Your insurance covers the rest, but this small fee keeps your costs predictable.

Different services have different co-pays—for example, visiting a specialist might cost more than seeing your primary doctor.

4. Coinsurance: Splitting the Bill With Your Insurance

Imagine you and a friend go out to dinner. Your friend covers 80% of the bill, and you pay the remaining 20%.

That’s coinsurance in action.

- If your coinsurance is 80/20, your insurance covers 80% of your medical costs after you meet your deductible.

- You’re responsible for the other 20%.

If your hospital bill is $10,000, you’d pay $2,000, and your insurance would cover $8,000 (assuming you’ve met your deductible).

5. Out-of-Pocket Maximum: Your Financial Safety Net

Now, let’s talk about worst-case scenarios. Say you need major surgery, and the bills keep piling up.

Thankfully, health insurance has a safety net called the out-of-pocket maximum.

- This is the most you’ll have to pay for covered medical expenses in a year.

- Once you hit this limit (including deductibles, co-pays, and coinsurance), your insurance covers 100% of the remaining costs.

If your out-of-pocket maximum is $5,000, that’s the absolute most you’ll pay for the year—even if your total medical bills hit $100,000.

6. Network (In-Network Versus Out-of-Network): Where You Can Get Care

Your insurance network is like a special discount club.

- Doctors and hospitals in your network have agreed to charge lower rates for members.

- Going out-of-network can mean much higher costs or zero coverage, depending on your plan.

If you go to a doctor outside your network, you might still get what you need, but you’ll pay a lot more.

7. Explanation of Benefits (EOB): Your Insurance Receipt

A few weeks after seeing a doctor, you get a letter from your insurance company. It looks like a bill, but it says “THIS IS NOT A BILL” at the top.

That’s your explanation of benefits (EOB)—your insurance’s way of breaking down the following:

- What the doctor charged

- What your insurance paid

- What you still owe

Checking your EOBs ensures that you’re not being overcharged for medical services.

-

EXAMPLE

An EOB is NOT a bill—it’s a summary of what your health insurance covered and what you might owe.

Imagine you went to the doctor for a checkup and got a test done. Here’s what your EOB might look like:

|

Service

|

Doctor’s Price

|

Discount (Insurance Rate)

|

Amount Insurance Paid

|

What You Owe

|

|

Checkup Visit

|

$200

|

|

$100

|

$20 (Co-pay)

|

|

Lab Test

|

$150

|

|

$75

|

$25 (Coinsurance)

|

Total Doctor’s Price: $350 ($200 for checkup + $150 for lab testing)

Total Discounted Price: $220 ($350 − $80 − $50)

Total Insurance Paid: $175 ($100 + $75)

Total You Owe: $45 ($20 co-pay + $25 coinsurance)

Key Takeaways:

- The doctor’s price is often higher, but insurance negotiates a discount.

- Insurance pays part of the cost, based on your plan.

- You only pay your co-pay or coinsurance (depending on your plan).

- If you’ve hit your out-of-pocket maximum, you won’t owe any additional amounts for covered services!

Remember: Always check your EOB before paying a medical bill to ensure that it matches what you actually owe.

8. Understanding the Different Types of Health Plans

Choosing a health plan can feel like picking a streaming service—each one has different rules, benefits, and restrictions. We’ll cover them all in depth in an upcoming lesson to help you decide which plan is best for you. For now, here is an overview of some of the features of each:

-

Health Maintenance Organization (HMO)

- Must choose a primary doctor

- Need referrals to see specialists

- Lower costs, but less flexibility

- Think of it like this: “You need permission before switching shows on Netflix.”

-

Preferred Provider Organization (PPO)

- No referrals needed

- Can see out-of-network doctors (for a higher cost)

- More expensive than HMO but more freedom

- Think of it like this: “You can watch any show, but in-network is cheaper.”

-

Exclusive Provider Organization (EPO)

- No referrals needed

- Must stay in-network

- Think of it like this: “You can switch shows freely, but only within one streaming platform.”

-

High-Deductible Health Plan (HDHP)

- Lower monthly premium

- Higher deductible ($1,500+ before coverage kicks in)

- Often paired with a health savings account (HSA)

- Think of it like this: “Pay less each month but more when you need care.”

-

Here is a quick video that covers these health plans using visuals:

-

EXAMPLE

Scenario 1: Routine Checkup

Doctor visit cost: $150

Insurance covers preventive care → You pay $0

Scenario 2: Emergency Room Visit

Bill: $4,500

You pay $1,000 deductible

Coinsurance (80/20) applies to the remaining $3,500

You pay $700 (20%); insurance covers the rest

Total cost for you: $1,700

Scenario 3: Catastrophic Event (Major Surgery—$50,000 Bill)

Your out-of-pocket maximum is $5,000

You pay $5,000 total; insurance covers the rest

Health insurance may seem complicated, but understanding these basics can help you choose the right plan, avoid surprise bills, and make informed financial decisions.

When used wisely, health insurance isn’t just a bill you pay—it’s a financial tool that protects you from medical debt while ensuring that you get the care you need.

-

Now, it’s your turn! Use what you’ve learned to resolve these real-life health insurance scenarios. Check your answers using the “+” button to see how well you understand how health insurance works.

Scenario 1: Prescription Pickup

You go to the pharmacy to pick up a prescription. The total cost is $120, but your insurance plan includes the following:

- A $25 prescription co-pay

- No deductible for prescriptions

Scenario 2: Specialist Visit

You visit a dermatologist for a skin issue. The total cost of the visit is $300, and your insurance includes the following:

- A $50 specialist co-pay

- No applicable deductible for specialist visits

Scenario 3: Minor Surgery

You need a minor outpatient procedure, and the total bill is $6,000. Your insurance includes the following:

- A $1,500 deductible (you haven’t paid anything toward it yet this year)

- 80/20 coinsurance after the deductible

- An out-of-pocket maximum of $5,000

Scenario 4: Yearly Medical Costs

Let’s say you have an HDHP and have had a tough year, medically speaking. You’ve had several medical procedures, totaling $35,000 in bills. Your plan includes the following:

- A $3,000 deductible

- 70/30 coinsurance (insurance pays 70%, and you pay 30%)

- A $7,000 out-of-pocket maximum

- How much do you pay in total for the year?

- How much does insurance cover?

- You pay your $3,000 deductible first.

- The remaining $32,000 is subject to 70/30 coinsurance, meaning you owe 30% of $32,000, which is $9,600.

- However, your out-of-pocket maximum is $7,000, so you don’t have to pay the full $9,600. Once you’ve paid a total of $7,000 (including your deductible and coinsurance), insurance covers 100% of the remaining costs.

- Total you pay = $7,000 (out-of-pocket max). Insurance covers the rest.

Health insurance can feel like a confusing maze of numbers and jargon, but once you break it down, it’s really about how you and your insurance company split costs.

Here’s what to remember:

- Premiums are what you pay every month to keep your coverage active, like a gym membership.

- Deductibles are what you pay before your insurance starts helping, like meeting a spending threshold.

- Co-pays are small set fees for doctor visits or prescriptions, while coinsurance is a percentage split between you and your insurer.

- Your out-of-pocket maximum is the safety net that caps your total costs for the year, protecting you from medical bankruptcy.

- Networks matter! Going to an in-network doctor will ensure big savings, while out-of-network care can leave you paying far more.

Understanding these terms can help you make smarter choices when picking a plan, budgeting for medical expenses, and avoiding surprise bills. Health insurance isn’t just a monthly bill—it’s a tool that gives you access to care when you need it while protecting your finances.

-

- Co-Pay

- A fixed amount you pay for a covered health service.

- Coinsurance

- The percentage you pay for a covered service after meeting your deductible.

- Out-of-Pocket-Maximum

- The most you’ll pay for covered services in a year before insurance covers 100%.

- Network

- A group of doctors, hospitals, and providers that your insurance plan has contracted with.

- Explanation of Benefits (EOB)

- A summary from your insurer showing what was covered, what you owe, and what they paid.

- Health Maintenance Organization (HMO)

- A plan requiring you to use in-network providers and get referrals for specialists.

- Preferred Provider Organization (PPO)

- A plan offering flexibility to see any doctor, with lower costs in-network and no referrals needed.

- Exclusive Provider Organization (EPO)

- A plan covering only in-network care but without referrals for specialists.

- High-Deductible Health Plan

- A plan with a higher deductible but lower premiums, often paired with an HSA.

In this lesson, you discovered why you need health insurance and how it can help you reach your financial goals. You also learned all the health insurance terms you need to know to understand how health insurance works.